*Please see our disclaimers at the bottom of the page and our full disclaimer here. By using our website, you acknowledge you have read our disclaimers and agree to our terms of use.

**Thank you to all of our subscribers! We hope you enjoy our Tencent piece and please join our Discord to continue the conversation!

***This piece contains a rather long product walkthrough of Weixin/WeChat and QQ as it is important to understanding Tencent. If a reader is familiar with Tencent’s products, they might want to skim these sections, as it is highly detailed since many non-Chinese do not have access to their apps due to the Chinese Firewall.

Founding History.

Ma Huateng was born into a relatively well-off family in 1971, with both of his parents working at China’s Maritime Safety Administration in the Huainan Province. Showing signs of being precocious at a young age, Ma Huateng was drawn to astronomy after being cultivated with a steady diet of science books and magazines. In 1984, the family moved to Shenzhen, which would turn out to be incredibly fortuitous, as Shenzhen’s Special Economic Zone would not only provide Huateng future work opportunities but also be vastly more accommodating to founding a private enterprise. In another stroke of luck, a few years later at Shenzhen middle school, he would meet his future co-founders: Chen Yidan, Zhang Zhidong, and Xu Chenye. Scoring high on the Gaoke (allegedly a 739 out of 750, ~100 points higher than most top universities required), Ma Huateng could have gone anywhere, but opted to stay close to home in Shenzhen (the political unrest at the time likely played a role).

With Shenzhen University not offering an astronomy major, Ma Huateng elected for a computer science degree, coming to the same decision as his middle school friends, Zhang and Xu, who also attended Shenzhen University. Quickly becoming an expert in the C++ programing language, he and his friends would hold competitions to see who could create the best viruses that would lock a computer permanently. Ma Huateng often won, earning him the label “Master Hacker”. When Ma was a senior in college, he interned at a prominent computer company, Liming, and developed a graphics-rich, stock market analysis tool on the side that his employer ultimately bought for 50,000 yuan, which was equivalent to several years of salary at the time.

In 1993, Ma Huateng, who was also going by “Pony” (the English translation of his name), graduated and went to work as a software engineer at Runxin, a telecommunications company specializing in pager services. While he was an effective engineer and would eventually receive managerial responsibilities, his time there was relatively unimpactful to the founding of Tencent compared to his encounter with CFido. CFido, or Chinese FidoNet, was a rudimentary message board system ran by a group of Chinese computer and software enthusiasts that operated through basic telephone modems. Many active users who Ma Huateng would regularly converse with later became important players in developing China’s tech sector including Lei Jun (Xiaomi founder) and Ding Lei (NetEase founder). Ding Lei became a friend of Ma’s and shared his war stories of starting NetEase over beers. Embolden by the success of Ding’s flagship website, 163.com, he itched to start an internet company of his own. In 1998, at a quaint coffee shop, Ma turned to middle school friend, Zhang Zhidong, and said “let’s start a company”. He quit his job and looped in friends Chen Yidan and Xu Chenye and, after realizing four engineers wasn’t the most balanced team, brought in an acquaintance, Zeng Liqing, who had sales experience. The five of them started a company that would utilize pagers to send voice and text messages. Tencent was born.

Background History.

While they were working on “pager services”, the team noticed an opportunity for instant messaging. In 1998, AOL purchased the Israeli company that launched ICQ instant messaging just two years prior. The attraction to instant online messaging was clear as it was an effective and cheap communication means, but there were a ton of clones popping up to chase the opportunity. However, none had served the Chinese market well. The team split the company in two divisions and created the OICQ business line (the “O” stood for “open”) to focus on the opportunity. The product proved to be successful with better localization and features like offline messaging, which supported rapid growth: they reached 1 million users just 9 months after launching.

However, their rapid success proved to be almost lethal to the company, as they had no revenue sources and the cofounder’s ability to self-fund was reaching its limit with expanding server needs. Adding insult to injury, they were served a lawsuit from AOL claiming that ICQ was their intellectual property and that they needed to immediately cease operating under OIQC domains. Tencent had RMB 10,000 in cash left. In a telling show of Ma’s momentary desperation, he pushed a dual track strategy of raising funds or selling the company outright. Potential acquirers met Ma with trepidation given their lack of monetization strategy, but he was able to still attract a low ball offer worth around ~$100,000. Learning of “venture capital” in the nick of time, they were able to secure a meeting with IDG Capital. When Ma was asked by IDG’s partners what is Tencent’s future, he replied, “I don’t know”, showing his characteristic honesty. Only weeks before reaching insolvency after drawing personal credit lines, they received a $2.2mn investment at a $5.5mn pre-money valuation, with IDG taking a 20% stake and Li Kashing’s son putting up the funds for the other 20%. A few months later, the tech bubble popped, drying up all appetite for tech investments.

Tencent changed their social messaging product name to QQ (the apocryphal story is that some employees overheard some people talking on a bus refer to OIQC as QQ) and Tencent added a group chat function, which helped fuel further growth. Just a little over a year later, they reached 100 million users but still had cash flow issues as they hadn’t yet figured out how to monetize the messaging app. They again fielded acquisition offers, but were repeatedly turned down. It was at this time that Naspers investment officers walked into Tencent’s offices unannounced after seeing the ubiquity of QQ at internet cafes across China. They offered to buy ~33% of the company at a $60mn valuation with existing investors IDG selling part of their stake and Li Ka-shing’s son all of it (11x one-year return sounded pretty good at the time…).

Noticing the trend in Korea where users would create custom avatars, Tencent copied this approach and was able to start monetizing these virtual items by selling them for a trivial amount (1-5 RMB each). In order to facilitate these transactions, they introduced QQ coins, which could be purchases through money-order, debit, Paypal or WAP billing (charged to phone bill). This was their first foray into payments and was so successful that the Chinese government eventually tried restricting their use for fear it would create a viable alternative currency in China. QQ continued to grow, and Tencent soon started expanding their internet service offerings. As a natural extension to socializing online, they published their first video game in 2004 called QQ Tang which was a casual game, but with more social elements relying on the QQ social graph. With that success, they continued to roll out over a dozen new games in short order on their QQ game portal. By year end they would have a million concurrent users playing games at peak times. With the business now solidly profitable, actually incredibly so for an early-stage internet company (they had $70mn of profit on $180mn of revenues for a 39% net profit margin), Tencent readied for an IPO. In 2004, they raised ~$200mn at a ~$1bn valuation for what probably was one of the cheapest priced tech IPOs of all time, valued at just ~14x 2003 earnings while growing revenues 50%+. After going public, they hired the lead Goldman Sachs banker who assisted in the IPO, Martin Lau, as Chief Investment and Strategy Officer, who has been largely responsible for all of the M&A they did thereafter.

With more cash, they started expanding their services with Paipai—an ecommerce platform aimed at Taobao, Tenpay—a payment escrow service similar to Alipay at the time (this laid the foundation for Weixin pay), and Soso.com—a search engine. All of these efforts eventually failed, but they informed a very important strategy that Tencent would employ from here on out: only build within your competency and partner with the best for everything else. (Paipai would eventually be folded into JD for a 15% stake, which they then later further increased). In this expansion growth phase, they made one of their most important acquisitions in Foxmail, with the aim of building a QQ Mail product. They acquired Foxmail in 2005, which was second to only Hotmail at the time. However, more important than the user base (Tencent’s was much larger at the time), was acquisition of Foxmail’s founder, Allen Zhang (Zhang Xiaolong), who would eventually create Tencent’s (and China’s) most important product.

In 2010, with the rise of the Smartphone, messaging was moving to mobile and QQ was at risk of becoming increasingly irrelevant. Allen Zhang was watching the rise of “Kik Messenger”, a text messaging app that allowed users to exchange messages for free, before shooting an email to Ma that they should develop a similar product. Ma agreed and gave Allen the latitude to lead the product that would ultimately become Weixin (known as WeChat in English—although that technically refers to the international version of the app. Weixin is pronounced “Way-shin”). It was launched in 2011 without much traction, but a second version which added the ability to connect QQ contacts and voice messages was a success and quickly reached 30mn users (QQ had 720mn active user accounts at the time). Adding a few other novel features like “Shake”, which matched users to someone else who was also shaking their phone (think Chat roulette), “Drift Bottle”, which allowed a user to drop a message in a geolocation for others to pick up, and “Nearby”, which allowed a user to see who was near them and was often used in a Tinder like way. In a subsequent version, they launched a feature that would be critical to Weixin infrastructure: QR codes. At first, these QR codes were simply used to scan contacts to add, but more creative uses were quickly proliferating. Just 14 months after launching, they reached 100mn users.

They continued to add new features like Red Envelopes, which allowed users to send money to each other in the traditional Chinese manner to gift money, and Moments, which is an in-app Instagram-like social media platform. These elements further galvanized growth to eventually become so ubiquitous that virtually every Chinese phone had Weixin on it. With such a highly penetrated user base, there was the opportunity to continue to push more capabilities like payment (Weixin Pay), Mini Programs (light apps that load like a webpage but have functionality more like a mobile app), and a slew of everyday services like ride hailing, booking a doctor, and paying bills in addition to much more (we will rehash Weixin functionality in-depth later). In time, virtually every Chinese smartphone would have Weixin downloaded on it.

Around the time of Weixin’s launch, Tencent completed an important acquisition. In 2011, they purchased a majority (93%) of Riot Games, the developer of League of Legends, giving them their first owned top-tier gaming IP. Their relationship with Riot Games started earlier though. In 2008, Tencent made a minority investment (22%) in Riot Games and partnered to help them distribute the game across Asia (you may recall from our SE piece, Tencent used Garena, SE’s gaming arm, to distribute the game in SEA. Tencent owns ~22% of SE). Partnering with minority equity investments or buying studios outright is Tencent’s playbook that they would run many times of the years, including in 2012 with a 40% stake in Epic Games, creator of Fortnite and the Unreal gaming engine (more on other investment later).

In the years that followed, Tencent would continue to innovate and expand their dominance in the lives of the average Chinese consumer, as well as Chinese businesses, through Tencent Video (SVOD), Tencent Pictures (production studios), Tencent Music, Kandian (news), Tencent Cloud, LiCaiTong (wealth management), Weixin Work, Tencent Meeting, Tencent Marketing Solution, and much more. Today, Ma Huateng remains at the helm of Tencent as the CEO, with much of the original founding team still involved in some capacity, including Xu Chenye as CIO (Chief Information Officer). With a sense of Tencent’s history, we will now go further in depth into their business as well as products.

The Business.

Tencent has changed their reporting structure several times throughout their history as a public company, but today operates through six operating groups (Corporate Development, Cloud & Smart Industries, Interactive Entertainment, Platform & Content, Technology Engineering, and Weixin) and reports four segments: Value-added Services, Online Advertising, Fintech and Business Services, and Others. Note that the first two segments (VAS and Online Advertising) are organized around monetization methods, while the third, Fintech & Business Services, is organized around their business lines. Their VAS and Online Advertising revenues are primarily generated by their video gaming and media & social businesses. As a result, we will first go into details by business, diving into their products, and then go through each segment’s monetization (which will overlap across different business lines).

At a high level, in aggregate, Tencent has grown revenues every year for the past 20 years, with 20% growth (experienced in 2019) being the lowest annual growth rate in their public history. That comes out to a 20-year revenue CAGR of 58%, a 10-year CAGR of 38%, and a 5-year CAGR of 36%. This is an incredibly long and consistent track record that required Tencent to make multiple pivots and expand into many different business lines. Perhaps even more incredibly though, they made an operating profit every year with margins never dipping below 25%. LTM revenues are roughly RMB 550bn or USD $86bn with operating profit of RMB 129bn or USD $20bn (which includes interest income of ~$1bn). Growth has been trending slower in recent years with revenues growing +19% in the past 9 months, but Tencent is a highly diversified business, much more so than their 4 segments suggest. With so many different businesses, several of which are purposely throttling monetization, growth could remain strong for multiple decades. We will now go through their businesses, starting with Gaming, followed by Social Media, and then Professional Media. Keep in mind, this is our grouping of businesses and not Tencent’s, but we think it is a logical way to group their operations.

Gaming.

Tencent’s video gaming endeavors started with simple and low production games for QQ, but they have since stepped up to become a top-tier game developer (especially in mobile) and the global leader in video game publishing. China is the largest consumer of video games commanding 30% market share globally and with mobile phones being the most popular gaming device.

An important idiosyncrasy in the development of the Chinese video game market is the fact that gaming consoles (Playstation, Nintendo, Xbox) were banned until 2014, so very few Chinese grew up playing them (there was very limited availability on the grey market). This meant that throughout the 2000s, PCs were the main gaming device for many consumers, although a high-quality computer was cost prohibitive for many Chinese. This led to the popularization of internet cafes, which were commonly flooded with gamers, but insufficient to make gaming mainstream for the average Chinese consumer. It wasn’t until the popularization of the smart phone, paired with freemium gaming, that video gaming was truly “democratized” with cost and friction becoming negligible. Globally, the console and PC gaming markets are each estimated to have ~20% share of total gaming revenue, with mobile games taking the other ~60%. Given China has a trivial amount of console users, mobile gaming is even more popular in China with 70-75% gaming market share. TAM estimates vary, but China has around ~$50bn of annual gaming sales with ~$15bn of that estimated to be PC related. Tencent commends roughly half of that with over $25bn of video gaming related revenues LTM.

Tencent’s original forays into gaming were originally exclusively PC focused and built on the backs of their QQ social network. But after launching QQ Tang in 2004, they quickly expanded their gaming capabilities. By the end of 2005, Tencent had 34 mini casual games including the very popular QQ Pets and had developed their first “fuller” game which was an MMOG (massive multiplayer online games) called QQ Fantasy. MMOGs usually have thousands of players that play on the same server in the same “world”; these sorts of games are uniquely suited for QQ given the social nature of the game with most players playing with friends. While Tencent was growing production in their owned gaming studio, they also started licensing content from other studios. Also in 2005, Tencent licensed one of their first hit video games, R2Beat, from a Korean studio. With them rapidly developing and licensing games, their game portal, QQ Games, quickly became China’s most popular gaming portal.

With early success in gaming, Tencent started to lean into the role of publisher and distributor for various game developers, a role in high need given the barriers to release a game in China. All games distributed in China needed a license from the SARFT (Chinese State Administration of Radio, Film and Television) and these licenses were only granted to Chinese companies. However, a developer without a license could partner with someone who had one in order to get their game published after going through a content review process. This was an important factor that Tencent would utilize to their advantage, positioning themselves as the “go to” video game publisher for Western studios to access the Chinese market (NetEase used a similar strategy). This was a crucial reason why Riot Games wanted Tencent to invest in them in the first place in 2008: almost guaranteed access to the Chinese market. Tencent would use a sort of “stick and carrot” approach whereby studios needed someone by law to publish their games, but they also offered superior distribution as well as expertise in what appeals to a Chinese audience.

Tencent quickly learned what worked in the Chinese market and would help studios localize games in order to improve the chances they would be successful in China. The games art style usually changes because of cultural differences in gaming preferences and sometimes a game studio may reskin the whole game. Per Tencent management, a popular art style in China is cute and stylized characters with abnormally large heads or anime-style graphics with cartoon-styled avatars. However, the popular western cartoon style that looks more realistic (like Family Guy) are highly disliked by a Chinese audience. Tencent can either license the game and help localize it or simply just advise the studio on what works. Given the partnership nature of development, it was common for Tencent to push for minority stakes (and later majority). The financial stake helped the studio develop a better game and ensure Tencent’s voice was heard, but it also likely acted as a sort of financial bondage that made it unlikely competitor NetEase would win that business. The combination of regulatory acumen, a large social network, monetization tools, best in class gaming expertise in China, and (sometimes) financial backing made Tencent an obvious choice to partner with.

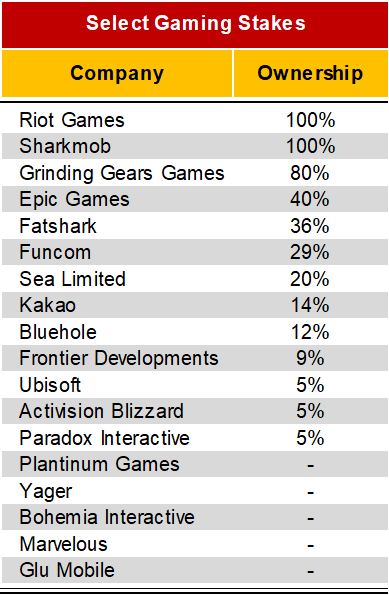

Tencent actively developed many different gaming partnerships and acquired numerous studios in the process of building their gaming portfolio. In addition to their in-house studios, Tencent has ~60 known gaming investments including full ownership in Riot Games and Sharkmob, a 40% stake in Epic Games, 20% of SE, and 5% of Activision Blizzard and Ubisoft. Below we highlight some of their more notable stakes with ownership listed when known.

Mobile Gaming.

While their gaming business started on the PC, Tencent managed the transition to mobile very well. Given their legacy Telecommunications business (resold SMS and other phones services and actually built the national WAP/ WEB portal for China Telecom) they were well aware of the growing importance of mobile. Alongside the rapid adoption of Weixin in 2013, Tencent was developing dozens of mobile games. The first mobile game they released was called “Tiantian Kupao” or “Cool Run Everyday”. Within 10 days of launching they had 50mn registered users with 25mn+ DAUs, making it the most popular mobile game in China at the time. They added a “games” tab in the discover section which allowed users to access all of their new games. Their first games were much lighter given slower and smaller smart phones, but they quickly became convinced that their tier 1 IP could also provide a compelling gaming experience on a smartphone (we will touch back on this momentarily).

Above is how a user can access games through the Weixin app. Below is what that looks like on WeChat (Wechat is the international version of Weixin and this version was set to English). Note that you have the ability to download games directly into the WeChat app and they are also stored within WeChat. This allows them to surpass the app store and deliver games to their users with less friction, especially with WeChat Pay layered in for in-app purchases. Additionally, this creates more functionality for WeChat, increasing stickiness and also giving Tencent a new way to monetize WeChat through games.

Tencent kept adding various in-house developed mini-games while opening the platform to 3rd party games as well. It is worth mentioning that as Tencent rapidly increased game selection they were commonly accused of copy-catting popular games (see below). These criticisms were largely valid, but nevertheless it didn’t matter to the success of the games: superior distribution and social functions hands down beat originality. With Tencent mini-games you can see what your friends have scored, invite them to play, and even receive notifications when they beat your score. If you recall from our SE piece, Garena originally paired gaming and social functionality to become one of the largest PC game distributors in SEA because of how strong of a combo this is. The network effects from having an integrated social graph helps new games grow with little advertising cost and games you play with friends have increased retention. Additionally, Weixin’s large userbase introduces many new users to games for the first time, with management saying ~1/3rd of mini-game users do not play other mobile games.

Today there are over thousands of mini-games on Weixin, all of which are limited to 8mb, up from 4mb originally. The small file size allows users to download the game quickly (like loading a large web page vs full app). Some studios would put a small version of their game or the first level of it on Weixin Games to get visibility and then direct the user to their full game upon competition. Getting a demo of the game before downloading a full app, which can take over 10 minutes for large games increases conversion. For instance, a popular puzzle game called Memorial Valley (pictured below) created a mini-game version which was just the first few levels. This allows users to quickly try the game and then directs them to download the native app upon completion. (How they download the native app is a more complex question we will get to shortly).

Tencent can direct traffic to these mini games through optimal placement in the game tab and calling out “new” or “hot” games. Given this capability it shouldn’t be too surprising that the most popular mini games are usually those Tencent developed or has exclusive publishing rights to (including Memorial Valley). For developers though the mix of distribution, social functions, access to Tencent’s ad network to monetize, and a payment mechanism was a strong value prop that many developers would find a lot of success with favor. The revenue share between Tencent and the developer has moved around a bit, but it is today a 50/50 split with the first 2mn Yuan (~$315k) receiving a 70% split in the developers. This may seem high, but it is actually inline to slightly favorable for the Chinese app market, as we will show in a bit.

Mini-games do have their drawbacks though, namely the app size which prevents a more in-depth gaming experience. Tencent saw that mobile gaming would go beyond light, casual games and was pushing Riot Games to develop a League of Legends (LOL) mobile game early on. However, Riot Games refused to because they thought it would be a watered-down game that would hurt the LOL brand. Despite Tencent owning 93% of Riot Games, the founders’ maintained control, so Tencent couldn’t force them to make a mobile version. Instead Tencent pushed ahead, giving two of their inhouse studios, TiMi Studio Group and Lightspeed & Quantum Studios, the green light to develop a MOBA (multiplayer online battle arena) game that would be a rough “reproduction” (to put it kindly) of LOL. To understand the decision to have multiple studios essentially rip-off a game that they owned, you have to understand the culture of internal competition that Tencent encourages. Roughly translated to “Horse racing mechanism” in English (an ode to “Pony” Ma’s competitive spirit), Tencent pits multiple teams against each other for the same project. When Weixin was being developed as a mobile messenger, a separate team under QQ was creating their own mobile first product. This does mean that redundant resources are used on the same project, but also increases the chances of success with more autonomy granted to smaller teams, encouraging bottoms up innovation. In Tencent’s culture, refusing to accept a project just meant that it would be passed to another team (or teams in this case).

The two MOBA games, Legend Heroes by TiMi and We MOBA by Lightspeed & Quantum, were released on the same day (!) in 2015. Initially Legend Heroes flopped, while We MOBA was gaining strong momentum, however TiMi quickly reiterated the game and relaunched Legend Heroes three months later as Honor of Kings. Within months it garnered tens of millions of active users and would go on to become the highest grossing mobile game of all time: in 2021 Honor of Kings is estimated to generate just under $3bn for total lifetime sales of ~$13bn. Honor of Kings’ success emboldened Tencent to focus on mobile games and they would continue to publish more hit titles than anyone else including: PUBG (self-developed) , Clash of Clans (Supercell developed, has majority stake), Boom Beach (Supercell), Brawl Stars (Supercell), QQ Speed Mobile (self-developed), CrossFire Mobile (exclusive publisher), Perfect World Mobile (exclusive publisher), Call of Duty Mobile (publisher and helped develop), Fortnite (exclusive publisher, owns 40% stake), and eventually even League of Legends, who launched a mobile game in 2020 after seeing how successful Honor of Kings was.

We will touch more on monetization in the VAS and Advertising sections, but most of these games monetize via a mix of in-app virtual item purchases, “season passes” for exclusive content, and advertising. In just 10 years from launching their first mobile game, they went from an inconsequential portion of revenues to around ~80% of gaming revenues (with the rest attributed to PC). In terms of Tencent’s total revenue, VAS gaming revenues (in-app purchases), is responsible for ~30% of Tencent’s total revenue with mobile alone responsible for contributing 25% of their total revenue. Clearly gaming has been a huge boon to Tencent, with game revenues up ~3x in just 5 years to ~$25bn. We will pick back up on this in the monetization section, but first a few words on app distribution.

App Stores and App Downloads.

App store dynamics are very different in China with Apple’s iOS only having ~10% market share and Android the remaining ~90%. But since Google has no presence in China, which includes their Google Play Store, there is no natural app store leader. Given the large and high margin revenue streams from running app stores, many players have competed for this business. Tencent’s “MyApp” app store is the leading app store on Android, but they only have an estimated ~25% market share by active users. Huawei’s App store, Oppo’s App store and Qihoo’s 360 Mobile Assistant are 2nd to Tencent with an estimate 10-15% each, however these estimates do not have a high degree of confidence as data is sparse and sometimes self-reported. In fact, some Huawei estimates put them neck to neck with Tencent in terms of usage. 3rd Tier app stores include Baidu Mobile Assistant, Vivo App store, and MIUI App Store by Xioami, which each have <10% market share. Then 4th tier app store with an estimated low to mid single digit market share are PP Assistant by Alibaba, China Mobile MM Store and Anzhi Market. However, even these 4th tier app stores can have 20mn+ users. In total though there well over 5,000 different app stores, but these ~10 comprise the vast majority of the market.

Given the level of competition for app downloads, it is interesting to note that the fees are actually much higher in China than the rest of the world. Tencent app fees range from 40-70% with 55% being a typical rate for games (Tencent sometimes negotiates on a game-by-game basis like with Genshin Impact where they only charged 30%–the lowest rate they’ve ever been known to accept). However, these revenue shares aren’t so straight forward because Tencent can still make money through Weixin pay (usually 100bps take-rate) and games utilizing their advertising network (where fee rates vary). Other app stores similarly have ~50%+ app store fees. App store fees range closer to ~50% in China vs 30% globally, which are already at risk of being legislated down. With 5,000+ app stores and 10 “main” ones you would expect such competition to reduce app store fees, but instead they were driven higher.

Instead of competing on fees to draw more developers in, these app store owners go to extreme lengths to keep their consumers captive to them by erecting barriers from fair competition. The OEMs (Huawei, Oppo and Vivo) will have their app store predownloaded on the devices they sell (similar to other OEMs elsewhere), but if you try to download an app through another channel (or a competitors app store) it will flash scary warnings that you could be about to install malware and directs you with large and colorful buttons to stop. These ruthless tactics keep the app market very fragmented, but also “uncompetitive” in terms of fees that are charged to the developers.

Therefore, an undue (and potentially unsustainable) amount of leverage lies with the distribution partner versus the developer. The global standard is for the developer (creator) to receive 70% to 85% of their creation, but this is almost always under 50% to as low as 30% in China. In a world where distribution costs are generally near zero and there is little friction to download an app, the App Store owners have to create friction and barriers in order to maintain their fees. With anti-competitive practices increasing in China, Tencent could potentially be at risk of having their app fees reduced, not necessarily by statute but rather through opening up competition. If other app stores are no longer allowed to steer consumers away from alternatives, then perhaps they are more inclined to compete on fees to preserve market share. Maybe not though. As this relates to Tencent though, they often have a role in multiple pieces of the value chain beyond just the app distribution, so it is possibly they can make up any losses elsewhere (whether that be raising payment fees, ad network take-rates, or publishing revenue share).

Furthermore, Tencent has a privileged position with app downloads because they can use Weixin to get users to download apps directly through it. For instance, to download Honor of Kings you can search it in the games tab and simply click download without having to visit another app store. A similar thing can happen when on a business’s official page (more on this later) and it can direct you to their native app if they have one (most do not though and instead have a Weixin mini-program). It is likely this ideal placement in the flow of app discovery allows Tencent to capture the app download regardless of new app-related regulation.

Separately, users can download Tencent’s MyApp which functions similarly to any other app store. It is likely that Tencent’s higher app market share comes from Weixin’s superior user acquisition rather than their actual App Store app, although there is no available data to confirm that.

As mentioned, we will return to the financial side of gaming in the VAS section after going through Social and Professional Media.

Social Media.

Tencent has many different social media properties, but QQ or Weixin is the entry point for almost all of them, so we will organize our discussions around those two products, starting with QQ. Within QQ there is really two different product groups. The first is QQ the instant messaging application that started on desktop and the second is QZone, which is a social network with a lot of different functionality (think of something closer to a MySpace) that grew from the messaging app. Before getting into each product we will give some high level thoughts on the health of the platforms.

As seen above, QQ was Tencent’s dominant social app until it was overtaken by Weixin in 2016. Today Weixin & Wechat have over 1.25bn users, making placing them amongst the world’s most used apps, behind only Whatsapp, Facebook, and Facebook Messenger. However, Weixin’s functionality far exceeds other social apps and is closer to an operating system or full suite of apps than a single smartphone app.

Tencent has battled to keep QQ relevant with mixed success. QQ has been losing users (mostly to Weixin), with cross-platform usage (PC to mobile) keeping it somewhat pertinent, but users are still down ~300mn or 31% over the past 5 years to 575mn. Similarly, Tencent has been going through a herculean effort to keep their social media platform, QZone, relevant, though the outcome also hasn’t been stellar. On one hand, you can argue that a social network can rapidly degradate into irrelevance as users flee, as it happened to MySpace over just a 2-3 year period, and so Qzone only shrinking ~25% over 5 years can be seen as a moderate success. On the other hand, it is hard not to think of a social media platform born in 2005 with a shrinking user base as in run-off and in danger of soon reaching irrelevance.

However, the loss of users isn’t such a clear negative because as social media options proliferated and with the success of Weixin taking some of Qzone’s functionality, Tencent responded by further pushing the platform to cater more towards the youth which likely accelerated the user decline. They differentiated the QZone platform by emphasizing more fun and playful features with more colorful and “bubbly” animation. While they stopped breaking out QZone MAUs separately in 2018, today they still have an estimated ~500mn MAUs on the platform, which still ranks it among the top social networking platforms globally. It was hard to find many contacts that used QZone, but many of their kids were familiar with it.

We will now go through a product walk through of Weixin/ WeChat, QQ, and QZone. If a reader is familiar with the products they may want to skim through the product info (which is highly detailed since many Westerners have no experience with their products and cannot access them due to the Chinese Firewall) to get to the Weixin Ecosystem and Superapp section.

QQ.

The original QQ product was a simple desktop-first messaging application. As mentioned in the history, over the years they added a lot of functionality to QQ including games and a separate social media platform, Qzone. The core desktop messaging product is still available today though (pictured below). While they stopped reporting separate QQ MAUs and QQ Smartphone MAUs in 2018, at last disclosure in 2018, 807mn people used QQ monthly. For the past three years they have only reported QQ Smartphone MAUs, which were 574mn in 3Q21 and there is likely another ~100mn or more who exclusively use desktop. While Weixin is the clear dominant mobile messenger, some users still like QQ messaging because it is cross platform (desktop to mobile) and there are no file limits on QQ. While work specific messengers have become more popular recently (Tencent’s WeCom amongst them), prior to that many users would utilize QQ as their “Slack” or “Teams”.

Above is the QQ desktop app, which you can see only takes up a small portion of the screen. Clicking the buttons on the bottom of the screen will open new windows.

We will now go through all of the functionality within QQ (there is a ton!). Starting at the top of the screen clockwise, the first thing we want to call out, and a notable differentiator between QQ and Weixin, is that QQ allows users to display their “status”.

Status: This allows a user to know which friends are online and available for engagement, which creates more of a sense of “immediacy” to respond, helping foster more spontaneous conversations, versus text where there is more intentionality when messaging and no similar expectation to quickly reply. This sentiment harkens back to the origins of the web and even today being “online” has some connotation of being available and in the same virtual “space”. Practically though, it helps users decide who to chat with and pressure into playing online games with.

Custom Skins: QQ is heavily customizable with “Custom Skins” among other personalizations, which helps retain a strong following with the young. In our talks with consumers a common sentiment was that “Weixin is for old people – and designed as so. QQ lets you express individuality”. There was a line of thinking common in our research that customization was especially popular in China because of a cultural history of uniformity and tough competition making it near impossible to stand-out. However, Tencent’s customizations, especially with a users’ avatar, allows a user to look different. Whatever the reason, these personalizations have been wildly popular since the beginning of Tencent.

Medals: The medals button is a gamified feature where users can earn virtual badges for downloading certain apps and other online activities. In theory, this incentivizes app downloads through Tencent and other online behavior, but it is unclear how many users care.

QQ Mail: QQ Mail is QQ’s email provider that was launched early in the development of the internet, giving it a critical leg up versus others. Today it is a market leading email provider with many non-avid QQ users still retaining and using their QQ emails. Anyone who was over ~20 that we spoke to in China associated QQ with email and their messaging app second. Shopping Cart. The final call-out here is on the shopping cart – the shopping cart directly links to JD.com, a Tencent partner and portfolio company. This seems like a relic of their prior ecommerce ambitions, as it seems like a contrived way to enter the JD site, but we suppose some users may value this function.

Now moving to the bottom of the screen there are 6 buttons, each of which bring up new screens.

(1) Add/discover friends, groups, courses: The add/discover button is the foundation of the QQ platform. After clicking it a new screen pops up with 5 different tabs. Besides importing their existing contacts, users are able to search for people via a variety of filters including name and QQ number. They’re also able to look for groups, browse KOLs, find online courses, and source services.

The photo above shows the “Find a Group” screen for League of Legends (LOL). Here you can see several groups built around LOL gameplay and characters. Think of this like a Facebook group – but with group size limited to under 500 (but can be set to a lower limit). Besides size, QQ also limits the number of groups a creator can create (up to 6 groups), in hopes that the creator will continue to stay active in their groups. While there are several reasons for these limits (likely technological in the beginning, but today more so political), one of the key benefits is the forced intimacy a smaller group brings. People already self-select for their interests, and these limits force engagement – leading to more active and vibrant communities.

The photo above shows the “Courses” screen. It may seem odd or random to have a separate “courses” section, but remember that QQ is positioning itself towards the youth, basically all of whom are students. Getting a student to take a course through QQ is a great way to keep them coming back to QQ and also may alleviate a parents concern that QQ is a time suck. Here, users are able to search for courses on a variety of skills and topics like programing and Gaokao test prep. Clicking on one of the courses will take you to a homepage that includes several sample videos, information on the instructors, the syllabus, and the price of the course (you can think of this as being similar to Coursera). Oftentimes, these courses will have dedicated QQ groups as well, and make use of Tencent Documents and Tencent Cloud (more on this later).

The photo above shows the tab that allows users to find local and online services for anything from online tutoring to travel photography. You can think of this as a more curated Craigslist. This tab also seems somewhat a relic of the past as most users will do this through Weixin, Meituan or another app today.

(2) Tencent Documents: Tencent Documents is similar to Google Drive – it is a browser-based app where users are able to create, upload, and share a variety of files including text, spreadsheets, presentations, and more. This has clear tie-ins for schools, and makes it the obvious choice for online courses.

(3) Game Center: The video game controller button takes users to the QZone Game Center, where users are greeted with a customizable homepage and can discover new games. While this one-stop-shop for gaming is an attractive funnel for game developers, the Game Center’s larger display than a mobile app store allows it to focus on surfacing new content as well as what’s trending, making it popular with consumers.

(4) Mobile Game Assistant: Showing how important gaming is on QQ, right next to the game center button is a second gaming button. The mobile game assistant button serves a variety of functions, but it is most noteworthy for its mobile game emulator which allows users to play mobile games on PCs. (You may have experience with this if you ever played one of the popular Pokémon games via a Gameboy emulator on your phone or PC). As an added boost, video game developers need not customize their game code for PC specs, and can focus exclusively on mobile.

(5) Tencent Weiyun: Tencent Weiyun (mini cloud) is similar to Tencent Documents, but focused on a wider range of categories like photos, videos, and music. Tencent Cloud sells subscriptions for users to pay a monthly fee for bonus perks like more storage and faster upload/download speeds. This makes it easier to share files that are otherwise too large to send over mobile or email (email files have limited size). This is a very simple feature, but one that is highly annoying if absent and no doubt some users have remained on QQ just for this reason (especially among the older business professionals we talked to).

(6) App Manager: The App Manager is relatively straightforward – it allows users to see all of the apps tied to their QQ account for easy access. Interestingly though, they also have an “Others” tab, where users can discover and manage non-QQ/Tencent apps like Steam. The first photo below shows Tencent’s apps.

The second photo below is featured apps available for download.

QQ Mobile.

While QQ is designed as a native-desktop experience, they do have a mobile app that essentially is a facsimile of the desktop version, but with a couple important exceptions.

Kandian: On the mobile version of QQ, Kandian is preloaded as a “contact” and it shows up in “conversations” of the users feed. Someone from the US might think this is sort of a clumsy extension of the app, but that is more a byproduct of being used to messaging being totally separated from other social media (i.e. iMessages) and it is common in China to use the message feed for other products. Nevertheless, it is an effective way to delivery users more content and direct users from an unmonetizable surface (messaging) into a monetized feed (Kandian). Kandian is a cross-platform newsfeed designed to compete with Baidu and Bytedance. It provides users with a mix of media from the Tencent Ecosystem of apps including articles, photos, videos, livestreaming, and more. As noted, this allows Tencent to monetize QQ via in-feed ads and helps bolster their creator’s ecosystem by delivering them a larger audience. (As it will be relevant later, these sorts of ads are categorized as Social Ads).

Streaks: This is a screenshot of a private message between friends. The notification alerts the user that in order of the user’s contact to become a “good friend” – they must communicate daily for 7 days. Everyday there is a message, the four-leaf clover will grow and once a day is missed, the clover die’s. This is a simple, but powerful gamification tool that will keep users returning to the platform to engage their friends. Similar to Snapchat streaks where close friends will keep a “streak” going for years, this is results in a dramatic increase in user retention while also offering differentiated novelty that the youth on QQ enjoy.

As you can see there is a ton of functionality within QQ, but the adoption of a lot of these features is less clear. In general, we view QQ messaging as in decline, but with them still winning new users in the <18 age cohort, which isn’t a terrible given they have Weixin that serves everyone else.

QZone.

QZone is a social network, very similar to MySpace or Facebook, that was built off of QQ’s user base. A QZone user can see all of their QQ friends that are also on QZone. Similar to other social networks, users have pages and share posts, photos, etcetera with their friends. Just like with QQ, customization is very popular on QZone (and how they mainly monetize it). QZone offers a very popular “VIP Service” which is a monthly subscription that unlocks a host of customizations for a user. One of the factors (and a key differentiator vs Weixin’s Moments) that drives popularity of QZone is the fact that kids’ parents tend to not be on QZone. Below we show the homepage for QZone.

Below is the Game Center that is also accessible through QZone.

Qzone tie-ins with QQ have helped it remain popular with certain youth, but it is not totally ubiquitous even among the <18 crowd. The fact that parents aren’t on QZone does help it keep its appeal for certain teens.

Weixin/WeChat.

As we mentioned earlier on, Weixin and WeChat are essentially the same app, but WeChat is the international version and Weixin in the version used within China. Created in 2011, today the two apps together have 1,263mn MAUs as of 3Q21, with the vast majority of them (we estimate at least ~1.1bn) belonging to Weixin. For that reason we will focus mostly on Weixin, but will insert some WeChat comparisons when the apps differ. A lot of the interface is interchangeable between the two so we will not show both. (Most of the Weixin photos are in English because that is a setting you can change).

When you open the Weixin app you will see 4 main tabs: 1) Chats, 2) Contacts, 3) Discover, 4) Me.

(1) Chat: Chat is relatively straightforward – the tab is filled with “conversations” from your contacts, as well as business accounts users can follow or news aggregators.

(2) Contacts: While the “Contacts” tab is quite basic, it is instrumental to the Weixin ecosystem. The rise of Weixin has meant that users build up their contact lists within Weixin rather than their smartphones’ contacts app. This means that a user’s full contact list is held within the Weixin app and deleting Weixin would delete their contacts. Further entrenching Weixin’s “ownership” of the contact list is the fact that many contacts were adding with a “Weixin ID”, which is a proprietary ID tied to a specific user (think like a Facebook log in). So many users do not even have all of their friends’ phone numbers in their contacts since the Weixin ID effectively does the same thing, and is even quicker to add contacts with (QR code scan).

However, there is one critical point: it only works through Weixin. This is important to understand the absolute dominance of Weixin and how sticky of an app it is. Adding to the ubiquity of Weixin is the fact that it has transversed multiple use cases: whereas in the US you may give someone your email or Linkedin for professional use and phone number or Instagram when meeting someone new, all of this is done on Weixin. Having complete ownership of a user’s contact base had an interesting side effect: increased substitutability of the smartphone. Since users no longer held their contacts in their phone, changing phones became as simple as downloading Weixin on the new phone. This is part of the reason why China has such a competitive hardware market (Apple, Oppo, Vivo, Huawei, and Xiaomi all have sizable market share).

One important function with messages is the ability to chat with “Official Accounts”. This allows a user to talk to a business in an easy manner, similar to when a user messages an Uber driver or Door Dash partner. Weixin Official Accounts have other direct functionality, serving as a mini website complete with navigation links and FAQs.

There are two main types of Official Accounts: Subscription Accounts and Service Accounts. The Subscription Account is available to anyone so bloggers and KOLs (Key Opinion Leaders) would tend to use this option, however some brands do as well. Subscription Accounts are primarily to deliver content and work similar to how someone may use an email list. The content a KOL creates is pushed to a user’s subscription folder, which is nestled in between other messages (see below).

The Service Account has more functionality but require a business license. Once verified a Service Account can also utilize Weixin Pay and Weixin Mini stores. When a Service Account sends a message it shows up separately in the user’s messages, as seen below.

Clicking the Nike link would allow a user to access a light version of their website, message the business, read other articles, shop their ecommerce store, and access other mini-programs (more on mini-programs later). The mini-program below is to buy Nike sneakers, but they have other mini-programs for stuff like their membership program, running clubs, ect. These Official Accounts act as gateways to other activity. The idea is to push content, new product launches or discounts to users so they then land on your Official Account page and either shop or becoming more engaged with the brand with top of funnel product discovery (which leads to future sales).

(3) Discover: The Discover page is where Weixin and WeChat differ most due to different international availability of certain services. The core remains the same though with: 1) Moments, 2) Channels, 3) Scan, 4) Shake, 5) Top Stories, 6) Search, 7) Nearby.

(4) Me (Profile): Similar to the Discover page, the profile page is mostly the same across Weixin and WeChat. Here we will focus on payments and stickers.

We will first go through Discovery in more depth and then the Me section.

1) Moments: In the Moments tab a user can choose a profile and cover photo and the rest is the moments feed where a user can see their friends’ posts. The feed is very similar in function to Instagram, but with more of a tilt towards a private social network (like Snapchat). For instance, in a user’s Moments feed, they can see all posts that a friend shares, but they can only see comments and likes from users that also their friends. This is unlike Instagram where anyone can read anyone else’s comment on a public post. This makes likes less important since you can only see your friends likes and lowers the bar to comment since it isn’t totally public. Also lowering the bar to post is the ability to make post expire after 3 days, so they disappear and are not permanently hosted like Instagram posts are (effectively a hybrid between an Instagram Story and a Post).

Moments is monetized via in-feed advertisements, similar to Instagram, but Weixin is notorious for keeping their ad inventory very low. In fact, they only served a single ad unit per person per day in the feed for a while, with a 2nd ad unit introduced in 1Q18. The last time they disclosed ad load it was up to just 3 ads per person per day, which was in 2Q19 (but talks with advertisers imply they are now at 4 or more). The very low ad load gives us confidence that Moments is very under-monetized, especially versus global peers that may show ads 1 out of every 4-5 posts.

2) Channels: Channels is Tencent’s answer to Douyin and Kuaishou. Whereas Douyin is purely algorithmic, Weixin allows you to sort by 1) what’s hot, 2) what a user’s friends have liked, and 3) accounts a user follows.

3) Scan: Scanning is best known for adding someone as a contact via QR code or paying a bill, but it can do more than that. Weixin has built in the ability to translate languages by just aiming the camera at foreign words and can identify specific products. This ties into a search and shopping capability whereby a user scans something and a results page pops up with product details and reviews. Also on this page is listings of where a user can buy the items with integrations to JD’s mini-program for frictionlessly purchasing (assuming the user has a JD account and Weixin pay set up).

The first photo showcases Tencent’s ability to scan an item. The second photo is what comes up after finding that item. The third photo is what happens when you click into the second photo, which allows you to shop for the product.

4) Shake: Shake is a simple, but novel function. When a user shakes their phone they are able to discover different people who are also shaking their phone. A function like this has limited utility, but helped add to Weixin’s virality when it was a nascent product. They also added a second feature that allows users to identify music (think of Shazam).

5) Top Stories: The top stories page is split up into 2 tabs: 1) what’s popular, 2) what your friends have engaged with. This is an easy way for users to stay up to date with not just national news, but news for their specific friends. Top Stories integrates a number of different media forms, all of which can be saved in favorites—from links and files to music and places. This adds a newsfeed to Weixin that is constantly being updated and contains near limitless content, so a user may check this feed multiple times a day as a time kill.

6) Search: Search is another helpful function within Discover, where users can search for news and services like life insurance services, public transportation routes, Covid vaccination sites, utilities, and anything else hosted in Weixin like mini programs and business pages. For certain services there are mini programs the user can pull up and pay directly for via Weixin pay.

7) Nearby: This novel function allows a user to find people who are nearby and only requires you put in a gender and region. This was used as a de facto “Tinder” early in Weixin’s life before other alternatives were created and helped add to the original virality of the app. Today it is somewhat more just a gimmick.

8) Gaming: This is one of the differences between the international and domestic apps as only Weixin has the Game Center. This is likely because Tencent often only has gaming distribution rights within China and not internationally. The Game Center is basically: 1) an in-app gaming arcade that gives users the ability to pull up thousands of mini games and 2) also a gaming-focused app store that allows users to download full games. While they do not have many games available internationally, within China they are an essential partner who can make or break a game. Their ability to promote games is 2nd to none and the position it has within Weixin’s game center is a critical piece of that capability.

Once you click the Game Center icon in the discovery page you will get the page below. The tabs at the bottom are homepage, game, game group, chat, and profile pages.

Below, we show how to download a game from the game center by clicking into the Honor of Kings icon. To incentivize users to download the game from the Tencent game store, they offer in game virtual items (in the example they are offering: 30 “Emperor Gold Coins”, 3% Gold Coin Bonus, and 5% Experience Boost).

The ability to incentive user behavior with free virtual items creates a strong customer acquisition channel. If you recall, Sea does a similar thing with Shopee and their Free Fire, which allows them to effectively acquire users with no cash CAC.

9) Mini Programs:

This is the mini program hub where users can see what mini programs they’ve used recently or saved. A mini program is basically a “light” mobile app that has more limited functionality than a full app. Many standalone apps in the West would be unchanged as mini-apps though; think of the Starbucks app that you use just to order drinks, the Disneyland app that is used as basically just a map, or the UPS app which just tells you when your packages are going to be delivered. All of these apps have fairly straightforward functionality and would make good mini-programs. A big difference between regular apps and mini-programs is size: mini-programs are limited to under 10mb each so they can only support straight forward functionality and they basically load as a webpage would. A user will click a mini-app and it will quickly load within Weixin and allow the user to interact with it and then disappears when the user is done with it. This format is actually often superior to having to go to a separate app store and then download and open a different app to do simple tasks. It also eliminates a lot of app clutter that users accumulate overtime.

Another big benefit of a mini program is that they are easier to develop and cheaper than a full app so small businesses are much more likely to adopt them. For instances, many restaurants can create mini-programs that just host their menus and an order function whereby developing a full app would be untenable for most mom and pop restaurants. Having a mini-program also allows seamless access to Weixin pay and the user can follow the business as well, giving the business direct access to the consumer. The benefits are strong enough that Tencent hosts over 3mn mini-programs today. The downside of a mini-program is that Tencent does not share full data with the company (even partner companies like JD), but this drawback for the business just increases their reliance on Tencent. Pulling your program from Tencent means losing access to their ~1.2bn users and all of the commerce transactions that entails, which is estimated around $250bn of GMV for 2021.

Below you can see the miniprograms for JD, Bilibili, and XiaoHongShu (left to right).

Tencent’s Ecosystem is strong enough that there is little risk mini-programs leave and in fact are actually threatening other businesses like Alibaba’s Tmall as mini-programs provide an easy way for brands to reach their consumers in a more direct way.

10) WeChat Out: This is how users can call mobile phones and landlines worldwide. This used to be an important function, but with the proliferation of Weixin domestically and WeChat globally it’s usage has largely dwindled. Still though, it is another service that is nice to have without having to leave the Tencent ecosystem.

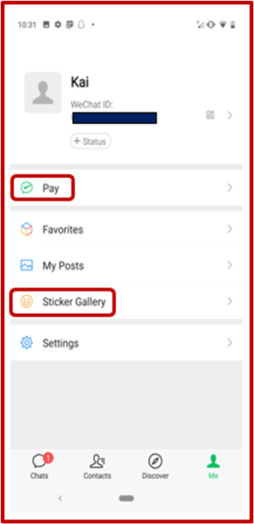

All of the functionality we just went over is housed in the discovery tab. The last tab is the “Me” tab which has two things we want to call out: 1) pay and 2) stickers.

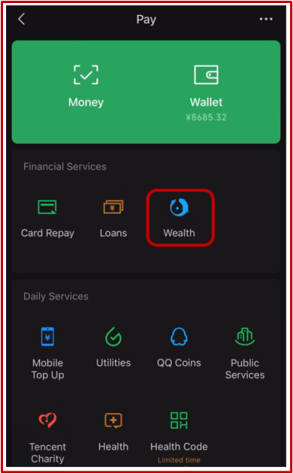

1) Pay: This is Weixin pay, which allows users to pay for goods and services online or offline via QR codes. It is very popular with an estimated 900mn+ users or almost all Weixin users. We will talk more about Weixin Pay in the Fintech section. As far as functionality is concerned though, users have a wallet which can store money or they can link bank accounts (credit cards have very low adoption in China). Pay is almost a Superapp in and off itself, with the ability to access a variety of services including ride hail, hotels, tickets, and shopping in addition to more utility functions like paying electricity bills and buying mobile top up. Users also have access to other financial products like money market funds and loans.

2) Stickers: The stickers page allows a user to look through millions of different sticker packs they can buy. Stickers are a popular way for people to express emotions and communicate in a way that is not easily captured by words or the limited emojis available. In China there are full time sticker creators that just try to design popular stickers for consumers, but success is very rare. Sticker creators actually can charge for their creations and usually sell them as a “pack” of 20 or so for small amounts of money (maybe ~5rmb and Tencent takes ~half of this revenue). Nevertheless, it is a popular product for consumers and Tencent has millions more stickers than anyone else. The sticker pages and some examples are shown below.

Weixin Ecosystem and a Superapp.

With a sense of how Weixin works and knowledge of all of its functionality, it may be apparent why Weixin has earned its designation of Superapp. Readers may recall how we were critical of Grab’s “Superapp” in our prior piece, but that is in part because of how incredible of a self-contained ecosystem Weixin is with everything from social media and messaging to shopping, games, and even millions of their own mini-programs, which are all proprietary to the platform, and enabled by Weixin Pay. Furthermore, the always-logged-in nature of Weixin means that Tencent can collect data on everything users do within their ecosystem with total clarity. In our Grab piece we defined a Superapp as follows:

A real Superapp is self-contained and can offer (directly or through partners) most of the things you would need over the normal course of a day. The Superapp effectively acts as a low-cost funnel of future customer acquisition for different offerings by keeping customers captive to a slew of everyday services. The high frequency nature of these “everyday services” keeps consumer churn de minis. Since the consumer already uses the app regularly, getting consumer adoption for a new service is as simple as promoting it with preferenced placement in the app.

There are really three core aspects that are essential to a Superapp: 1) high frequency to drive more “cross sell” opportunities, 2) essential services to reduce churn, 3) built in means to add new future services in a way that feels natural. The high frequency, essential services are like a foundation that everything else is built off of.

The idea that a Superapp has a foundation of “essential” services that are not designed to monetize, but just keep users attached to the platform is why many other Superapps fall short. Other companies that strive to create a “Superapp” whether it be Grab, GoJek, Paypal, Affirm, Klarna, all have shaky foundations that they are building off of in hopes of new services not only bringing in new revenue streams, but also increasing users retention. Their aims of creating a Superapp is to solve a business weakness, not to strengthen the value prop to the user (they would argue it does both of course). This strategy of trying to bootstrap your way into loyalty by offering users an increasing amount of services in hopes they adopt them is distinct from Weixin; who already had a strong lock on the consumer just from their superior messaging product which enjoyed strong network effects coupled with high switching costs from unportable contacts. It was from this high frequency and high retention product that they continued to build out their app more with an aim of doing more for the user, not solving a user’s loyalty issue. Tencent never hoped that adding a ride hail function would help solve their churn problems, but of course as they added more and more functionalities overtime the bar to compete against them increased.

Today, Weixin is so dominate as a platform and ecosystem that it is hard to see them ever being displaced, especially since they now host millions of mini-programs—this is akin to having proprietary access to a small portion of the internet with access only possible via your internet browser. Add in 20 million official accounts, which have critical information of millions of businesses, services and KOLs, and are also exclusive to Weixin and it starts to become apparent why most Chinese users seldom bother with Baidu’s general search—whatever they want is not only on Weixin, but restricted to it. Logged-in users with Weixin Pay integration and a user base of >1.2bn who spent ~$250bn on the platform last year means that it is almost always easier for a business to build a mini-program and official account within Weixin’s ecosystem than try to develop a presence outside of it, which only strengthens Weixin’s value prop to consumers. Just look to Alibaba, a company with 950mn active customers in just China, and yet they still see value in creating a mini-program to have a presence on Weixin. In fact, Pinduoduo’s rise could of very well of been prevented by an earlier Alibaba presence on Weixin. Tencent’s Weixin is just so large that its gravitational attraction pulls everything towards it and no company is too big to be better off without it. If you wanted to inconvenience the most amount of people to the highest degree by deleting just one app, you’d pick Weixin. Such importance naturally opens the door up to multiple monetization opportunities.

We will pick back up on Weixin and how it generates money in the VAS and Online Advertising segments. First though we will continue going through the business in the Professional Media section, which includes Tencent Video, Tencent Music and Chinese Literature.

Professional Media.

The Professional Media section includes a variety of different media products that leveraged Tencent’s user base with QQ and later Weixin to win consumer subscriptions. While all of these businesses feed back into Tencent’s other properties in some way, most of them are run more or less as standalone businesses. Tencent does offer bundles for users who utilize multiple services (Video, Music, Literature), but the bundles do not seem to drive much incremental adoption or lock-in since many users will cancel and sign up again for a single service multiple times a year.

Tencent Video.

Tencent Video, launched in 2011, is the largest online video platform in China by mobile daily active users. It is similar to Netflix or Hulu with a lot of exclusive content created by Tencent themselves. Tencent has their own production studios which help feed content for their video offering, but they also license a lot of shows. Viewers can watch with an ad-supported version or pay 250 RMB (~$40) for an ad-free experience.

We see Tencent Video with an ever-growing library of content including many of the most popular shows for just ~$40 a year as cheap, but the Chinese competitive environment is very different and higher mobile usage means other forms of social media are more direct competitors given that mobile time spent is more fungible (in other words, generally Tiktok may take some time spent from Netflix, but generally speaking if you wanted to watch something on your sofa Tiktok isn’t in that product use set. However, if you were watching Netflix on your phone than Tiktok could be a direct competitor). Given that many users watch “TV” on their mobile phones, other entertainment alternatives are numerous including Douyin, Kuaishou, and Bilibili.

There are also several other paid video services in the competitive set. Tencent Video is number one, but Baidu’s IQIYI is a close second and is known to have more “smash hits”. This analogy isn’t perfect, but IQIYI can be thought of as more of an HBO with very popular shows, but a more limited catalog that a user can burn through quicker, whereas Tencent Video is more like Netflix with fewer very popular shows (they still have many though), but more quality content that can keep a user captivated. IQIYI is known to be more creative and innovative, but they also have more misses. Additionally, Tencent Video has way more capital backing to buy and license content, so they will occasionally team up with IQIYI for joint procurement or a content agreement since IQIYI is superior at identifying top shows. Many users will have subscriptions to both services or will rotate between the two (subscribe a month and then cancel and sign up for the other). However, despite this behavior subscriptions have been increasing every year to reach ~130mn paying users for Tencent versus IQIYI’s 100mn. Ad-supported MAUs estimates are not reported, but estimated around 500-600mn MAUs for IQIYI and ~600mn for Tencent. Aside from IQIYI there is also Alibaba owned Youku, MangoTV (owned by a Chinese television network SOE) and Bilibili, who has recently made strides with revamping their premium video offering subscription. Youku is generally thought to be more “tired” and appeals to an older generation, however they are taking up content investment, but nevertheless they seem to lack the talent to identify hit shows that resonate with most Chinese consumers (according to our industry contacts). Bilibili has made several successful series, but they are much more niche and still over index to ACG content (Anime, Comics and Gaming). MangoTV has a few popular series, but is very conservative with their content given their parent company is state-owned, which usually precludes it from having the newest hit shows (which can often be a little edgy). However, what content is allowed to be produced is undergoing changes anyway.

The Chinese SVOD (streaming video on demand) industry went through a fervent period of expansion and unconstrained growth starting in 2014. Tencent Video, IQIYI, and Youku all were trying to rapidly gain market share against each other and would throw lavish salaries out to well known actors in order to produce popular content that could attract users. A TV series cost went up from an average of ~1mn RMB per episode to over 20mn RMB. While this was in part driven by a marked increase in quality of content and the money did help bring more consumer options, the zealous fan culture and exorbitantly paid actors drew the attention of regulatory bodies. In 2018 a salary cap was introduced and further regulations around what kind of content can be shown to the Chinese consumer was rolled out as recently as this year. With this regulatory activity on-going it has tempered the industries momentum. To the positive this has in some ways benefited Tencent Video as they never were known to have the most “edgy” content and as a streaming leader, a more constrained capital flow into the industry would be to their benefit as they do not have to bid up on content as much. However, they did come under scrutiny for the practice of allowing users to pay to get content early (advanced video on demand) and ultimate had to eliminate it, which is unfortunate as it could have been as much as 20-30% of Tencent Video revenues.

Nevertheless, despite the regulatory overhand, the same factors that play out with Netflix are playing out with Tencent Video. That is the more subs they can earn, the larger the user base to amortize content costs over, providing high operating leverage while simultaneously justifying further content spend, which in turn brings in more users and thus drives content cost per user down further. SVOD is very much a scale game and the player who can get the most users can afford to spend the most, which brings the best value prop to each individual consumer. Today Tencent is not only the largest competitor, but also has advantages with access to popular IP through their gaming franchises, Chinese Literature (more on later), and global partnerships.

Their position does give them pricing power, but they largely have decided to not exercise it. Since originally rolling out the service in 2011 they only raised prices for the first time this year, taking prices up ~5 yuan a month or a ~25-30% price increase depending on what package you had (they offer discounts based on monthly, quarter, or annual subs and whether you are a continuing member) and puts it in parity with IQIYI. Leaving excess consumer surplus, as opposed to pricing to the efficient frontier, is a great way to continue to attract and retain customers, which is far more important at this stage of Tencent Video’s maturation than profitability. However, they did charge separately for over-the-top or OTT (TV streaming) capabilities for 100RMB, which is a good solution to take some pricing while keeping their entry level price low through bifurcated their offerings.

Overtime Tencent will continue to raise prices but driving more users to the paid subscription is likely to be the larger growth driver in the interim. With only about a ~20% paid penetration rate among their user base, there is ample opportunity to upsell users.

Below we show what the Tencent Video mobile app looks like.

Below, you can see what it’s like to watch a video. The first two photos show an ad playing, which can only be skipped by VIP members. On the first photo, you can see a second ad at the bottom of the screen. The third photo shows the video playback functionalities like sound and broadcast to a different device.

Tencent Music.

Tencent Music is a subsidiary of Tencent but is also listed separately on the NYSE under the ticker TME.

It is one of the leading online music and audio entertainment platforms in China, operating 5 core products: 1) QQ Music, 2) Kugou Music, 3) Kuwo Music, 4) WeSing, and 5) Ultimate Music. TME’s portfolio of products offer a comprehensive library of music content across licensed, self-produced, and co-produced content, as well as professionally generated videos (music videos, concert recordings, music shows), and user generated content (short singing videos, livestreams, essays).

Tencent Music across all apps has ~850mn MAUs versus their closest competitor, NetEase Music, with 180mn users and Migu Music with around 80mn. As far as paid subscribers goes, NetEase has just 16mn versus Tencent Music’s 81mn (growing +30% y/y). Generally speaking, paid penetration for music is quite low at just ~10% in China. This compares to Spotify which has 380mn MAUs globally with 45% of those users paid subscribers so paid penetration in China clearly has room to improve overtime.

Helping Tencent Music gain such dominance was the fact that it had exclusive rights to 80% of all available music in the market including deals with the big 3 labels: Universal Music, Sony Music Entertainment, and Warner Music Group. However with the recent anti-trust scrutiny, the SAMR ordered them to forgo their exclusive rights to their music catalogs, so they can no longer restrict competitors from access the labels catologs or receive above market royalties for sub-licensing the rights (For example, Tencent sub-licenses Universal’s Catalog to NetEase at a royalty rate for above global standards). While forging their exclusive rights isn’t a positive, they are dominant enough that it is unlikely to have a devastating effect to their business, especially since they have a lot more social functionality built into there apps. Nevertheless, competition could pick up as a result.

Tencent Music is also well positioned to continue to grow subs as more Chinese upgrade from the ad-loaded experience to an ad-free one. Their multi-app approach with 4 out of the top 5 music apps (including the #1, #2 and #3 spots), positions Tencent very well for when users do upgrade to a paid experience, which we think will continue to happen slowly overtime. In total they have four main apps: QQ Music, Kugou, Kuwo, and WeSing.These apps differ in some functionality like live streaming, fan groups, and karaoke which all create more of a community feel and increase engagement.

QQ Music was established in 2005 and focuses primarily on professionally produced music, similar to Spotify. Kuguo focuses on more UGC and helps new artists get discovered. They also have livestreaming and karaoke. Are far as music goes, Kuwo is a mix somewhere between QQ Music and Kuguo with both professional music and UGC, but Kuwo is actually more known for hosting radio and podcasts. WeSing is a karaoke-focused social network with the ability to record and remix signing videos.

Swipe through the below photos to get a sense of the QQ Music platform. The 5 tabs are: 1) Home, 2) Radio, 3) Music Videos, 4) Community, 5) Profile. The last three photos are general UI photos.