*Please see our disclaimers at the bottom of the page and our full disclaimer here. By using our website, you acknowledge you have read our disclaimers and agree to our terms of use.

**Thank you to all of our subscribers! We hope you enjoy our Grab piece and please join our Discord to continue the conversation!

***Notes: 1) Grab’s accounting treatment has led to revenues being negative in certain periods. This means many revenue growth rates could look weird; we tried to adjust them so a smaller loss (or a negative to a positive) doesn’t show up as a negative rate, but nevertheless you should probably just ignore growth rates off of negative bases as they can be misleading. 2) SEA refers to Southeast Asia, not Sea Limited (SE). 3) For this deep dive, we interviewed ~100 Indonesian consumers and many industry experts. We only focused on Indonesia because it is the largest market in SEA and one of the most contentious for Grab. We hope you enjoy!

Background History.

The seeds of what would become Grab were planted in 2011 at a Harvard Business School entrepreneurship class. Anthony Tan, a Scion of one of Malaysia’s wealthiest families, teamed up with Tan Hooi Ling, who also was Malaysian, but from a far more modest background. With the idea of “double bottom line” businesses—that is those that focus on doing good as well as making profits—ringing in their heads from a recent course, Tan Hooi Ling knew the problem she wanted to solve.

Prior to HBS, Tan Hooi Ling did a stint in consulting at McKinsey in Malaysia. Working late nights, she was scared she’d fall asleep driving home, but the alternative was taking a cab which meant in the best-case scenario subjecting herself to aggressive driving and the virtual certainty she would be price gouged for the dirty cab ride home with any protest to be met by belligerence. However, as a young woman riding alone at the dead of night in an unknown man’s car, there were far worse outcomes than overpaying. The concerns were so salient that Tan Hooi Ling and her mother had to create their own safety system. Ling would text her mother the cab’s license plate in an obvious manner such that the cab driver knew she did, and then message her half-asleep mother when she passed agreed-upon markers.

While Tan Hooi Ling’s interest in ride-hail stemmed from personal experience, Anthony Tan’s interest stemmed from a business one. Prior to starting Grab, he had spent a summer trying to run a taxi service, which made him intimately aware of the issues dispatchers faced. Coupled with the fact that he was in the process of rediscovering his Christian faith, he instantly gravitated towards the idea, as it serves society while (*hopefully*) also being profitable.

The two whipped up a business plan to start a ride-hailing service in Malaysia for their Entrepreneurship class and later won second place and $25k in the HBS New Venture Competition in 2011. But more than the money, the pair walked away with invaluable feedback from the judges: focusing on a market like Malaysia was too limiting.

After graduating, Anthony, who had resolved to create a “double bottom line” business, ignored his family’s desires for him to join their automotive empire, and instead opted to launch the business with the plan they created. With the prize money and some help from Anthony’s family, the pair released MyTeksi, the precursor to GrabTaxi, in June 2012. They stood outside of gas stations in Malaysia and passed out snacks to cab drivers before trying to convince them to download their app, promising more rides and more money. While the company saw some early traction, Tan Hooi Ling chose to return to McKinsey, in part due to an obligation to the company for sponsoring her MBA. While at McKinsey though, Tan Hooi Ling stayed close to the company, using her vacations to help Anthony however she could, including a two-week “vacation”, where she visited 5 different SEA countries and surveyed the landscape. (She returned full time as COO in 2015, worried that Anthony would quite literally work himself to death without her–Anthony was hospitalized at one point after collapsing, seemingly from lack of sleep).

After Tan Hooi Ling returned to McKinsey and on the heels of increased competition, Anthony rapidly expanded into new markets. Rebranding to a more generic name in GrabTaxi, they launched in Singapore in 2013, the same year Uber entered the market. Grab then rolled out operations in The Philippines, Thailand, Indonesia, and Vietnam over the next couple years, usually a few months before Uber did. Whereas Uber “copy and pasted” their model in each new market, Grab localized each countries’ offerings with different products. In Malaysia, they originally focused on just taxi cars since that was a popular means of transit there, but in Vietnam & Indonesia they launched GrabBike for motorcycle taxis (referred to as Ojek) and GrabTuktuk (3 wheel vehicles) in Thailand. Critically, Uber restricted payments to just digital means, seemingly not realizing that most consumers don’t have credit or debit cards. Grab capitalized on this blunder by offering options for cash payments. Contrary to what analysts expected, Grab’s fiercest competition came not from the very well-funded ride-hail leader out of the U.S., but from a local start-up, and in an odd coincidence of history, one of Anthony Tan’s HBS classmates.

While at Harvard, Nadiem Makarim virtually operated a call center in Indonesia that connected callers to Ojeks for delivery and passenger transport by forwarding information to a small fleet of drivers. Called GoJek in an ode to the motorcycle deliverymen (Ojek), they launched their service in Indonesia in 2010, but didn’t roll out an app until 2014. This delayed launch (likely due to outsourcing the app’s original development given GoJek’s limited tech abilities at the time) was fortuitous for Grab, who also would roll out an app in Indonesia in the same year, which limited GoJek’s first mover advantage. While GoJek was slow to the mobile app game, they were much quicker at rolling out a slew of other services. Vying for the position of SEA’s first Superapp, they added a slew of services: GoGlam (on demand makeup), GoLaundy, GoFix (air condition repair), GoClean (house cleaning), GoMassage, and others. While most of these would eventually be discontinued, it showed GoJeks desire to fill as many everyday needs of the consumer by testing many different products quickly to see what resonates and cutting those that don’t. While GoJek was rapidly growing the Indonesian market and expanded to other countries, Grab was a ruthless competitor with an ability to sustain losses thanks to a $250 million investment from Softbank in 2014. While Grab battled GoJek with subsidies, they fought the better funded Uber with local knowledge. A telling story was when Uber brought their Ice Cream Day promotion to Malaysia, which gave users the opportunity for free ice cream, they instead disappointed consumers by the delivering ice cream that melted in transit from the heat and slow traffic. Grab responded by rolling out a Durians promotion, a treat that Malaysian’s tended to desire more anyway. The smelly fruit, illegal to carry in many public places, had to be delivered in specially designed packages for this campaign, but was a clear marketing success and continues to this day. Eventually, Uber would cede the market to the local competitors, selling their SEA operations to Grab in 2018 for a 27.5% stake in the combined company.

Back in 2016 though, one of the most important offerings Gojek introduced was their payment service and eWallet, GoPay. Recognizing the opportunity and rationale behind the Superapp, Anthony Tan launched GrabPay in 2017 and invested in Indonesia’s leading fintech, OVO (later taking a majority stake). This prompted Makarim to say “It’s really interesting that Grab has started to try to take that word away from us”, referring to the word “Superapp”, “I’m like, ‘Excuse me?’ You spend the first years of your life copying Uber? And then the next three years of your life copying Go-Jek?”. The Superapp was hardly GoJek’s invention though, with Alibaba and Tencent having been promoting that concept for years. Either way, at the end of the day, execution is all that matters. Grab took the ride-hail lead in GoJek’s home market with ~60-65% market share. Having beaten Uber and now the leading regional market player, Grab has started looking to new services with deliveries, GrabKitchen (cloud kitchens), insurance, wealth management, lending, GrabAds, and an enterprise platform. However, they continue to butt heads with a formidable competitor in GoJek, and more recently Sea, with AirPay/ SeaMoney and ShopeeFood. While this market looks like it is settling, there is a risk that it could tip towards another player and Grab could lose their leading position. Aware of their tenuous lead and the ebullient capital markets, Grab decided to raise over $4.5bn to restock their war chest and attack new opportunities. In April 2021, Altimeter, a tech-focused crossover fund, announced that they would take Grab public via their SPAC, Altimeter Growth Corp (NASDAQ: AGC), in the largest SPAC deal to date. The deal values Grab at $40bn, making it one of SEA’s largest companies. The company has yet to de-SPAC.

The Business.

At a high level, you can think of Grab as a combination of Didi, DoorDash, and Ant Financial. In most of their markets, they are a leading ride-hail player, a #1 or #2 food delivery provider, and a top ePayment enabler. While they started with just ride-hailing, they have consistently added new services to their app to drive frequency and user reliance with the goal of becoming SEA’s Superapp. Today, they have 25mn monthly transacting users (MTUs) that each spend ~$600 in GMV on their platform. This yields Grab a 2Q21 run-rate GMV of ~$15bn, +22% from their 2020 GMV of $12.5bn. We will pick up later on the rationale behind, and their success with, the Superapp concept.

Grab operates four segments: 1) Deliveries, 2) Mobility, 3) Financial Services, 4) Enterprise and New Initiatives. Given accounting treatments of subsidies and varying stages of monetization, it isn’t straightforward to compare their revenues. Instead, we show their GMVs below. (But never fear, dedicated reader, for we have an accounting section that will clarify all of this!) You will see the deliveries segment is the largest today, following by financial services, and then mobility. This mixshift has been materially impacted by Covid though, with LTM mobility GMV being 85% higher than in 2019.

Below, we touch upon their offerings by segment. We will go further in depth when we dive into each segment individually.

1) Deliveries. These services are generally similar to global peers like Doordash, Just Eats, and Meituan. Full offerings are listed below. We will touch on how they fair versus competition and some unique aspects of their offerings in the delivery segment.

2) Mobility. This is similar to peers like Didi, Uber, and Gojek, although they have far more options that cater to local transportation idiosyncrasies.

3) Financial Services. Their financial services include GrabPay, a leading digital payment option in SEA, and a slew of other financial products. More on these later.

4) Enterprise and new initiatives. Two of the biggest initiatives here are GrabAds and GrabDefense. GrabAds is their advertising platform that allows merchants to promote listings within GrabFood or GrabMart. They also allow merchants to buy banner ads through the app. Lastly, they have offline advertising that utilizes their vehicle network for car wraps and in-car back of seat ads.

GrabDefense is their self-developed antifraud service that they are rolling out to merchants. With the digitization of the economy, digital fraud has become more common. To combat that, Grab has been rolling out a suite of tools fight fraud. There are nice synergies here with their Grab Financial Solutions, as many of the antifraud capabilities were likely already developed to reduce payment fraud. This offering could also help embed Grab deeper with MSMBs (micro, small, medium businesses) and could become a customer acquisition tool for their other financial and delivery offerings.

Lastly, Grab is also experimenting with flights, hotels, and other subscription services from partners offered in app. So long as consumers continue to use their app, there will be the opportunity to add other services to cross-sell.

Superapp Strategy.

Before we dive into each segment in more detail, we wanted to zoom out and give an overview of what Grab’s overall business strategy is with all of these different services.

Grab refers to themself as a Superapp, a category that was arguably created by Alibaba’s Ant Financial but where Tencent’s WeChat is clearly the gold standard. WeChat started as just a messaging app, but evolved beyond just an app into a sort of operating system with mini programs (like an app store), payment capabilities (think ApplePay), and extremely high penetration to the point that almost every Chinese-speaking smartphone user has the app downloaded. In fact, it is such a powerful app that it actually weakened Apple’s grip on the smartphone market since users could easily port their WeChat account with all of their contacts between devices easily. When many users are pressed between only using WeChat versus all other apps, they opt for the former: that is how versatile and instrumental to everyday life WeChat is in China. We wanted to be clear that this is the perspective coloring how we judge other “Superapps”. A real Superapp is self-contained and can offer (directly or through partners) most of the things you would need over the normal course of a day. The Superapp effectively acts as a low-cost funnel of future customer acquisition for different offerings by keeping customers captive to a slew of everyday services. The high frequency nature of these “everyday services” keeps consumer churn de minis. Since the consumer already uses the app regularly, getting consumer adoption for a new service is as simple as promoting it on the miniprograms page.

There are really three core aspects that are essential to a Superapp: 1) high frequency to drive more “cross sell” opportunities, 2) essential services to reduce churn, 3) built in means to add new future services in a way that feels natural. The high frequency, essential services are like a foundation that everything else is built off of. WeChat built their foundation off of messaging and strengthened their foundation with payment and other social media. As you can imagine, compared to this standard, almost every other “Superapp” falls far short, but we do want to give Grab credit for what they have built, as their claims of being a Superapp are much more substantiated than others.

As shown above, Grab is trying to use ride hail, delivery, and eWallet as their foundation. There are several issues with this approach: 1) ride hail and food delivery are notorious for promiscuous customers, making for a shaky foundation, 2) eWallet is better, but with users often having multiple wallets, it is unclear how much of a grip on the consumer this is. To be critical, Grab is tying together services with weak grasps on the customer individually in hopes that the sum is greater than the parts. The question Grab is trying to answer is– can you combine a bunch of low loyalty services to create higher consumer loyalty? As you can see below, the answer seems to be yes, this strategy is defensible.

The more services a user adopts on the Grab app, the higher their retention. This is critical when considering the health of their foundation. Without users that are captive to Grab, their flywheel will eventually fall apart. While we would prefer to see a sturdier foundation with something like messaging services that are harder to replicate and do not suffer from the same degree of competition, it is encouraging to see user health trending upwards.

Another aspect to Grab that makes it distinct from WeChat is that all of their core offerings are proprietary. Of course, you cannot access Grab’s delivery, ride-hail network, or eWallet outside of the Grab app. This means that their individual businesses’ competitive position will either empower Grab as a more convincing Superapp or impede them. For example, if they cannot present a convincing delivery experience due to a lack of selection, delivery speed, or price, then a user can simply download another delivery app and place their order there. Losing customers like this creates cracks in Grab’s foundation and weakens their ability to sell other services. The same way that increasing the number of offerings a user adopts reduces churn, a user utilizing fewer offerings will increase churn. This means that in order to keep usage trending in the right direction, Grab cannot shirk on any of their offerings. If they do, they not only lose that direct business, but the lifetime value of the consumer drops across all of their other services. What can be a strength when executed well can quickly turn into a weakness. This is concerning for a company whose Superapp is built on three of the most notoriously competitive businesses: ride hail, food delivery, and digital payments. However, as we will go through later, they have executed well thus far. On one hand, you can argue that Grab is in a very precarious position because their core businesses are highly competitive and that they are at risk of a deteriorating flywheel. On the other hand, their leading positions in each of the segments suggests that management is highly competent and there is unlikely to be tougher competition in the future than there was in the past (maybe not though!). And while we may have been critical of building a Superapp off of such tough industries, their strategy is showing signs of success with over of half of their users now using multiple offerings. In short, this isn’t how someone would go about building a Superapp from a blank sheet of paper, but if you started with a ride-hailing operation, then turning it into a Superapp is the best thing you could do with it since it solves the low loyalty and low margin issues pervasive to ride-hail (more on this shortly).

While we noted some of the downsides of building a Superapp’s foundation off of proprietary services that are highly competitive, the flip side is that a unique offering or better service can earn you new customers that you can then push into your other services. This is a model that when done well can become a flywheel with each service feeding usage for another. Then, layering on financial services with rewards can help strengthen ecosystem lock. However, Grab is especially interesting because there is the flywheel of the Superapp (which is the customer acquisition and churn reduction benefits) and the flywheel of each individual business, each of which can feed off of the other.

The network effects within delivery and mobility are well understood with more users bringing in more drivers/delivery partners, which reduces wait times which attracts more users. The cross-sell benefits of owning both delivery and mobility platforms is also well acknowledged by the likes of Uber and GoJek, as passengers can later become food delivery customers. But there is another, more underappreciated factor. These businesses can also cross-seed each other, whereby drivers can become delivery people when work is slow. For gig economy apps, having a robust network of workers is essential to quickly and efficiently serving customers and making sure the workers will always have enough work is a great way to ensure that they don’t look to other platforms for work. This was very salient during the beginnings of the Covid pandemic when ride-hail demand plummeted and food delivery demand soared. Grab was able to quickly transition 237,000 driver-partners from ride-hailing to to food and package delivery. If Grab didn’t have the deliveries segment, they could have lost a material portion of these partners forever. So being able to volley between different services that fluctuate in demand allows Grab to keep their huge network of gig workers by offering them enough work to make a living. Thus, there is a benefit of having multiple “gig worker”-run platforms from the partner side as well as consumer side. Gojek has actually exploited this advantage more than Grab thus far by adding more categories of services.

So, while Grab is reinforcing their Superapp foundation by improving the offerings of each business and cross adoption of multiple services, they still are in early innings of monetizing that foundation. Meituan is known for first wanting to dominant high frequency, low margin services (food delivery) to keep platform health strong and then monetizing with low frequency, high margin services (like travel). Today Grab hasn’t really moved up from building the foundation phase to the pure monetization aspect yet. Some of the pieces are there, like advertising and a suite of financial products, that are generating some revenue, but it still is early innings. The focus for Grab is still rebaring their Superapp against GoJek and to an extent SE, but once the foundation is sturdy there is ample opportunity to monetize their consumer lock by cross-selling consumers into a slew of new and more profitable products. So again, if you set out to design a Superapp you probably wouldn’t want to start with a cutthroat business like ride-hail, but if you started with a ride-hail business then a Superapp is the best strategy to address all of the weakness of that business model. Furthermore, if it works, like it is with Grab then it becomes harder to compete against them.

Accounting.

There are a few accounting terminology idiosyncrasies in how Grab reports which result in negative revenues in some circumstances. While we are not a fan of some their non-IFRS accounting creations, Grab does provide enough info that we can look at the financials in the way we think makes the most sense. In specific, we think their “Adjusted Net Sales” figure is misleading and doesn’t make much sense. In short though, if you don’t get anything else from this, remember that (1) they net all partner payments and partner & consumer incentives against revenues (unlike Didi) and (2) we will refer to take-rate as gross billings, which is before any incentives, over GMV and (3) net take-rate at revenue, which is after all incentives, over GMV. So, if partner payments and partner & consumer incentives are greater than their fees, they will have negative revenue. This is common because when they start in new markets they often heavily incentivize activity and undercharge for their services. We will dive into their accounting a bit below, as it provides more color on the profitability of their operations even though we ultimately will ignore their accounting creations in our builds. As the exhibit below shows, Grab reports various intermitted steps from GMV to Revenues.

Essentially, they define Adjusted Net Sales as revenues before “excess partner incentives” and consumer incentives. Not including consumer incentives could make sense if these go away over time, but that still seems too aggressive of an assumption to make, especially right now, as even in mature markets we see some subsidizing. The “excess partner incentives” are what we take more issue with because they are ambiguously calculated as any incentive above what they earn from that driver/merchant partner. If we were to be very charitable in our interpretation of this, the idea would be that these “excess” incentives would go away overtime. However, the way they define “excess” incentives implies that they are still counting the revenue from the consumer side (there are fees charged to both partners and consumers) as positive in their adjusted sales figure even if the whole transaction is a net loss. The accounting here isn’t very clear, but our understanding is that, for example, if Grab makes $1 on the partner side and $0.20 cents from the consumer, but pays the partner $1.50 in incentives, then $0.50 of that will be categories as “excess incentives” (the amount over the $1 they made on the partner side) and they may still count the $0.20 cents from the consumer as revenue (not clear). So this entire transaction that lost ($0.30) cents is recorded as either “adjusted net sales” of $0.00 or $0.20. The fact that this is done on a market-by-market basis, though, makes it even harder to conceptualize. Either way, it does not accurately describe the actual economics of the transaction. We can sympathize with the issue of trying to delineate between one-time incentives and reoccurring ones, but this just seems like a poor solution since they are definitionally assuming all of their incentives above what they bring in will eventually be economic. Again, they give us the ability to ignore these designations they make entirely, so we do not want to be overly critical, but seeing management promote and utilize metrics that seem misleading is never a confidence booster. The chart below helps illustrate this graphically. It is also odd that it was presented in the original F4 but removed in the later, amended F4 (we are not sure how common it is for exhibits to change from different F4 editions, but it seemed odd to us).

In the picture above, we see that Grab records partner payments in three different ways: 1) Payments to partners, 2) base partner incentives, and 3) excess partner incentives. Item (1) is their normal disbursement of funds to drivers and merchants; this would be the drivers’ revenue share or the merchants’ revenues. Items (2) and (3) are both incentives that are designed to spur more adoption by drivers and merchants. To reiterate, what makes (3) excess versus (2) is not based on any economic rational but rather because they have designated any incentive over what they bring in as “excessive”. We do not actually know if these are excessive incentives to merchants and partners or necessary to keep their activities ongoing. It actually isn’t even clear what the meaning of a “base incentive” is—it is defined for an output without any specific business justification. As stated, they define it as any incentive up to how much they receive, but how that is a “base incentive” doesn’t seem to make much sense to us. By being a “base incentive”, does that imply it is unlikely to go away? In our Didi piece, we went through lengths to clarify the issue of “growth” vs “maintenance” incentives, which for Grab are denoted as “excess” vs “base”. We feel that the Didi discussion was relevant enough that we have repurposed part of that section for Grab and reprinted it below.

Since partner incentives are sometimes considered “base” or “excessive” on the basis of their P&L impact and not economic rationale, this creates a problem when trying to deduce what their ultimate profitability will be. Ideally, we would want “excessive” incentives to be synonymous with what we will refer to as growth marketing, implying that it will eventually disappear without impacting platform activity (GMV). With many growth companies, marketing is inflated as they spend to take advantage of value creating investment opportunities that do not materialize on the P&L until years later. To illustrate this, consider an investor looking at a SaaS company. A SaaS company spends prodigiously on marketing, knowing that every customer they get is likely to stay for a long time (very low churn and long customer life) and spend more with the platform overtime (spend by cohort increases). Before investors were comfortable with SaaS companies, they complained about how they were always unprofitable and could grow losses on increasing revenues. However, over time, many realized that SaaS companies “invest” through their P&L instead of their cash flow statement. So stripping out the growth investment in marketing (which can be thought of as “excess incentives” in this case) you would see a much more profitable company. This is fair treatment for a SaaS company because their customers seldom churn, so there is almost no “maintenance” marketing that is needed to incentivize them to stay. Contrast that with many consumer companies that sell products in one-off transactions, where marketing can seldom be fully turned off because you have to “re-acquire” the same customer over and over again. This is especially true for Grab as the food delivery and ride-hail spaces are infamous for very high (and often wasteful) subsidies. If you have used ride-hailing or food delivery services, then you likely recall getting push notifications or emails with a coupon incentivizing you to come back to order again—it is not clear if this marketing spend is to habituate you to the service so you become a customer for life or is simply a reoccurring customer acquisition cost that can never be fully eliminated. These are important distinctions to make as we think about the quality of the businesses and what the mature core business’s profitability could look like.

This is to say, the troubles we run into with Grab’s accounting definitions are not just that it isn’t clear what is a “growth” expense that is driving new user growth or what is a “maintenance” expense that is needed to get a user to stay is, but definitionally the fee rate they set dictates that distinction. This does not make sense as whether Grab takes a 3% or 10% take-rate of the order from the merchant would have no bearing on whether the customer returns. While most companies do not make a distinction between growth and maintenance marketing, we are only calling Grab out here because they created a metric that optically seems to address this issue, but really is just obfuscating it in a misleading way. To be fair, Grab does provide more information than many public companies. And again, we can simply ignore this trap of their own creation entirely. However, investors should be critical of any valuation that uses their Adjusted Net Sales figures. With that preamble, we will now dive into each segment.

Deliveries.

Today, deliveries comprise about half of GMV, +86% y/y in 2020 and up another+24% YTD to $6.8bn. Their average take-rate, which we define as gross billings over GMV is approximately ~18%, up from 11% in 2019 when it was a newer business. As you can see below, revenues barely turned positive in 2020 (because incentives were higher than gross revenues) and they are still adjusted segment EBITDA negative, losing ~one penny on every dollar of GMV they service, or ~4 pennies on every dollar they bill for today.

As shown above, their take-rates have been increasing to ~18% from 11% in 2019, which are calculated before incentives. Many newly onboarded restaurants and merchants still receive reduced fees, but with heavy competition it is unclear how much Grab can raise this in the interim. Pushing their on-platform advertising services, which allows a restaurant to promote their food with special placement, will help Grab increase their take-rate. But it also worth mentioning that they aren’t actually getting a lot of this “take-rate”, with 85% of it being returned to merchants in the form of incentives, which is actually an improvement. Their incentives as a % of take-rate just recently dropped below 100% (which is another way of saying revenues turned positive). We will need to see their incentive rate as a % of take-rate continue to drop if we are to believe they will ever reach meaningful profitability. Below, we show graphically how much of their take-rate has been remitted back to the merchants, drivers, and consumers in the form of incentives. While they have a healthy gross take-rate, after incentives it is an underwhelming 2.6%. We will dive deeper into their profitability with their unit economics momentarily.

As shown below, increasing GMV has cut losses, but they still aren’t segment profitable (which doesn’t even include corporate overhead, SBC, or D&A). They need to cut incentives and increase their net take-rate if they want to reach meaningful profitability.

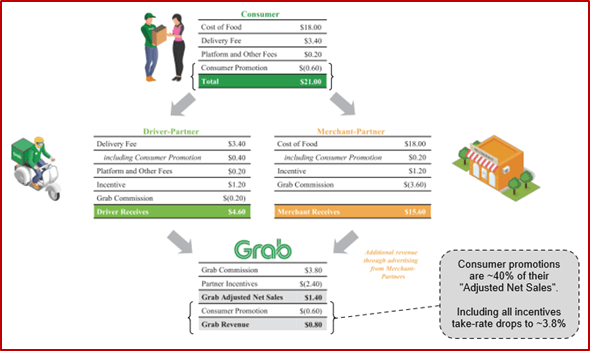

The unit economics illustration below shows that on a $21.60 AOV, Grab hopes to make $3.80 (17.5% take-rate) before incentives, or $1.40 (6.4% take-rate) after partner incentives but before consumer incentives. It is interesting to note that even in their unit economic sketch, they are showing 63% of the take-rate being rebated to partners in the form of incentives. This means that Grab believes they have a limited ability to cut their incentives from where they sit today. Given competition, it seems unlikely that they can materially raise their fees to either the consumers or the merchants, so this is unlikely to ever be a meaningful lever of profit growth. In the bottom left of the slide, they call out advertising as a source of revenue; we think this will eventually represent materially all the profit their deliveries platform makes, which we will show in our build.

Interestingly, they also edited this slide in the amended version of the F4 to include the consumer incentive. This helps highlight one of the issues we identified with the adjusted net sales metric, which doesn’t include consumer incentives. If we include the $0.60 consumer promotion, Grab’s revenue drops to $0.80, or just ~3.8% of order value. We also take this to mean that Grab’s very deliberate inclusion of consumer promotions in this unit economic sketch means they are unlikely to disappear, and that we should include them in our forecast assumptions.

GrabKitchen, launched in 2019, is a cloud/dark kitchen concept owned by Grab. For those new to the terminology, a dark kitchen (or cloud kitchen) is a commercial kitchen that does not have a physical storefront for guest to dine in and exclusively receives orders from food delivery apps. To illustrate, a merchant who wants to open a restaurant would rent kitchen space directly from Grab, paying only monthly fees for the right to use the space that comes furnished with kitchen equipment basics. The benefit to the merchant is it is lower commitment with less upfront costs, and since Grab has already vetted the location, the merchant can be assured that it is in close enough proximity to their delivery customers. Grab will use the data they have from their delivery customers to find underserved pockets that are lacking in options or specific cuisines. The GrabKitchen is unique in that since they compile 8-15 different restaurants in the same location, a consumer can order from multiple different vendors in the same delivery order.

From Grab’s perspective, it does two important things: 1) it co-locates vendors in close proximity—the same venue (!)—which enables order batching and grouping which drives delivery efficiency, 2) creates exclusive supply that is not available on other platforms nor easily ported. This creates some insulation from Grab’s competitors and is important to think through. When we talk about ecommerce companies, we emphasize fulfillment capabilities because that creates exclusive supply that is ready-to-ship in the ecommerce provider’s warehouse. Thus, fulfillment not only means exclusivity, but also logistics efficiency. The combination of better logistics and exclusive inventory creates a flywheel that makes it very tough for competitors to catch up to. This is essentially what Grab is creating with their GrabKitchens. The food vendors are only available on Grabs platform, and it simultaneously increases Grab’s logistics capabilities by having many orders in one location with a dedicated pick-up lane for the delivery drivers.

In an interesting twist, and a shift back to a more normal restaurant concept, they are now also experimenting with having a dine-in area. Under this model, a consumer can either place an order for pick up and eat there, or in some cases order at the venue through a traditional POS system. There are a few notable things about this in-person dining strategy. First, it acts as advertising for their Grab Delivery operation, and to a lesser degree, their other apps. Second, they can push adoption of GrabPay (OVO in Indonesia).

Today, they have over 80 kitchens with the vast majority of them in Indonesia and are continuing to roll them out. They are also forging partnerships with various local chains that are in some cases utilizing the cloud kitchens to grow instead of opening more physical stores. An Indonesian restaurant with a single location—Nasi Goreng Maut Seafood—expanded to become a “virtual chain” with their subsequent 5 locations all in GrabKitchens. Providing the infrastructure for food vendors to grow is a very interesting strategic position to be in as they are becoming critical to the restaurant’s operations and the better position they have in the value chain, the less competition they will have and the more profitable they can ultimately become. Exactly how they monetize these Kitchens today isn’t entirely clear though, and the contractual terms seem to differ merchant by merchant. In some cases, they offer merchants free space in exchange for commissions on sales. But this seems more like a promotion to build merchant occupancy. We do not expect them to try to make each Kitchen standalone profitable (although they could be), but rather focus on making their whole delivery segment a better value prop to the consumer that can eventually allow them to eliminate subsidies and possibly even raise delivery platform fees. It is also interesting to think about what would happen if they slipped grocery options and other FMCG products into their GrabKitchens, which could allow more delivery efficiencies. Perhaps, after delivering a hot meal to customer, a driver could drop off paper towels and some produce at a nearby house. This could work since the latter delivery is less time sensitive but still increases deliveries per hour. However, not to get ahead of ourselves, it still isn’t prevalent enough to insulate themselves from competition, which has been fierce.

Generally, speaking Grab and Gojek are seen as substitutable with many consumers (~54% in our Indonesian survey) having both on their phones . There are a few local competitors, but we can by and large ignore them. In our consumer survey, which focused just on Indonesia, the largest and most competitive market in South East Asia, only ~5% of results pertained to delivery services other than Grab and GoJek, with one important exception we will go over momentarily.

While selection across the platforms is similar, Grab tends to have more large chain partnerships and Gojek tends to overindex more to small local merchants. However, many restaurants are on both platforms and both companies continue to add more food vendors daily. Grab’s cloud kitchens are an interesting competitive factor as they create exclusive supply, but Gojek was quick to mirror that effort and has announced that they will open >100 cloud kitchens, so its likely this effort leaves them both in the same competitive position rather differentiates either (each will have some exclusive food vendors and ~60% of consumers have both apps to check what they want). So it seems that Grab and Gojek will have fairly similar food delivery services and will be competing more with their Superapp ecosystem to differentiate themselves. However, with most users already having a foot in each ecosystem, it is not quite the consumer lock that would confer any significant advantages to either.

While it is true that the more a user uses one platform vs the others the more they are likely to keep using it, they are still willing to transverse between them to see if one has better pricing, different selection, or faster delivery (92% of users said they check multiple platforms before ordering). It is true that some users will become Grab loyalists, but others will be Gojek loyalists, and earning the continual business of the large swath of indifferent customers in the middle.

In their F4, Grab quotes Euromonitor 2020 data that puts Grab’s regional market share (total SEA) in online food delivery at 50% and says the next closest competitor is at 20%. This seems incorrect to us. We have seen various estimates that did put Grab food delivery around 50% with +/- 10% varied by market, however it seems plainly wrong to say that Grab is 2.5x better than the next player. In our Indonesia survey (which is responsible for probably close to half of all regional activity) we actually saw that Gojek was slightly more popular with 75% of consumers using it vs 63% for Grab. The other issue is that after Covid, market share really moved around and it isn’t totally clear how it settled out today. At a high level, we assume that Grab is either tied with Gojek or has a nonconsequential lead over them in the entire SEA region, with the likelihood that Gojek leads in Indonesia. Not having more granular data like frequency and AOV means we cannot draw a linear conclusion from app usage to market share though. Nevertheless, things are changing rapidly.

The exception to Grab’s and Gojek’s clear dominance is a new entrant, ShopeeFood. Sea Limited launched their food delivery services in Indonesia in March of 2021 and has already seen impressive progress. With 38% of our surveyed consumers having said that they used ShopeeFood in the past 6 months and of those ~75% (29% in total) still regard it a “normal use” food delivery app. We are making this comment to delineate between apps that are used for large promotions and those that have entered habit (implying incentives can eventually be cut). ShopeeFood’s high returning customer rate suggests some success, but it won’t be clear until promos are curtailed. SE is using their Shopee ecommerce platform to push usage to their ShopeeFood delivery service with promotions for free delivery and discounted food as well as tie ins with Shopee Coins (discounts for orders) when the user uses ShopeePay.

What is interesting, and most concerning with SE, is that they are not just attacking one vertical, but rather attacking Grab and Gojek’s entire ecosystem. This is why it makes it a much more formidable competitor, especially when you consider their large user base from Free Fire that they can promote through for free, as well as the priority placement in the Shopee ecommerce app. ShopeePay, as we’ve mentioned in several of our prior write-ups, isn’t a top player in digital finance yet, but that could very well change as activity across their offerings increase with loyalty programs. The driver side of their network is definitely weaker than Grab and Gojek who can cross-seed with Mobility workers and have higher food demand to service. However, this doesn’t seem like much of a moat for Grab and Gojek as one-time bonuses are often enough to convince drivers to try a new service. The question is more whether the demand can sustain drivers full work desires, but they can help solve for this by only slowly ramping up driver partners. Also, recall that food delivery only relies on local network effects, so they can attack one market at a time.

Grab and Gojek still have a wider selection, and Grab has partnerships with certain chains, but most restaurants wouldn’t resist adding another delivery platform that can provide them incremental demand while decreasing their reliance on any one platform. To be sure, it will be a slog for ShopeeFood to sign up all of these merchants and slowly seed their driver partner network while simultaneously subsidizing consumer activity, but Sea has proven themselves to be a highly capable competitor with exceptional execution. If Sea were to succeed here, they would not only hurt Gojek’s and Grab’s food delivery business, but also put a dent in their on-going expansion into quick local commerce delivery and their financial services. Shopee’s relationship with merchants through their ecommerce platform is also likely to mean that they will be able to offer delivery services for local merchants who are already onboarded to their Shopee platform. While we don’t know how big Grab’s or Gojek’s non-food delivery business is today, it is definitely a big part of the growth opportunity that now looks even harder to keep winning in. Grab has had limited partnerships with Lazada in the past whereby users would purchase select items on the Lazada website and Grab would delivery them in an ~hour. However, Gojek will have Tokopedia (pending their merger) to help support that kind of commerce. It will be interesting to see how much Gojek can embed their delivery network into Tokopedia purchases. Sea, of course, has the more popular Shopee platform that they can do something similar with after they build out their driver network. In addition to local commerce, grocery will be the next battleground.

This is all to say, just as Grab and Gojek probably thought market share was settling and they could focus more on streamlining operations and profitability, Shopee has darted those plans and they will have to turn back up the competitive intensity to maintain their existing customers. It’s also worth noting that the degree of success ShopeeFood has enjoyed in such a short time makes us reconsider how formidable of an advantage a three-sided network really is without some level of consumer lock-in (think a subscription service like DashPass that entitles the user to free delivery or exclusive selection either through partnership or something like GrabKitchen). With ShopeeFood also in Vietnam and rolling out Malaysia, Thailand and others, the range of outcomes regarding Grab’s mature market share and profitability have just widened. In our build, we will show a wide range of potential values, but we defer to the reader as to what you feel comfortable assuming.

Mobility.

Mobility is Grab’s second biggest segment today, given they are not really monetizing their financial offerings yet. As you see below, GMV still hasn’t recovered from their pre-pandemic levels of $5.7bn. However, while their take-rates have remained fairly steady at ~22%, the portion of that take-rate that they actually keep (i.e. take-rate after incentives) has jumped. In 2019, 99% of their take-rate was rebated back in the form of incentives, giving them revenue of just $9mn (!) on $5.7bn of GMV. Over the past year, they have materially rolled back incentives to just 24% of their take-rate and they are showing real revenues of ~$500mn on a LTM basis.

We do not expect Grab to be able to raise their take-rate, and note that it is also possible they are under-incentivizing GMV compared to a non-Covid environment. Our line of reasoning is that there is a selection bias of people in that those who are using ride-hail today are largely those who do not have other good options to travel with, and thus they do not need to be incentivized to use ride hail. If you are scared of getting Covid or giving it to someone in your family, a few bucks off of a ride isn’t going to change your decision to ride-hail over public transit or drive your own car over ride-hail. Thus, the people who are using their mobility services today are largely those who picked it on other nonmonetary factors, and so Grab was able to cut their incentives materially. It is not clear whether in the future they will have to take on more subsidies to return to pre-pandemic GMV levels or if they even have a desire to do that. Perhaps they would prefer a smaller but more profitable business to chasing GMV growth. However, if we look to their illustrative unit economics sketch below, it seems that they believe incentives are too low today as Grab pegs incentives as a % of their take-rate closer to 70% vs 24% today. At that level of incentive, it is questionable whether they will be able to reach more than mediocre profitability, if at all.

Competition today is essentially just between Grab and Gojek in the mobility space. There are a couple newer entrants like Maxim that came up in our surveys, but we are very comfortable saying Grab and GoJek are in a league of their own in ride-hail. Our Indonesia survey showed 72% of people use Grab and 81% use GoJek, with lots of overlap. Maxim (a recent Russian ride-hail upstart) has reached 13% thanks to heavy promo use and “other” was 4%.

While Gojek originally focused more on two-wheel transportation and Grab started with four-wheel, they both now have comprehensive offerings and a driver network that covers all options, so there will not be a big differentiator there. Pricing is also very similar and with ~90% of our consumers saying they cross check apps for price (and travel time), it is unlikely Grab will ever be able to raise pricing materially.

Perhaps Grab and Gojek could raise pricing if they moved in concert, but they each seem to be more focused on increasing adoption than increasing fees on existing users. This is because ride-hail is part of the “foundation” of their Superapps, and they don’t want to turn consumers off. (We highly recommend anyone who is curious about ride-hailing competitive dynamics and what is needed for the business model to work most efficiently read our Didi piece, where we went to great lengths to explain all of the factors that are relevant to ride-hail). Today, Grab believes that they have a ~71% market share position as of 2020 with the next closest competitor having 15%. This diverges most notably in Indonesia, which is Gojek’s strongest market, but across all of SEA this could be directionally accurate (still feels a bit high to us, but we do not have many other regional estimates to back us up).

Grab’s opportunity is not taking market share, but simply holding their share as the market grows. If you believe the estimates Grab quotes in their F4, then ride-hailing will return to pre-pandemic levels in 2023 and then more than double in 3 years. This is a ~14% CAGR from their peak GMV levels in 2019. While SEA is fairly spread out geographically, roughly ~45% of the ~675mn people live in urban areas where ride-hail is an appropriate means of transit. The bull case story is something like public infrastructure is inadequate, car ownership is expensive, and ride-hail can solve everyone’s transit issues while ameliorating traffic. However, as we showed in our Didi piece, many consumers are price sensitive to ride hail and prefer private transportation for other reasons. Additionally, public infrastructure can improve and likely will as the region continues to develop. Also, increasing incomes have usually led to more car and private vehicle ownership, regardless of whether that is strictly “rationale”. Our personal view is that ride-hail will continue to grow as it is more convenient in many circumstances, but is unlikely to become the primary means of transit for too many more people anytime soon. We can even give Grab full credit for their 2025 TAM estimates, but it doesn’t really change the investment thesis as adding more GMV of low margin dollars creates very limited value.

The more important aspect is qualitative, which is whether ride-hail can act as a wide funnel to get more users into their ecosystem and then eventually pushed towards more other profitable offerings. With only ~24.7mn monthly transacting users, which is down ~5mn from their peak in 2019, suggests that ride-hail has been the most important business in growing their ecosystem. When ride-hail volumes dipped because of the pandemic, they lost ~17% of their user base. This is critical to note, because it shows that ride-hail is the focal pillar of their Superapp foundation and losing it has materially affected them. Grab having deliveries has prevented their entire business from unraveling from the pandamic, but they still have fewer monthly transacting users than 18 months ago. It is possible that this trend doesn’t reverse until Covid concerns are allayed, but it also possible that the ride-hail business has been crippled for some time, especially with the rise of work from home (assuming that Grab over-indexes to wealthier users who are more likely to have this as an option).

Without a clear path to ride-hail fully recovering or evidence that deliveries or financial services can grow users, we would be worried about the growth prospects of Grab’s ecosystem. We don’t have quarterly info for every quarter, but from the disclosures we do have, we can see that MTUs dropped to as low as 19.3mn in 2Q20, the heart of the pandemic, and went back up to 24.7mn in 2Q21. This suggests that their Delivery segment was vital to stabilizing the platform and recovering some of the lost users, although they still haven’t fully made up for their Covid user losses (2019 MTUs were 29.2mn). One line of thinking would be that when Covid fades, their ride-hail operations can rapidly help them grow their user ecosystem, but that could also come at the cost of losing delivery customers.

These dynamics make it very hard to figure out user growth trajectory. We estimate Shopee has around ~80mn buyers in SEA (see our last update here) and given Didi’s 377mn active users in China (~25% of population), we were surprised at how low Grab’s penetration rate was (~4% at peak). An optimist will say that this is the opportunity, but we would express hesitation as it is very hard to predict novel new use cases and when the growth runway will flame out. It is just as likely that, for whatever reason, ride-hailing isn’t as strong of a value prop (China restricts car ownership for example or motorcycle ownership is cheap enough). In our build we will give Grab the benefit of the doubt that they can achieve growth in a growing TAM, but an investor should really think about how aggressive such an assumption is.

Financial Services.

Financial services just recently became revenue positive with LTM revenues of $23mn, illustrating how they have not really started monetizing their services here and have had to heavily incentivize usage. Grab reports TPV before intercompany transaction eliminations and after eliminations as GMV. As seen below, this segment is still losing money. TPV is still growing through the pandemic to ~$10.4bn on a LTM basis, which equates to a ~22% 18-month compounded growth rate. GMV grew ~10% over that same 18-month period, suggesting that on-platform payment activity is growing faster than off platform.

Incentives as % of GMV were 7% in 2019 and LTM have dropped to 1.7%. This is still very high when considering most payment services have regulated fees. In Indonesia, for instance, the government has capped take-rates to 70bps on a transaction under the QRIS (Quick Response code Indonesia Standard). Broadly speaking with our industry contacts, no one really expects their eWallet or payment service to be very profitable. With eWallets, they can earn interest from consumer deposits, but many consumers keep trivial amounts of money in their wallets (one contact estimated it at $20 and no one thought even at the high end consumers had more than $100-200). Payments services are also not expected to be much of a money maker with fee rates regulated, proliferate alternatives, and the strategic nature of payments making companies reticent to aggressively push monetization for fear of forfeiting activity.

Grab is utilizing the monetization strategy of Gojek and other financial apps globally: cross-selling. Ant Financial is the pinnacle embodiment of this strategy, with the average user using a myriad of different financial products. As shown below, Grab has various financial offerings within the app, including BNPL, insurance, asset management, and other banking services.

Grab competes here not only with Gojek and SeaMoney, but also Dana (a local Indonesian wallet that is part of Ant Financial), Akulaku (a digital bank across South East Asia), and a bunch of other players that focus on specific verticals like Kredivo (BNPL), Koinworks (lending), Amartha (lending), Xendit (payments), Oy! (payments), Flip (payments). The players with digital banking licensing now include Bank Jago (Gojek partner), Tonik Bank, Honest Bank, Big Pay in addition to Shopee and Grab. OVO, an Indonesian-based fintech with a leading wallet positioning was effectively (via a series of esoteric ownership structures and partnerships) 90% acquired by Grab this last month after building an original investment in them back in 2018.

Licenses vary by country though, each with a separate long and arduous process to win them. Today, Grab only has a full banking license in Singapore, which they had to team up with Singapore-based telecom provider Singtel to secure. In other countries they have limited licenses though, for example, in Indonesia they do not have a full banking license, but they have a lending license through OVO. They are in the process of securing other licenses, but all players are in a similar boat. GoJek partners with Bank Jago since they do not have a license in Indonesia. SeaMoney also has a Singapore banking license, but doesn’t have one anywhere else. Governments have been slow to award licenses and often prefer legacy banks or home grown fintechs to regional tech companies. There is no dominant player in SEA, with market positioning varying by country and could shift on a whim depending on the approval of licenses or forging of partnerships. This is all to say that for a financial service that is predicated on cross-selling for monetary success, there is still a lot of hurdles.

As far as the consumer experience is concerned, many view the apps of Grab and Gojek similarly, with over half of the consumers we spoke with having both. On margin, consumers mentioned that Grab still seems to provide more incentives than Gojek (26% for Grab vs 15% for Gojek, but with no noticeable difference the most common answer). Of the ~100 consumers we interviewed 54% had Grab and 50% had GoJek, showing that cross-use is the most common (at 61%, shown below).

Importantly, by law, eWallets cannot give users interest on their deposits so they have to compete on other factors like convenience, acceptance, breadth of offerings (i.e. the Superapp ecosystem). Ironically, the more each wallet tries to differentiate themselves, the more likely a user is to have multiple wallets, which means the “cross-sell” opportunity will be further bifurcated.

Grab also has many offerings aimed at their driver partners like car insurance that is offered in micropayments as little as ~$0.30 per ride and also offers payment solutions so a driver can receive a payment immediately after a ride/delivery ends and doesn’t need to wait for it to “clear”.

The other aspect of Grab’s financial offerings are merchant focused, specifically towards MSME (micro, small, medium enterprise). The original offering was QR-code facilitated payments. As shown below, in lieu of a “dongle”, users scan the QR code with their smartphone to pay for goods. They also recently rolled out a numberless pay card (shown above) that utilizes Mastercard’s network, employing NFC and EMV chip technology, to facilitate a transaction without having to open your phone.

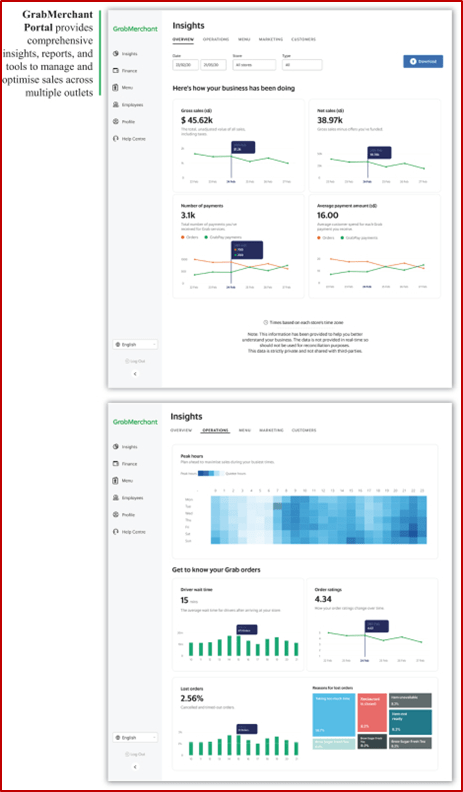

In addition to enabling merchants to take digital payments, Grab also offers working capital loans, insurance, factoring, and some analytics and software tools through their GrabMerchant Portal. While the GrabMerchant portal technically falls under their enterprise offerings, we are mentioning it here because of the natural tie-ins between payments/sales and thus business insights. Grab can use their relationship to onboard the merchant onto the GrabMerchant platform, where they can upsell them on different analytics and software tools from there. Software offerings can become more integrated into the businesses everyday operations, whereby increasing reliance makes supplanting Grab all the harder.

As payments has become a fairly commoditized service, software is increasingly how payment companies will differentiate themselves. Grab’s efforts here are still in early innings and the industry contacts we spoke with didn’t know many merchants who currently utilized their full suite of offerings, but they also acknowledge this has become an increasing focus for payment-forward companies. The opportunity is to translate all of the data they collect to actionable insights for a business. For instance, with sales info linked to an inventory management system, merchants can be alerted when a SKU is low or when a sales channel like GrabFood is slower than usual so they can offer a promo. It’s not quite this sophisticated yet, but over time they could potentially become the merchant’s “operating system”. However, this is hard to execute on and many players are going after the same opportunity. Today, the most popular route for merchants is utilizing an amalgamation of different solutions without a single unifying platform, which could change overtime.

Sizing up the ultimate earnings power of Grab’s financial operations is tricky and will no doubt be fraught with fallacious assumptions. There are many unknowns including: 1) the mature user base of Grab, 2) the rate of adoption of financial services, 3) the monetization rates of financial services, 4) the loss rates with lending given the limited credit history, 5) regulation limitations, and 6) whether they take financial services on balance sheet (in which case they will need a funding source) or if they partner with other banks. In our build we will assume that they do not want to have a bank-like balance sheet and thus will partner with banks, passing off the loans or insurance policy in return for a referral fee. For instance, Grab recently partnered with Citi Bank to offer personal loans in. A partnership like this effectively allows Grab to monetize their user base by becoming a funnel for Citi’s lending business, with the amount Citi pays in “CAC” to be Grab’s revenue. For an internet company with no experience in lending, this seems like the most likely route as they would otherwise have to raise funds and would still not be as profitable as a bank. (This is because banks profit off of the spread and effectively compete on the cost of their funds. Deposits are often the cheapest source of funds, but that is a highly regulated activity, so Grab would have a higher cost of funds and thus a smaller spread for the same loan). Below we take a stab at trying to size up how they can eventually monetize their financial offerings, but this is a very low confidence forecast (which has a much larger band of outcomes than what we are showing below).

In the build above we are trying our best to just get the broad strokes of different revenue streams for their financial offerings, but in doing so we have no doubt oversimplified and missed many levels of granularity. However, the aim is to just get a rough sense of the magnitude of Grab’s earnings power. The build shows ~$1.3bn of revenues from financial services. This assumes zero incentives, which they would net against revenues (So our current revenues of $93mn match LTM gross billings). It is hard to say whether this is bullish or conservative, as most of these offerings are very new and have very low adoption. Perhaps success could look much better than this, but if none of these businesses materialize to a large extent it also wouldn’t be that surprising, especially in the context of how competitive the financial sector is between legacy banks, fintechs, and regional tech companies.

Enterprise and New Initiatives.

As shown below Grab has started to generate some revenue from their enterprise and other initiatives. We are rather positive on their enterprise offerings and advertising, but it is too early to pencil out how it will unfold.

Clearly, business services are a large market, and could not only be a great growth opportunity for them, but also a much easier business to make money in than their other businesses. Somewhat ironically, this segment is their second most profitable segment (!). GrabAds are utilized throughout their app to monetize consumer time spent. They have several ad formats, including header ads on the home page and pop-up ads when you order a ride. The largest advertising opportunity though, is promoted listings for their delivery businesses whereby a restaurant pays Grab for priority placement in the app and search engine result page, effectively paying them for demand-generation capabilities (it seems that this is recorded in the food deliveries segment, and we will reflect that in our GrabFood valuation). Sponsored listings is an important source of revenue for marketplace businesses (think Amazon) and is likely going to be a majority of all profits Grab makes off of food delivery. This is also in stark contrast to ride-hail, which because of the commoditized nature of the service, does not accommodate “sponsored listings”. As mentioned prior, advertising also includes billboards and wraps for cars as well as in-car advertisements. Having all of these capabilities allows Grab to run full service campaigns where a company can really saturate the market with their message.

Build and Valuation.

To be honest, we almost didn’t do a build for Grab because of how little basis we felt we had for almost all of our assumptions. As as investor, you always have the option of “passing” if it’s too difficult, but as business researchers we felt we had to provide some bearings for our readers rather than just putting it in the “too difficult” bucket. In order to solve for this, we opted to use what we consider to be fairly optimistic assumptions and rely on our qualitative assessment to gauge whether this seems like a fair return for the risk perceived. However, what we consider optimistic, another investor, with further diligence, may consider to be a fair base assumption. With the return as given, it is up to the investor to judge whether it is sufficient for the risks they deem to be significant. Sometimes valuation is easiest to work backwards with, starting with what your return would be if all goes well and then deciding if you are willing to stomach those assumptions that get you there. To draw back on the metaphor we used in our SE Update, we are trying to provide a map (as low resolution as it may be) for investors to decide whether or not they want to take the trip–or perhaps whether it is even worth researching further.

GrabFood Delivery Valuation.

As shown below, if we assume a $40bn TAM by 2030 with Grab controlling half of that, then that is $20bn of GMV versus just $6.8bn today. The net-take rate is the most sensitive assumption in the model. Their gross take-rate is around 18% today, but after incentives it falls to a net take-rate of 2.6%. In Grab’s own unit economic illustration they show a ~4% net take-rate. We believe advertising services are more likely to make up for an increase in net take-rate rather then decreasing incentives. Looking at ecommerce peers, ~5% of gmv as advertising revenues seems like a fair assumption to us. This would be high margin and would materially raise the net take-rate. With around a 10% net take-rate, Grab would generate $1.2bn- 1.8bn in revenues vs $179mn LTM. It is hard to inform a steady state margin assumption as there are no mature global peers, but looking to a scaled and monoline food delivery peer, Door Dash, we see that they are today at ~25% margins if you back out the S&M. Of course, Grab will still incur some of this S&M even though they record incentives on a net basis. In theory, an internet platform should be highly scalable and enjoy high incremental margins, but we acknowledge that in practice, operating leverage has been limited in global peers. If you take on faith that they can achieve 25-30% mature margins, which seems plausible, although we can’t support that view with any existing mature businesses, then you get $6-11bn in value at a 25x multiple (which would need mid to high single digit growth exiting 2030 to support). We purposely broadened the range of values in the sensitivity because of the higher range of unknown variables to allow an investor to make their own judgement. At the high end of values we get $22bn, but we could still be too conservative for some (in which case you should download the excel and change whatever assumptions you want into it!). It is also worth noting we are only looking at food delivery here and not their local commerce deliveries business, which will have its own TAM. We have no sense of how large their non-food delivery business is and none of our contacts have used it either, but it is no doubt another growth vector (more on this in the call options section).

Grab Mobility Valuation.

We ran a similar valuation on Grab’s Mobility business, sizing up Grab’s TAM numbers to $28bn for 2030. We assume Grab is the dominant leader in the region with 65% market share for a GMV of $18bn vs $3.1bn LTM today ($5.7bn 2019). This implies Grab will grow mobility GMV at a low double digit rate for a decade. Net take-rates today are 17%, but their unit economic sketch shows 6%, so we would think that incentives are likely to be higher overtime. Putting a mature margin band assumption on their mobility business was very tricky as there is no profitable player globally and accounting methods differ. Didi for example, the clear dominant leader in China with ~90% market share only reported a paltry adjusted EBITDA figure that comes out to around a ~10% margin if you account for their payments on a net basis. However, on a GAAP basis this is still negative, despite Didi achieving the greatest scale of any ride-hail player. Frankly, this draws into question whether ride-hail will ever be profitable. Grab’s strategy of tying it to other services makes especially good sense if this turns out to be the case. At the high end we show a 25% margin which you will have to take on faith they can achieve that and on the low end we show a 5% mature profit margin, which still seems herculean. Assuming incentives kick back up for a 10-14% net take-rate, we get a $3-6bn segment value, which gets as high as $16bn in the most optimistic scenario.

Grab Financial Services Valuation.

We already touched on how we got to our revenue figure prior, but please remember that there is little scientific about it. We show a wide range as low as $500mn-$3bn in revenues and apply 20-50% mature margins. Our margins are informed by looking at peer financial services companies, which show a wide range of profitability. In theory, as a large portion of their revenues will be “referrals”, they should enjoy high margins here. We capitalize our NOPAT estimates at 30x, which is a fair multiple if they are able to achieve these margins and still be growing double digits in 2030 (not implausible as SEA is very underbanked).

Combined Valuation.

Rolling up everything we are circling around a $20-$40bn valuation for their existing segments. If you are very optimistic about these markets perhaps you are honing in closer to our $80bn figure, but with the current SPAC valuation of ~$40bn that is only a 7% per annum return in a very optimistic scenario, which may not seem like a fair return for the risk. However, there are also several call options for Grab that we are not explicitly valuing.

To be fair, explicitly valuing the businesses that exists forces us to assume the value of the Superapp is only their “foundation” plus some financial cross-sell opportunities, but of course if they can really achieve their Superapp goal than the businesses that have yet to be introduced will possibly be worth more than all of those that currently exist. Remember that with a real Superapp (and flywheel) the sum of the parts are worth more than the components. This is all to say that, in our opinion, an investor would have to unwaveringly believe Grab will become the undisputed Superapp of SEA for this to be an attractive investment. We do not believe our diligence has supported such a conclusion, but “growth” investing often requires heavily relying on one’s judgment of management and their capabilities, which we do rate highly.

Call Options.

- GrabMart. This is a business that is already operating, but it is unclear how big it is today. If local commerce becomes very popular and Grab is able to leverage their merchant relationships, perhaps they can gain significant share here as more people opt for quick commerce rather than the longer Shopee experience. We remain skeptical on how large of a use case this will ultimately become as there doesn’t seem to be many different things you need on demand, but if they have wide enough selection and good enough prices then there is no reason why they can’t achieve some success here.

- Advertising. While we are considering promoted listings in the Food deliveries app, they still have more advertising opportunities throughout their Superapp. Adding new services and selection to their app could also make certain advertising more valuable as it increases conversion rates. Imagine seeing an ad for a consumer loan and being able to click into it with Grab preloading all of your relevant information to complete the application process easier. Or perhaps a local merchant runs a campaign for flowers, and you can click the ad to get them instantly delivered. It is hard to size this up exactly, but this is a big opportunity as there are few platforms that can advertise as well as facilitate the service (or transaction) they are advertising for. However, slightly offsetting our constructive view here is that CPMs are very cheap in South East Asia, but with last click attribution (proving your ad delivered a sale), they should be able to demand higher CPMs (click through rates higher).

- Enterprise. While we touched on their merchant and enterprise offerings, this is a large opportunity for them with many different software verticals they can capitalize on. Any success here would be very welcomed as a higher margin business with a large TAM could help bring their profit profile up meaningfully.

- Grocery. As part of their push into grocery delivery, Grab has started testing a delivery-only supermarket dubbed GrabSupermarket that promises 24 hour delivery and zero delivery fees. Given the high-frequency, large AOV nature of this activity, winning it will be important for Grab to not only build a sturdier Superapp foundation, but also provide further opportunity to generate profits for their food delivery business. While it’s still in its early days, we recommend reading our Alibaba and Coupang pieces to get a better sense of what it can become.

- New Businesses. Grab will continue to roll out new services, naturally extending the advantage of the Superapp. If you believe Grab has a dominant Superapp then there is a long greenfield of different services, they could roll out to monetize their user base. This could be the largest value of Grab’s business today, but it is impossible to quantify.

Risks.

- Negative Operating Cash Flow. There is no way to politely say this, but consistently negative operating cash flows that are funded by positive financing cash flows is traditionally considered a bankruptcy risk. While we do not believe that is a base case by any means, Grab operates in some extremely tough businesses and has not shown an ability to generate profit in their core operations. Worst case scenario they could, of course, cut incentives and growth investments which would likely allow them to be profitable, but that would hurt platform activity and destroy the investment thesis. We are only saying this as a consideration and potential risk, not to make any claims that it is imminent or even likely.

- Autonomous Vehicles. There is a long section on the AV risks to ride-hail in our Didi piece, but in short, autonomous vehicles change the value chain and different parties’ respective negotiating leverage in ways that are very unclear. While the value of a dense network will remain, where the control of that network lies could change. We recommend our Didi AV section for a more in-depth discussion on this, but we will note that the high use of motorcycles and other small, unique vehicles reduces the risk that they will be supplanted by AV. Additionally, as the cost of autonomous vehicles will initially be high, the South East Asian region is unlikely to among those that sees early high penetration. However, if you are organizing around far out future number then this is definitely a factor to consider.

- Competition destroys mature margin structure. While until last year competition looked to be slowing down, SE has significantly altered the competitive landscape and could either steal market share or cause incentives to go higher, reducing profitability. Even in ride-hail new competitors are still popping up, like a Russian company called Maxim that is gaining some share but undercutting Grab and Gojek. While of course Grab and Gojek could respond in such a manner that likely drives these upstarts to bankruptcy, the issue is that they have to continually “flex” this muscle every time they are nearing profitability, so perhaps these “mature margin” structures are an illusion…

- Mature margin structures are an illusion. Following that point, we do not have a strong basis to figure out what many different cost items will be in the future as there are no steady-state P&Ls to help us. The supposed operating leverage we should see in these models has never come through in a meaningful way. That is not just a criticism of Grab, but is true of Uber, Lyft, Didi and others. While we can in theory see these businesses turning a profit, the dollars you invest in these companies are not theoretical.

- TAM is smaller than assumed. With many early, growing markets, it is never clear when they will suddenly slow. The addressable markets for ride-hail and food delivery specifically could be smaller than we assumed in our builds. The financial services sector TAM is not likely underestimated and we do think it will grow for a long time as SEA is very underpenetrated with banking services, but competition picking up could mean Grab’s share of this market is smaller than we assume.

- SPAC related dilution. We focused on the business analysis and not the deal specifics, but a lot of recent SPACs have had provisions that would allow for the promoter to receive more shares if certain conditions are met (through warrants usually). SPACs have the reputation of being fairly shareholder unfriendly, with layers of fees and dilution behind opaque legalese.

Summary Model.

Below we have our summary model, which can help give an investor some sense of how much operating leverage you would need to come through to reach profitability. We are growing total revenues at a ~30% CAGR, but expenses at only a ~7% CAGR to show a small profit by 2025. We consider the revenue growth assumptions to be actually fair (other than the enterprise line which is pretty optimistic), but the cost assumptions are very generous, especially when considering no global peer has experienced any cost leverage nearly as strong.