*Please see our disclaimers at the bottom of the page and our full disclaimer here. By using our website, you acknowledge you have read our disclaimers and agree to our terms of use.

Thank you so much to all of our subscribers. This is our first piece that is behind the paywall and given how gargantuan of a company Alibaba is, it is rather long! We know you will find high value in reading it though and additionally we will release a “PM Summary” this weekend that will be included for free in your subscription.

Given the prominence of Jack Ma and Alibaba, we have spent more time than usual on the businesses history, with sections on “Founding History” and “Business Background”. Feel free to skip right to “The Business” if you’re familiar with their story!

Founding History.

Alibaba founder Jack Ma was born in Hangzhou, China in 1964, a time when private enterprises were forbidden from operating. However, by his early teens, there were signs of China moving toward a new direction. In 1978, Deng Xiaoping launched China’s Open Door Policy, which when coupled with President Nixon’s visit to Ma’s hometown a few years prior, led to a tourism flourishing. Jack took this opportunity to practice his English by offering tours of the city. Despite his developed English skills, Jack was a poor math student and failed the GaoKao (China’s college entrance exam) twice. As a result, he became an English teacher and started his first company: The Hangzhou Haibo Translation Agency. Given his fluency in English, the municipal government sent him to the US to investigate the status of a construction project (which turned out to be fraudulent), where he was reportedly kidnapped (although Jack is sparse on details with regards to this supposed incident). It was in the US that Jack first learned of the Internet. He returned to China with one of the first computers in the entire region.

Surprised by China’s non-existent Internet footprint, Jack started a Yellow Pages for China, dupped chinapages.com, to help people find Chinese businesses globally. Unfortunately for Jack, the Internet was too nascent in 1995, and Ma had trouble explaining what it was and why it was important — people thought he was a con man. After a rough period of trying to win clients, they negotiated an agreement with a state-owned enterprise (SOE) where the SOE took a majority ownership in the company in exchange for a much-needed cash infusion. While they were supposed to work on a project together, the SOE was quick to ignore all of Jack’s input, and essentially turned him into a glorified public servant in a stultified government organization. After a few years there, Jack began plotting his next venture with 17 colleagues who would later become his cofounders in a business that would focus on the “shrimp” of B2B (a reference to American B2B sites being whales but 85% of the fish in the sea being shrimp-sized). In his cramped Lakeside Garden apartment in Hangzhou, Alibaba was born.

Open Sesame.

Background.

Alibaba was launched in 1999 to help facilitate B2B transactions. Initially, it was a collection of bulletin boards and message boards that helped various businesses source products (the transaction would be completed offline). A few months after launching, Joe Tsai, a Taiwanese-born, Yale Law School graduate became so captivated by Jack Ma that he left his lucrative private equity job to help Alibaba raise money. At the time, while they already had decent traction with over 28,000 members, Tsai was instrumental in helping legitimize the business (when he joined it hadn’t even been incorporated) and shoring up investors. Through Tsai’s network, Alibaba was able to secure a $5mn investment from Goldman Sachs for half of the company (Goldman would later completely exit their investment in 2004 for $22mn). This was critical to getting Softbank billionaire Masayoshi Son’s attention, who decided on the spot of meeting Jack to invest $20mn for 30% of Alibaba, which had grown its member base to over 100,000. Masa’s investment was crucial in keeping Alibaba afloat post-dot com bubble burst and as US internet companies Yahoo and eBay entered China, as Alibaba still hadn’t generated any revenue (nor had they figured out how they even would).

eBay entered the China market via the acquisition of auction house EachNet, which proved to be a pivotal event for Alibaba. While eBay focused more on C2C and B2C, Alibaba was concerned that large sellers on EachNet would eventually find their way into the B2B space. To obviate that fate, Alibaba moved downstream and launched Taobao in 2003 to focus on smaller sellers and consumers. Taobao sellers enjoyed free listings and zero commissions, a huge contrast with “Greedbay’s” ever increasing fees. Shortly after launching Taobao, Alibaba launched Alipay, a simple escrow service to help facilitate payments on Taobao. eBay’s bureaucratic management paralyzed platform development, and when they moved platform hosting from China to San Jose, web page loading became prohibitively slow and users churned in mass. This effectively ended eBay’s commerce ambitions in China. This was a huge feat for Alibaba as eBay was one of the world’s premier technology companies at the time. Yahoo had similar troubles fending off local competitors in China, and in 2005 decided to make a strategic investment of $1bn for 40% of Alibaba after which Alibaba would run Yahoo China (which was in a downward spiral after achieving muted success). This investment helped Alibaba continue to focus on building platform activity rather than monetization, but also likely played a role in Ant Financial ultimately being transferred from Alibaba (more on this to come).

By 2007, Alibaba.com had turned profitable thanks to the membership fees they had started charging for sellers to join the platform. But since Taobao was still burning cash, Alibaba decided to list just Alibaba.com in a 2007 Hong Kong IPO, which raised ~$1.7bn. The fortuitous timing of these funds helped insulate them from the worst of the Global Financial Crisis and allowed them to continue to build their platform. Notably, as global trade was hit hard, Jack decided that there was more opportunity focusing within China, and launched Tmall, an ecommerce platform that helps branded businesses sell to Chinese consumers. A year later, in 2009, Alibaba launched Aliyun (Alibaba Cloud).

In 2010, the People’s Bank of China (PBOC) issued vague rules on domestic third-party payment platforms that required all payment companies have one of the limited licenses or risk having to immediately cease operations. It was not clear whether majority-foreign-owned entities could control payment platforms or not, but Jack maintains that in order to avoid the risk of having to shut down Alipay, he transferred asset to himself and another cofounder for ~$51mn. At the time, Yahoo and Jack were publicly clashing due to Yahoo China’s continued languishing under Alibaba’s stewardship (likely an inevitability anyway), but Jack was concerned that Yahoo would leverage their large stake to replace him. We don’t think it will ever be clear if Jack was acting out of an abundance of caution, if moving Alipay under his control was an insurance policy to threaten Yahoo, or if something else was happening in the shadows. It could, of course, also just be that Jack was vying for a higher economic interest—but given his character and history of readily sharing equity (18 cofounders!), this seems the most unlikely. However, Alipay did receive license #1 and eventually Alibaba received a 1/3rd interest in Ant Financial, the new company that housed Alipay. Nevertheless, this instance highlights the major risks of the VIE structure with loose governance.

In 2013, Alibaba partnered with four of the largest logistics providers in China to create Cainiao and further reduce ecommerce friction. Since over half of all shipped packages were originating from Alibaba sites, it made sense to add a software layer that would integrate all of the different logistics providers and streamline operations for everyone since it eliminated the need for each logistics company to individually build out their own technology. This would also help them compete against JD.com, who operates their own logistics network that is highly regarded by consumers and often cited as a competitive advantage. As Alibaba’s business ambitions grew, they IPOed in 2014 on the New York Stock Exchange (NYSE) to bolster their investment capabilities and allow early shareholders to cash out. In the years that followed, they launched several businesses (Freshippo, Tmall Genie, Taobao Deals) and acquired or invested in many others including (but not limited to): ChinaVision Media (renamed to Alibaba Pictures), Youku, (top 3 long form video hosting site in China), Ele.me (local food delivery), and Lazada (see our Sea Limited piece for more info).

Jack Ma stepped down as CEO in 2013 and as Chairman in 2019 to focus on philanthropy. Daniel Zhang, a former President of Taobao & Tmall, has been Alibaba’s CEO since 2015. Joseph Tsai is still involved as Executive Vice Chairman.

The Business.

Alibaba operates many disparate businesses, but reports them through four segments: 1) Core Commerce, 2) Cloud Computing, 3) Digital Media & Entertainment, and 4) Innovation Initiatives & Others. We will start with Core Commerce, which is ~86% of revenues and the most important piece of their business.

Core Commerce.

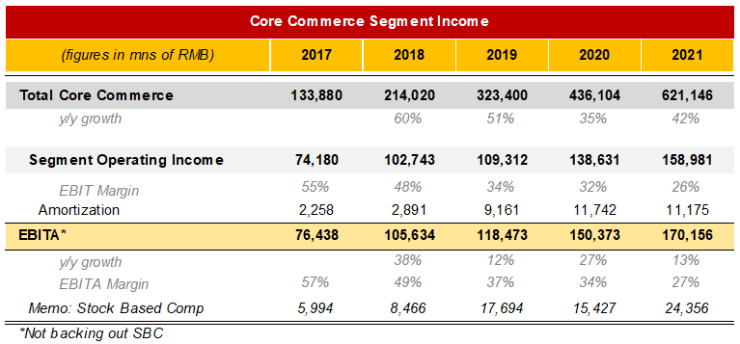

Core Commerce is further broken up into seven different segments, split between business in China vs. international, retails vs. wholesale, and other commerce services which includes logistics and local (which is mostly on demand food and CPG delivery, similar to DoorDash). Alibaba generated over RMB 600bn, or almost $100bn, from their core commerce businesses in 2021, growing revenues an incredible ~3.5x since just 2017. (Note that their fiscal year ends March 31st.)

As seen below, China Commerce Retail is >75% of their commerce revenues. So we will mainly focus on this piece of the business, which includes the immensely popular Taobao and Tmall platforms.

Core Commerce: China Retail.

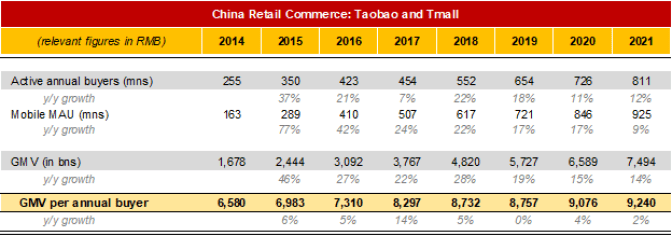

Taobao and Tmall are two of the largest ecommerce platforms globally, and together they facilitated RMB ~7.5tn of GMV last year (or ~$1.1tn) with that split roughly 50/50 between each platform. For a sense of scale, Amazon is estimated to support ~$500bn of GMV, or less than half of what Alibaba did last year. Just to hammer this point home, while GDP and GMV are not perfect comparisons, there are only 17 countries whose GDP is over $1tn. Alibaba also has a large buyer base with 800mn+ annual customers just in China and MAUs of 900mn+. As shown below, buyers have not only grown every year, but as a group have stepped up their purchasing on Alibaba’s platforms and now spend just shy of RMB ~10,000 per buyer. This is important to keep in mind when we talk about competition later on.

First, we dive deep into the dynamics of the platforms and why customers and merchants incessantly use their platforms.

Taobao and Tmall.

As mentioned previously, Taobao was started as a sort of eBay competitor, but quickly took on a life of its own and is now markedly different from anything you will see elsewhere. This is partly because of the underdeveloped retail environment in early 2000s China, which accelerated the usage of ecommerce penetration. Readers may recall a similar dynamic in our Sea Limited piece, whereby the relative infancy of physical retail was met with a jump straight to ecommerce, especially mobile-native ecommerce.

While eBay was focusing on selling used goods, Taobao knew that that approach wouldn’t work well in China where the average person had fewer possessions and most things they did own was not of high enough quality to be of value to a 2nd owner. Thus, Taobao focused on becoming a platform for small merchants and sellers, and today hosts over 10mn of them. While Taobao does have a reputation for being lower quality, its usage is high even among higher-income consumers in Tier 1 cities because of their wide selection and great value with incredibly cheap products.

Swipe through to get a feel for the main tabs on the Taobao app.

Taobao does not charge a listing or selling fee, which sets it apart from virtually every other ecommerce platform. Instead, they monetize through sponsored listings and other seller services. The no fee structure helped seed the marketplace with more sellers early on and today it has more selection than any other ecommerce platform at 1bn+ products. Compare that to Amazon, which has an estimated ~350mn products. To fill the gap of higher end products though, Alibaba has Tmall.

Swipe to get an idea of what it’s like to interact with the Tmall app.

With Tmall, Alibaba was looking to move upmarket with higher quality and branded goods—an area JD.com was already focused on. More Chinese consumers were becoming familiar with global brands, but there were limited ways to buy them and most global retailers weren’t sure how to approach the China market. Tmall aimed to solve both of these issues by making it easy for a multi-national company to set up a Tmall storefront and leverage Alibaba’s payment and logistics infrastructure for Tmall customers. Over time, many Chinese brands also started selling on Tmall, and today it is regarded as higher end than Taobao and almost as good as, if not on par with, JD.com, which is considered the gold standard for authentic products given its heritage as 100% 1P. However, JD.com is often more expensive and has a much more limited selection than Tmall. Most of the consumers we spoke to have used Tmall before for higher priced items, but for particularly large ticket items (especially high-end electronics) they prefer JD.com. Of course, this also varies by income levels. In the competition section below, we will get more into when and why a user prefers one platform over another. Tmall’s importance to Alibaba has been gaining in recent years with GMB growing from RMB 500bn in 2014 to RMB 3.2tn last year, almost on par with Taobao.

Unlike Taobao, Tmall charges a seller fee that ranges from 0.3-5% and comprises a sizeable portion of revenue. They stopped disclosing revenue from commissions last year, but it was about 40% of what they generated from advertising (in total it was ~21% of China Retail revenues, but that is understating its contribution because of 1P sales from their New Retail initiatives). Tmall has a standalone app, but a lot of traffic is also directed from Taobao. When searching for items in Taobao, buyers also see listings from Tmall (but not the other way around). This helps Alibaba upsell to their large and high engaged Taobao user base. For instance, a user could search for cooking ware in the Taobao app and see listings for cooking ware from branded Tmall stores in the results.

There have been many developments in ecommerce shopping since they launched these platforms, most notably: 1) livestreaming, 2) short-form videos, 3) group buying, 4) gamification, and 5) AR-enabled experiences.

1) Livestreaming: Taobao Livestreaming is very popular has generated over RMB 500bn in GMV in 2021. Livestreaming can often be similar to a home network shopping channel, but is tailored to each user’s interests with a wide variety of different streamers. Key Opinion Influencers (KOLs) will often livestream themselves showcasing products they like in exchange for a commission on sales (similar to how Instagram influencers will post products they like for a fee). For instance, a KOL may give a tutorial on how to apply a beauty product or show how to make a delicious stew with a pressure cooker, all the while promoting the items featured at a discounted price for viewers. Alibaba also has an affiliates program where they help merchants find KOLs to showcase their products whereby the merchant gets to set the commission fee (with Alibaba taking a small portion). The other aspect of livestreaming is more “personal” shopping experiences, like a farmer showing off fresh crops or a craftsman showing off new art pieces. For example, Huang Wensheng, better known as “Uncle Farmer”, is a popular tea farmer in rural China whose livestreams regularly receive millions of views. He dishes out tea expertise and life advice while exhibiting the minutia of farming life (rural farming livestreaming has become very popular recently). This format crosses commerce and entertainment, helping make Taobao a high(er)-engagement app.

2) Short-form Videos: Similar to livestreaming, this is another format for KOLs and brands to showcase their products. It differs in that it is much “punchier” content that tends to be more producted, although in some cases it is edited down livestreaming clips. Essentially, it is a more commerce-focused version of Douyin, built right into the Taobao app. The videos are used to help consumers find products and also see them demonstrated. Video has been a big push for Alibaba and they even required sellers to upload a minimum amount of short-form content to be promoted during the big Single’s Day event.

3) Group Buying: This has been getting a lot of attention recently due to the seemingly instantaneous ascendance of Pinduoduo (PDD). While there are a few different ways to implement this practice, the general idea is that the platform helps aggregate purchase orders and sends them directly to the manufacturer, allowing them to circumvent a distributor who traditionally played this role. The value prop to the manufacturer is clarity in demand forecasting coupled with scale, allowing them to offer customers the very cheap prices that a distributor would usually buy at. The consumer gets cheaper goods, but they often arrive slower as they are not on demand. PDD also has group leaders that can start a group purchase order and enlist friends often via WeChat. The group leader (depending on the model) can receive a commission from the order and is also responsible for collecting and distributing the items, which is a very elegant solution to the last-mile delivery problem. However, as PDD has gained scale, the groups of buyers have dropped from 10+ buyers to often just two (and regular home delivery is often used). Once there is a scaled user base, like PDD’s 824mn buyers, the need for groups drops on popular products because the demand is always coming in. However, the social functionality that comes with group buying continues to make it more interactive than traditional ecommerce, especially when you add on a layer of gamification. Clearly, PDD found a niche here, but Taobao is ready to compete in this space as well, launching Taobao Deals a little over a year ago. This standalone app has already garnered 150mn+ buyers and they are aggressively expanding their product offerings while leveraging their massive merchant and consumer bases to grow. Last year, 70% of new buyers were from lower tier cities. It’s also worth mentioning that Alibaba has had another business in the “Money for Value” space for a long time, called Juhuasuan. Juhuasuan is housed in the Taobao app for flash sales, and has recently been revamped. The shift of focus to the Money for Value space comes amid maturing ecommerce for middle and higher income consumers vs. lower tier cities still having low ecommerce penetration. More to come in the competition section below, but this is a growing area and focus for Alibaba as they’ve committed to reinvesting to fend off competition.

4) Gamification: Similar to group buying, this has also been a buzzword as of late. While PDD may have popularized this by executing particularly well with their gamification features, some aspect of this was present in Chinese commerce for a while (Ant Forest was a game launched in 2016 by Ant Financial where users would receive “green energy” whenever they used public transit or bought e-tickets that was used to grow a virtual tree. Real trees would then be platnted once the virtual tree matured… sound familiar to a certain recently popularized ecommerce game?). The idea of gamification is simple: make the app look more like a game and reward the consumer behaviors that you want to incentivize within the game. In one of the original PDD games, users receive “water droplets” and “fertilizer” by sharing with friends, buying goods, visiting merchant pages, and checking in daily, which they can use to grow a fruit tree of their choice, receive a shipment of actual fruit at maturation. Features like this help increase user engagement, stickiness, and virality. As such, Taobao has been focused on further gamifying their app, with little hesitation to emulate the more popular features of competitor products (see below).

5) AR-Enabled Experiences: While still in its early days, Alibaba has already demonstrated several new shopping experiences that are powered by AR in their apps. For example, virtual showrooms that are interactive or trying on clothing & makeup virtually. These efforts are still early innings and, as the AR space develops, there are going to be many other novel experiences that can be offered. All of these features are technically difficult to implement, and can potentially raise the barriers to compete in ecommerce over time.

All these features together have helped Taobao remain relevant while also giving competitors an opportunity to gain share. Ecommerce is ~25% penetrated, but will continue to grow as China incomes rise and physical retail becomes more meshed with online (a lot of Alibaba online/offline initiatives here; we will go into these in the New Retail segment below). As shown below, despite competitive intensity increasing, Alibaba has grown China retail revenues and active annual buyers every year. Additionally, total spend per user (GMV per buyer) across Alibaba platforms has increased every year. While we don’t have granular cohort data, we know that Alibaba is higher penetrated among higher income users and spend per user increases every year. Thus, we can ascertain that aged cohorts increase spend per user more than the average spend per buyer increases. This implies the spend per buyer figures we calculate in the exhibit below are dragged down by new buyers and the buyer base simply “aging” will result in GMV per buyer growth. Said simply, we show GMV per buyer growing ~6% since 2014, but the (hard to read) Investor Day slide below implies the 2016 cohort was growing spend ~40%+. New buyers are likely lower income so will not likely spend at those rates ever, but this is good GMV growth driver to be aware of and points to the large value consumers see in Alibaba.

The table below shows core China Commerce metrics for Taobao and Tmall. GMV per buyer grows from RMB ~6,500 in 2014 to RMB ~10,000 last year.

However, while spend per user is still growing, increasing the monetization rate (net revenue as a % of GMV) has been the more powerful lever in topline growth as of late. In the chart below we show what portion of total revenue growth can be ascribed to GMV growth vs. increasing their monetization rate of that GMV. While GMV growth used to drive ~40%+ of revenue growth, it has been a smaller revenue driver (ex-Covid bump). IN other words, their ability to further monetize their existing GMV is more important to incremental revenue growth than growing GMV further (but of course, they can do both).

To answer the question of how they can increase their monetization rate, we turn to the lesser known, but quiet driver of almost all of Alibaba’s revenues: Alimama.

China Retail Monetization: Alimama.

Alimama is a marketing ad platform, and the principal way Alibaba monetizes their Taobao and Tmall services. Alibaba breaks down their China Commerce Retail revenues into 1) Customer Management, 2) Commissions, and 3) Other. Commissions are mostly from the Tmall marketplace, and the “Other” category is also known as New Retail, which we will touch on later. Customer Management revenues consist of several products for merchants to bid on keywords for search rankings, buy display ads, and buy sponsored placements on a CPC basis. There are also programs like Taobao Ke, an affiliated marketing program whereby Alibaba helps match merchants to individuals to promote their products. These individuals are KOLs and receive a fixed commission (set by the merchant) for making sales through their channels, which can include external platforms—this is how many livestreamers can monetize their channels.

While it is not important to grasp the nuances of all of these products, we wanted to explore the main monetization tools of Alibaba, which sheds light on why they can be considered to be closer to a Google or Facebook, rather than an Amazon. In fact, Alibaba describes themselves as a “media” company rather than a commerce company, and this is because at the end of the day, they are largely in the business of monetizing time spend on their platforms. Compare that to Amazon, who despite their budding advertising business, is designed to get you off their platform as quick as possible by reducing all friction in the buying process. This was evident as early as 1999 when they patented the “1 click” buy it now button. While Alibaba of course does not want to create unnecessary friction in the purchase process, the platform is geared more towards engagement with a target recommendation feed, livestreamers showcasing their favorite products, short product videos, and gamification. Even the name seems to suggest the service is mean to invite engagement: Taobao translated to English is “searching for treasure” (although treasure may be too generous of a description of the products you’ll find on there). Without this context, it would seem weird that Alibaba reports MAUs and DAUs, metrics usually only seen from social media companies. Understanding this is important because the competitor set and product expectations change when a company is also in the “time spent” business.

Alibaba also enjoys a huge data advantage compared to peers. They not only benefit from owning customer purchase data, which is very high value as it actually shows what a consumer spends money on, from Taobao and Tmall, but they also have consumer data from Ant Financial/Alipay, their other ecommerce platforms, and media properties like YouKu. They even have their own unique user identity product—Uni ID— that ties all this data together and allows Alibaba to effectively track users across disparate platforms. This data allows them to better serve ads and promotions to relevant consumers and is why they also have an advantage in their 3rd party ad network business.

While seldom mentioned by management, Alibaba has an ad exchange (Taobao Ad Network and Exchange or TANX) that serves ads off platform. This is similar to Google’s DoubleClick business and is likely low margin, but it does give them an interesting competitive advantage. A Tmall merchant, for example, can buy ads through Alimama that are displayed on Weibo and then send the user back to Tmall if they click on it. Alimama not only gets paid for serving the ad, but also the benefits from the user traffic as well as 3rd party data. Similar to Google and Facebook, the algorithms that suggest ads will continue to get better over time, which 1) leads to more sales and 2) opens up more inventory as an ad can be shown fewer times to be effective. However, following this line of thinking of Alibaba as a “media matrix” (their words) monetizing time spent with ROI-driven sellers will quickly make an investor see some potential competitive threats they might not have otherwise. What we layout below is somewhat speculative, but worth being aware of as a potential investment risk.

Alibaba, Just a Media Company?

Alimama essentially monetizes time spent by selling ads and thus it makes sense to look at the health of their advertising ecosystem. A lot of their advertising can generally by considered more “discovery”-based commerce as a lot of it is geared towards showing a consumer something they didn’t know they wanted. However, the bidding on keywords is clearly more intent-based. This following line of reasoning is more applicable to the “discovery” portion of commerce, but still affects intent-based commerce as it relates to merchant return on ad spend (ROAS). We don’t know how much of Alibaba’s GMB is intent-based vs. recommendation-generated, but it could be fairly material as in our conversations with dozens of consumers, many noted that they had purchased Taobao recommended products and management has previously touted Feed Recommendation improvements as driving incremental purchases.

Above you can see theme-based recommendations and “curated” recommendations on the Taobao platform – both are powered by Alimama and the data collected from the wider Alibaba ecosystem. .

For a long time, Taobao was one of the few places to get high quality recommendations as direct response advertising is very nascent in China with few scaled platforms. Merchants thus have very limited options to drive traffic beyond Alibaba’s “Media Matrix.” While there are other ad platforms, very few had the advertiser tools, user data, and sufficiently advanced targeting algorithms that could offer merchants a good ad product that drives traffic. This is why Weibo and even Bytedance’s Toutiao and Douyin have ads served on their platforms from Alimama. However, this is quickly changing. Douyin, Kuaishou, Bilibili, and others are all building out their own advertising capabilities, which has created new channels for retailers to advertise through. These channels are already formidable in ecommerce today, with Douyin and Kuaishou driving over RMB 500bn and RMB 300bn of GMV last year, respectively. While a sizeable portion of that activity gets redirected back to Taobao or Tmall, more of it is likely to be completed on-platform, starving Alibaba from the traffic.

The real issue, though, comes when we look at the ROAS of Taobao vs. Douyin. As expected, ROAS range is wide, but a high number of Taobao merchants and a former senior Alimama executive purport(ed) ROAS (or ROI) of ~1.2x vs. Douyin advertisers of >10x. Several merchants we spoke with didn’t even know their ROAS and instead felt that they had to run the promotions just to drive traffic (without any idea if it was profitable or not).

Frankly, it is not clear how a 1.2x ROAS makes any financial sense with the low gross margins of most merchants, but one contact suggested that is because most Taobao ad buyers are factory bosses who are more focused on consistent factory throughput than profits. It is also possible that these factory bosses only buy traffic when they have an unsold portion of a batch order, or merchants are hoping to make money on a 2nd sale after establishing a customer relationship. Either way, these are clearly unsettling comments that suggest usage is supported by uneconomic ad spend. If Alibaba is just a “media’ company monetizing time spent, then ROAS is king.

The exhibit below walks through the math of why a 1.2x ROAS doesn’t make sense. Informing the merchant assumptions below is an example merchant P&L from Alibaba’s 2020 investor day. We show that the minimum break-even is for most merchants with a ~25% gross margin and what gross margin a merchant would require to break-even on a 1.2x ROAS. The math suggests that it is possible that a lot of merchants are losing money on advertising.

If a merchant is really getting a 1.2x ROAS, then they are very likely losing money.

While we think this is an important point to surface and a real risk, given the opaqueness of seller ROAS and the wide breadth of answers we received, we are not going to swallow whole the suggestion that Taobao is built on unsavvy merchants’ consistent uneconomic ad spend, suggesting Taobao is over-monetizing and at risk of other ad platforms cannibalizing their ad budgets. In response, we would like to make several points:

1) ROAS can vary for many reasons. Perhaps stating the obvious, but ROAS is not a uniform metric and varies by advertiser, product, brand, audience, ad spend, ad price, and content, which make it hard to extrapolate out generalized statements (especially with only a few dozen data points). While a low ROAS was more common than we would have like to have seen, it is also true that most ad buying still goes through agencies and operating companies who are more closed-mouth about client ROAS and more probably to be higher. Nevertheless, there still were several merchants who disclosed as high as 8x ROIs. There are ~4mn advertising merchants on Taobao and while it is likely that a good portion of them do not have consistent, profitable ad campaigns, they will fall out of bidding and new merchants will take their place in the auction.

2) Ad spend is less fungible than one may think. Many products sold on Taobao are fairly substitutable and it is hard to generate high ROAS anywhere when your product is similar to the rest. In other words, there is a selection bias between those merchants that can advertise on Douyin and those that only advertise on Taobao. Douyin advertisers are more likely to put more effort and time into content, which if successful, garners a high ROAS. But the small hair scrunchie or dining placemat merchant is probably not going to be able to create compelling content.

3) There will be many winners as the digital ad ecosystem evolves. When looking at potential advertising TAMs for companies like Facebook and Google a decade ago, analysts made the mistake of thinking these companies would simply just take market share from existing advertising players. Instead, what happened was that Facebook and Google created new use cases and grew the advertising market substantially. Similarly, it is likely that Douyin and other new platforms create new commerce opportunities and do not just cannibalize pre-existing TAMs.

4) Data advantage. As mentioned, Alibaba has a trove of data on users—not just on Taobao and Tmall but also all of their Alipay history, behavior across all Alibaba media properties, and data from their 3rd party ad network. More than just what you like, they know what you actually buy. This puts them in a great position to continue to refine their algorithms to increase ad success rates. A more refined algorithm means higher ROAS which then gets bid down again. This process could go on for a long time. Furthermore, even if Douyin, Kuaishou, and Bilibili build out their self-serve platforms, Alibaba may be able to better monetize those impressions given their better consumer data. One industry insider claimed Alibaba was still better at monetizing Douyin inventory than Bytedance is.

5) Taobao keeps improving and they are best in class for their ad product types. Remember, advertisers today use Alimama for impressions on 3rd party properties like Toutiao and that is because Alimama can monetize the inventory better than competitors. A different industry contact noted that recent improvements in Alimama’s news feed ad product has resulted in ROAS on Toutiao of 2.5-3x what other demand-side platforms (DSPs) are able to achieve (which in itself is still a lower monetization rate than Taobao Feed).

6) Global peers suggest Taobao is under-monetizing. Amazon is estimated to have advertising revenues of ~5% of GMV, with 1P estimated to be anywhere from 45-60% of that. For conservatism, assume 3P is 55%. That implies that their ad revenues are 9% of GMV in addition (!) to seller fees. Other platforms like Mercado Libre and Coupang are also estimated to be able to generate at least 3-5% of their GMV in advertising revenues (again, in addition to seller fees). In total, across both platforms, Alibaba monetizes GMV <4%. You can construe this as evidence of Alibaba’s ecommerce environment as being more competitive, which is partly true, but we believe that it is more indicative of their monstrous growth and their being in early innings of monetizing their platforms. We will revisit this point later, but we think this supports the thesis that they are more likely under-monetizing than over-monetizing.

7) ROAS is being driven down by high demand. Given their ability to drive traffic directly to merchant stores better than peers, the (potentially) low ROAS is being driven by high demand on the merchant side. Every time Alimama roles out ad improvements that increase clickthrough rates (and reduce cost per click), the ads get bid up again. This strongly suggests that the market (for whatever reason) is at an equilibrium and pricing is sustainable at this rate.

8) You are not paying for an explosive ad monetization story. To rationalize Alibaba’s valuation (explored later), it is unnecessary to pencil out a long runway of high growth in ad monetization. Simply gaining confidence that the current monetization rate is sustainable could suffice. While it would have been more comforting to see higher ROAS for merchants, we have to remember how cutthroat China ecommerce is. Even on Alibaba’s investor day, they showed only a 4% profit margin for a representative merchant (after ad spend).

9) ROAS are not capturing the true value of advertising. In talks with multiple merchants, they suggested that they are not buying ads or promotions on ROAS metrics, but rather because if they don’t Alibaba will throttle traffic to their stores. We have no way of verifying whether this is true, but one possibility is that successful advertising results in a higher relevancy score in the search engine result page which then leads to more sales. Perhaps there is a factor in the relevancy score that weighs more recent purchases higher than older purchases, so too long without advertising and slowing sales means you need to “reset” the flywheel by topping up ad spend. This means the true value of the ad spend is the direct sales plus the knock-on effects of being ranked higher in organic search. The second piece to this is that there are other promotion channels that merchants become eligible for when they buy ads that may not directly be accounted for in the ROAS figure, so there could be some under-attribution.

While we have many points to make, often the best rebuttals are simple, so we will leave it at this: Despite low ROAS and new advertising options opening up the past few years, we actually saw more ad spend on Taobao, not less.

Competition.

China is notorious for how brutal their startup competition can be with hundreds of companies going after the same market: Meituan’s success, for instance, was a result of the “War of 1,000 Groupons” (an ode to how many copycats they had to beat out). Given this backdrop, it should be no surprise that competitors are not disheartened by Alibaba’s size, continue to try and gain market share of China’s ecommerce, and supplant Alibaba as best they can.

Bytedance. Following our comments from the prior section, Bytedance with Douyin/Tiktok has been one of the newest distruptors in ecommerce. With a highly addictive app that users often spend over an hour a day on, Bytedance facilitates RMB 500bn of GMV. The large amount of user time spent with full screen videos makes Douyin a natural venue to serve ads and facilitate in-app commerce. While the nature of these purchases tends to be discovery-driven and more impulsive, they are building out their search capabilities that could serve more intention-driven purchases in the future. Their large base of videos could serve as a great way for users to learn more about specific products and see them in use. There is a very clear use case for verticals like makeup where a user could search “dark lipstick” and get a wide range of high-quality videos that showcase different products. In the future, Douyin may allow users to directly purchase it in app (even if it is not an advertisement with a link). However, most users do not think “Douyin” when they want to buy something—and changing how a user interacts with a product is hard. Also, today many merchants drive traffic back to Taobao or Tmall stores, but Bytedance is clamping down on that as they are trying to get merchants to set up stores on-platform. But even when they do, it is often for a limited amount of their SKUs. Generally, we see Douyin as a threat to Taobao’s discovery feed and livestreaming GMV, which serve buyers’ impulse-buying/discovery-based purchases, as well as a potential threat to stealing more of the ad budget (as mentioned above). However, Alibaba still has much better data and users visit Taobao with clear commercial intent, with most of the consumer we spoke with having positive opinions of the Taobao Feed recommendations. As long as Alibaba keeps users on their apps, they will get their share of recommendation commerce.

Although Douyin is wading into the ecommerce space, their core focus is still video. They compete with Alibaba for eyeballs and advertising dollars.

JD.com. For about a decade, JD.com was Alibaba’s most formidable (and really only) competitor. JD.com has a unique value prop vs. Alibaba as they take everything in-house: they own their own inventory so there is no concern of fakes, they operate their own logistics network with is very fast and reliable, and they have a good consumer-centric culture. It is for these reasons that JD.com tends to be the ecommerce provider of choice among the wealthiest, despite moderately higher pricing (although ecommerce platform usage is far from mutually exclusive). JD.com’s no hassle, free returns policy is also valued by consumers vs. Taobao/Tmall purchasers who have to deal directly with the merchant (some who are wonderful, others not so much, and a “xiao er” mediates the dispute). As mentioned, Tmall helped Alibaba gain consumer mindshare as a higher end platform, and they continue to lean in on that with Tmall Luxury and Tmall Flagship Store 2.0, but today JD is still generally seen as (slightly) higher end. Our conversations with dozens of consumers showed that most would recommend a friend go to JD.com for high end items followed by Tmall, then Xiaohongshu (a China app that can be best described as a cross between Pinterest and Instagram), so Alibaba still has work to do to gain more mindshare here.

JD mainly competes with Tmall for higher ticket, branded products.

To address JD.com’s superior logistics, Alibaba is investing more in Cainiao, their in-house logistics platform that connects with 3PL providers, to decrease delivery times and errors. However, for quick and reliable delivery, JD.com clearly wins today, with most of the consumers we spoke with (in Tier 1 cities) getting one day shipping with JD.com and a mix of one, two, three day shipping with Cainiao (two day seemed to be the most common). However, Alibaba is still investing in Cainiao and has a long-term goal of delivering anywhere in China in 24 hours (and international in 72 hours). Remember though, most of the “shipping time sensitive” purchases are already on JD.com and JD.com getting to same day shipping is much harder than Alibaba simply catching up to where JD.com is now, so JD.com is at risk of losing some purchases to Alibaba as their logistics advantage closes. In our talks with consumers, it was very seldom that a user cancelled or didn’t buy an item because it didn’t arrive quick enough, so we believe that logistics is increasingly less of a differentiating factor once you get to 2-3 day shipping. (Of course, consumers may always want quicker shipping—we just do not see them consistently comparing shipping times across different platforms after they have found an item they want.)

Meituan. The truly time sensitive purchases are now going to Meituan and Ele.me, which originally focused on food delivery but has expanded to delivering anything locally available—usually in <40 minutes. Local selection is of course more limited, but can still cover all of a consumer’s higher frequency purchases like groceries, household products, medicine, and personal care items. High frequency items drive consumer habits and leaves an open window every order for the provider to move more purchases into the consumer’s basket. While the cross-sell is tough with only sourcing locally, Alibaba cannot afford to capitulate these high frequency purchases. Alibaba invested in Ele.me in 2016 and acquired them in 2018. While Ele.me has a distant 2nd place market share with Meituan commanding ~65% of the local delivery market, it is a strategic asset that they can leverage with some of their other New Retail initiatives, especially their grocery push. In our conversations with consumers, they tend to use Meituan for food delivery, grocery, and some other goods like paper towels and notebooks. In order for Meituan to become a real threat to Alibaba’s Taobao and Tmall businesses, they would have to aggressively expand selection, which will naturally lead to trade-offs in delivery efficiency, not to mention the price of a personal carrier limiting use cases. In some sense, these high frequency purchases are worth more to Alibaba than Meituan as getting consumers in their Alibaba Ecosystem presents more selling opportunities given their larger variety of goods, but Meituan’s whole business revolves around these high-frequency purchases, so they will not cede them (at least without putting up a big fight). Critically though, we think it will be very hard for Meituan to move past food delivery, grocery, and fast-moving consumer goods (FMCG) without their delivery value prop deteriorating, a move that will quickly lead to an undifferentiated service.

Meituan mainly competes with Alibaba’s Local Services (Ele.me and Koubei) for restaurant recommendations and food delivery.

Pinduoduo. Entertainment, social functions, and even cheaper goods were how PDD differentiated itself from Taobao. PDD levered group buying as a customer acquisition strategy, while also keeping high engagement with gamification features. This was an incredible combination to attack user growth &retention and is how they were able to surpass Alibaba as the ecommerce platform with the most buyers in China (824mn vs Alibaba’s 811mn). However, in the context of Alibaba’s existing consumer spend, there is relatively muted overlap. This is because PDD’s target market tends to be lower-income, rural China and the purchases are more spontaneous. Careful to not generalize all consumer behavior, we see PDD similar to an outlet mall where goods are cheaper and usually of lower quality. Most importantly, the channel precludes many consumers from wanting to shop there for certain items. Furthermore, more purchases start on PDD through friends sharing or their discovery feed than search, whereas most people shop on Taobao/Tmall with intention. Admittedly, discovery has become a more important means of incremental sales, which is where we see PDD and Taobao overlapping. (Taobao Deals aside, which is a platform launched to directly compete with PDD.) However, Taobao benefits here from having better consumer data and more merchant products (or both lower and higher quality) which translates to better targeting. While we don’t want to dismiss PDD as they have accomplished something incredible, we just see the nature of these purchases as different and not often cannibalistic. This is not a zero-sum game, and spending across both platforms is likely to continue to increase. We will, however, acknowledge that incremental sales are more likely to go to new channels (PDD, Douyin, Kuaishou, Xiaohongshu), but this is because they are growing the market with new use cases. This does not imply that Alibaba market share will continue to fall, but spend per consumer is a far more relevant statistic, which has continued to go up every year, despite averaging down with lower income consumers—70% of new users have been coming from lower tier cities. (Alibaba market share was likely unsustainably high anyway at ~60%, as Amazon in the US has around ~40%. In the context of anti-trust scrutiny, more competition can be a good thing.)

Pinduoduo mostly targets the price-sensitive consumer – a userbase Taobao initially controlled, then shed in order to gain legitimacy with US investors. They have recently forayed back into the space with Taobao Deals.

Shown below is spend per user and how it comps to competitors. GMV per annual buyer has grown from RMB ~6,500 to almost RMB ~10,000 despite overlapping with the period that PDD gained 800mn+ users that spend RMB ~2,000. The concern we hear from most investors on PDD is that they have built up their business on low margins so they will be better adapted to move upmarket and Alibaba will not be willing to undercut themselves: this argument harkens back to the Innovator’s Dilemma framework. This framework, however, does not actually apply here for two simple reasons: 1) Alibaba has already committed to invest in the Money for Value space and has already rolled out a competitor product—Taobao Deals—with 150mn+ MAUs, as well as refreshed their flash sale product, Juhuasuan. 2) Their adjusted EBITDA margins have dropped from 57% in 2014 to 27% last fiscal year—clearly, they are not running their business to a margin metric and there was no dilemma moving down market. Alibaba’s willingness to forgo margin is similar to a sentiment Amazon Founder Jeff Bezos expressed in an early shareholder letter: “Our pricing strategy does not attempt to maximize percentages, but instead seeks to drive maximum value for the customers and thereby create a much larger bottom line—in the long term.”

It also shouldn’t be understated how hard of a task it is to go upmarket either. Consumer associate certain distribution channels with specific expectations and a company’s willingness to attack higher margin segments is in no way an advantage. That’s not to say PDD won’t have some success breaking into new categories, but Alibaba had to launch a whole separate platform from Taobao to move upmarket (Tmall) and then invest prodigiously in support and anti-counterfeit measures to ensure high quality. In fact, PDD’s early prodigious growth was largely a result of Taobao stomping out counterfeit manufacturers—who then moved their storefronts to PDD. This is something PDD will have to contend with if they seek to move upmarket. Additionally, moving upmarket risks secluding their current consumer base and retailers risk brand dilution coming onto the platform. Furthermore, most purchases on PDD are price-driven with no real recognizable brands and it will be hard to win them as the point of brand building is usually to demand higher prices, which is at odds with PDD’s current value prop. Lastly, they will also have to catch up to Alibaba who is well ahead of them on shipping times with Cainiao. While PDD has some initiatives around getting more brands onboarded and building out their logistics capabilities, these are not at all easy problems to solve. These tradeoffs give us confidence that PDD is not an existential threat to Alibaba, especially when considering the ecosystem Alibaba has built.

Alibaba. Alibaba benefits from having ~10mn merchant sellers with the widest selection across both low-end products on Taobao and high-end products on Tmall, with the ability to cross-seed traffic from Taobao without making brands feel their image is being diluted. Merchants on Taobao are known for being very responsive to consumer questions with 40% of all transactions involving a merchant query prior to buying with many consumers receiving responses within minutes. The rating and review system on Taobao keeps merchants very invested in making their consumers happy, with merchants generally being very accommodating for product issues and often dropping an extra small knick-knack or sample into purchases (the large team of xiaoers act as a backstop should a customer still be unhappy). This effectively turns merchants into their own customer service, fielding product questions and addressing issues. Merchants also devote significant effort to curating their store content for Taobao, including videos, livestreams, and affiliated content—all of which not only helps educate their prospective customers, but also is difficult to port over to other platforms in full. Hosting a lot of this content is Alibaba’s Weitao, which is sort of like a commerce-oriented Instagram that is integrated directly into Taobao. Weitao users can follow businesses or KOLs to see educational and entertaining content about brands or products. Many Weitao KOLs, who get paid commissions for sales, find it to be such a compelling platform that they do not bother building up much of an audience anywhere else. This is all activity that is unlikely to leave Taobao. Additionally, as mentioned, Alibaba has virtually all of a consumer’s purchase history (among other data), so they are well positioned to have the most personalized product suggestions. Furthermore, Taobao has multiple selling formats that allow merchants the most options in how to sell their products from livestreaming and short-form videos to branded stores or promotional flash sales—all of which is supported by Alipay integration and Cainiao’s logistics. Lastly, if you want to reach over 800mn+ consumers who spend RMB ~10,000 annually, you have to be on Taobao.

There is no doubt that Alibaba would be a much better business financially if JD.com, Pinduoduo, Meituan, and Bytedance never existed. But generally speaking, fear of competition has driven Alibaba’s margins down over time as they continue to invest heavily in making the consumer experience better. This is actually exactly what you would want to see though, as the alternative would be very concerning.

If you remember our eBay conversation earlier in this report, one of their biggest mistakes was not taking over more of the transaction: they didn’t help with shipping, fulfillment, customer service, or merchant support. The result of this was two-fold: 1) poor consumer experience when buyers were inevitably let down, and 2) competitive advantages that dwindled over time as more places to connect buyers and sellers popped up. eBay wanted to be a pure marketplace and keep the high ROIC and margins that that entailed, and even today they have some of the highest gross margins of any marketplace. Amazon, of course, took the opposite approach, and built out all of the infrastructure needed to provide the consumer with the best experience, which while of course is costly, is why Bezos famously touts “Your margin is my opportunity.” Fast forward a few decades, it’s so clear which approach was better that we don’t even need to say it. We bring this up to make the point that Alibaba has transitioned over time from essentially eBay’s modus operandi with minimal enduring competitive advantages to a hybrid between the two. And this was happening long before the new set of competition was an issue. Every year that goes by, Alibaba reinvests to make each transaction a better experience with more efficient warehouse picking, slightly faster shipping, better product recommendations, new selling formats, and deepening the value of their buyer & seller network with products like livestreaming, Weitao, and short-form videos. We won’t make the claim that Alibaba is as well insulated as Amazon is with Prime lock-in and merchants’ inventory literally stored in their warehouses, but there is simply no ecommerce player that could replace what Alibaba does today at the scale they do it.

We understand the fear of competition: Pinduoduo is gaining share on lower end commerce, JD.com is relentlessly attacking the high-end, Meituan is going after high-frequency local, and Kuaishou, Douyin, and others threaten share in discovery commerce. But Alibaba has a strong hand to remain relevant for a long time with the deepest product catalog, the most selling formats, a unique product description platform, the most purchase data with a 3rd party ad network to drive traffic, and over 10mn merchants who are high invested in Alibaba’s platforms with it often being their most important sales channel. Add in 800mn+ buyers who buy an average of twice a week, seamless integrations with the country’s largest payment method—which itself is a large funnel of traffic—and Cainiao’s logistics network, and you can see why we are not worried for Alibaba. This is before even mentioning all of the strategic initiatives and assets in New Retail, Money for Value, augmented reality, and many others described below that further purport a unique value prop.

Open Sesame.

New Retail.

Alibaba has been focusing on what they call “New Retail,” which is ironically physical retail (but with a software layer). There have been three big developments here so far, and most of them relate to grocery because of its high frequency, room for consumer improvement, and large TAM (estimated >$1.5tn and growing). As mentioned prior, since physical retail was less developed in China, more of an emphasis was placed on ecommerce earlier on. However, digital commerce could not fully fill the need for more grocery stores as many consumers like to browse markets and see & smell the food before buying. Additionally, most shoppers buy food multiples times a week, which means the products must be close to the consumer. The grocery category is also tougher to penetrate because many foods require cold storage and building out cold-chain logistics is very capex heavy. The easiest solution to getting customers cold food quickly is simply to build out a grocery store footprint where the store also serves as a mini-storage facility for their inventory. This, tied with the strategic rationale of why grocery is important mentioned in the Meituan section (high frequency purchases increase user tie-in and drive increases in total spending across services), is why Alibaba has opted to focus on physical grocery stores and try to link them to their digital platforms.

Taoxianda. This is effective a “store OS” that helps integrate online and offline channels with inventory management systems. This was initially rolled out and implemented at a portion of Sun Art’s stores, a Chinese supermarket chain with ~500 physical stores that Alibaba invested in. This software makes all of a retail store’s inventory shoppable online and plugs into Alibaba’s different demand channels and logistics platform for delivery. Taoxianda enables inventory in Sun Art’s stores to become available to users of Ele.me and Tmall supermarket, which expands grocery selection and range while speeding up delivery times. After successful trials with Sun Art, Alibaba took a controlling position in Sun Art and now owns ~72%. It’s worth mentioning that Taoxianda has a natural synergy with Alibaba Cloud as adopting this Store OS will often lead to new compute requirements.

Tmall Supermarket. This is a platform for users to order mainly groceries, but also other small consumer packaged goods (CPG) across multiple different supermarkets. Tmall Supermarket has also been tied to Alibaba’s food delivery app, Ele.me, which cross-seeds traffic and utilizes the same driver network. The strategy is to use the Tmall and Ele.me traffic to bolster their grocery delivery business, while they simultaneously onboard supply through Taoxianda.

Freshippo (or Hema in China). In addition to aggregating existing supermarkets onto their platform, Alibaba is creating their own. Freshippo is Alibaba’s new chain of high-end grocery stores that imbeds digital capabilities directly into the store with several different store formats. New features include 1) scan & go, which displays info about an item as well as offers delivery options and the ability to pay for it right on your phone, 2) digital price tags that update in real time for dynamic pricing, 3) stores as fulfillment centers with employees picking in-store and prepping orders for back-of-store delivery, 4) facial recognition payment, 5) delivery under 30 minutes within 3km, and 6) experiential retail with automated robot servers. Listed below are several store formats they are currently experimenting with. Across all of their formats, Freshippo stores become profitable within 6-12 months.

1) Freshippo Farmers’ Markets are in located in residential districts, mostly in the outskirts of cities and offer a wider variety of fresh produce and meats alongside regular market items.

2) Freshippo Mini is a smaller neighborhood store format that offers high quality supermarket items and can deliver to anyone within a 1.5km distance.

3) Freshippo F2 stands for “Fast and Fresh” and they sell fresh fruits, drinks, and other small, packaged food items that you can self-checkout from a kiosk as well as order warm food that is held in meal lockers.

4) Freshippo Pick n Gos are located at subway stops and busy intersections. A user orders ahead of time on their phone one of many different warm meal options, and then picks it up from a locker via QR code.

5) Freshippo Stations fulfill produce orders for local residents to pick up or have shipped within a 1.5km distance.

6) Freshippo Membership Store is similar to Costco, where a customer buys a membership for the right to shop there and is given discounts on bulk items in return. They charge RMB 258 vs. Costco’s RMB 299 and have over 500,000 paying members in Shanghai (the only membership stat Alibaba has disclosed).

7) Freshippo Mall is a full-fledged shopping center with family attractions, retail stores, and food options. They only have one of these currently, but it is an interesting look into how the mall of the future may turn out with all of a retail store’s inventory purchasable on your mobile phone.

While it is hard to know how the future of retail ends up, we believe that success with Alibaba’s omnichannel approach could position them at a significant edge over competitors. Many consumers still enjoy shopping in-person, but are put off by the annoyance of check-out lines, crowds, or out-of-stock items, which are problems Alibaba can solve, while further entrenching their relationship with the consumer. This will create another unique value prop that is hard to replicate as it’s in the world of atoms and not bits. Furthermore, crossing the online/offline boundary with Taoxianda and initiatives like Freshippo Mall, could result in Alibaba having the most shoppable inventory that exists simultaneously in real stores and online. This would effectively make every retail store on their systems a mini-warehouse for their ecommerce platforms while simultaneously offering the retail stores an opportunity to drive in-person traffic from their mobile apps. Success here could look like a consumer searching for a sweater online and deciding to try it on in-person from a shop they know with certainty has it in stock, and then purchasing it on their phone to have it shipped to them later so that they don’t have to carry it with them to their next destination. This is all speculative, but we think retail will move in this direction at some point, and Alibaba is well-positioned for when it does.

China Wholesale.

The remainder of Alibaba’s core commerce operations are a much smaller portion of revenue. China Wholesale operations are just ~2% of revenues, and consist of the 1688.com and Lingshoutong businesses.

1688.com is a B2B platform entirely in Chinese for domestic manufacturers and suppliers to connect with wholesalers and distributors. In order to sell on the platform, one must be a member, which costs RMB 6,688 annually and a government license to sell. This gives buyers some confidence in the legitimacy of the supplier. Banking restrictions also tend to bar any foreign companies from buying or selling on the platform given how complicated it would be to remit payment (but this is what Alibaba.com is for). Today, they have over 40mn active buyers and ~1mn suppliers who pay for the right to sell on the platform, have access to premium analytics, and get customer management services. This is the largest B2B commerce platform in China and covers a large swath of goods. As of last disclosure, of their 40mn active buyers, an average of 7mn are daily active users with 76% of buying done in-app. Renewal rates were 70%, but number of buyers was still growing ~20% with daily average buyers increasing 50%+ and paying members growing ~40%.

Lingshoutong helps small and medium-sized businesses (SMBs) digitize by offering them a slew of different tools including access to a larger variety of goods they can offer their customers, online/offline integration, delivery, promotions, and even store footprint layout.

These are both relatively small pools of revenue for Alibaba, but they help support the rest of the Alibaba ecosystem and are good businesses with less competition focused here. Last year, this segment grew 15%, partly adversely affected by Covid delays on domestic manufacturing. Alibaba should have plenty of pricing power with membership given the demand generation for suppliers and a few alternatives, but we don’t expect much more than low double digits growth over the long term.

International Retail.

There are several different platforms Alibaba puts in this segment, most of which they acquired. This segment comprises only 6% of revenue, but is considered a strategic priority longer-term, especially for them to reach their 2036 of 2 billion Alibaba Ecosystem consumers globally. Several of these platforms are tiny and do not have any disclosures, but we walk through what all of them are below.

AliExpress is a global marketplace, available in 17 different languages and 200+ countries, that connects buyers and merchants globally. However, despite their stated ambitions for a global platform, most of the supply is still sourced from China and the buyers tend to only shop for cheap goods here. Additionally, this has also become a popular channel for “part-time sellers” to buy in bulk from China and resell on other platforms, like Amazon, because it’s cheaper since they skipped the traditional supply chain with manufacturers selling directly to consumers. The last breakout was in 2019, which showed $10bn in GMV with 80mn annual buyers tilting young (60% under 35 years old). They also broke out the most popular items by country, which shows how “different” consumer demand is globally: Brazil—quartz wrist watches, Spain—vacuum cleaners, Netherlands—diamond painting cross stitches, UK—laced wigs, and the US—hair bundles with closure.

Tmall Taobao World is basically Alibaba’s domestic platform offerings ported overseas just for the Chinese consumer outside of China. This platform is aimed at the tens of millions of overseas Chinese consumers and basically allows them to keep using Taobao/Tmall even though they are abroad.

Lazada was mentioned in depth in our Sea Limited piece, but it is a South East Asian (SEA) ecommerce platform that Alibaba took a controlling stake in 2016. At that time, they were arguably the #1 ecommerce platform in SEA, as Shopee was barely a year old. However, today it looks like they have lost the lead and are a distant #2 or #3 in all of the geographies they operate in. There have been issues with Lazada management being dropped in from China and not properly localizing their offerings to the region and instead just trying to push what worked in China. Even though they are and have been losing ground, Alibaba has not capitulated SEA in any way, and we should expect increased investment here even though their chances of success in SEA seem fleeting with Shopee continuing to move very quickly and aggressively even with their seemingly insurmountable lead. That said, Lazada does still have the benefits of a huge Chinese seller and consumer base, so perhaps they can leverage that better to onboard merchants and attract users. The last time Alibaba disclosed numbers, Lazada had 70mn unique customers with orders growing ~100% y/y and 75% of parcels going through their own facilities. These statistics, however, are pre-Covid, and while they have lost significant ground since, they are likely still growing nicely given how underpenetrated the market is. Frankly though, there isn’t much evidence to support that they are doing well against Shopee. Interestingly, Alibaba does also have a large stake in Tokopedia (~28% before the last private funding round), another Shopee competitor that is merging with Gojek to form GoTo, and is closer to catching up to Shopee in Indonesia.

Trendyol is the leading ecommerce platform in Turkey that Alibaba acquired a majority stake in 2018 and later further increased their stake to 86.5% with a $330mn investment. It is currently rumored to be valued at $11bn with GMV on track to be $10bn this year.

Daraz, started by Rocket Internet (who also incubated Lazada), is the leading ecommerce platform in Pakistan. Alibaba bought them in 2018 from a rumored ~$200mn.

Tmall Global is a platform that helps overseas businesses sell to mainland Chinese consumers without the need for any physical locations (note that most large, multi-national brands that sell to Chinese consumers haver Chinese offices and are counted in China Retail). Tmall Global GMV is not broken out, but it was disclosed that they were growing 40%+ in 2020. This helps open up the Chinese consumer to more international sellers, growing their offerings, a potential advantage vs. the competition.

Kaola was acquired for $2bn in 2019 and is a membership-focused service that is geared towards higher-end, overseas, import products offered at a fair price. Essentially, Kaola places large orders to get discounts on a variety of goods and then passes along the price savings to members. While you can use the platform without becoming a member, those that do pay the $40 fee receive premium discounts, lower delivery fees, and get assigned a permanent customer service rep to help them shop. Kaola active buyers are growing at over 20%.

These businesses have some natural advantages riding on Alibaba’s commerce, payment, and shipping infrastructure, but those do not tend to extend well outside of China as lack of familiarity with local customs has been a barrier to knockout success internationally. The import business focused on the Chinese consumer seems to be better positioned as they more naturally fall in Alibaba’s circle of competence: serving the Chinese consumer. These international efforts are still important focuses for management, but frankly their efforts here seem to lack focus. Of course, this could very well change, and the opportunity remains as SEA ecommerce is still in its infancy.

International Wholesale.

This segment consist of just Alibaba.com, the very first business Alibaba launched in 1999.

Alibaba.com was originally created to help connect Chinese and international wholesalers. Today, it is the largest wholesale marketplace with 26mn buyers from 190 countries. Suppliers do not have to pay to list their items, but if they do, they get vetted by a 3rd party agency and receive an official logo (which signals some legitimacy). The annual membership fee (all members are dubbed Gold members) is either $3,500 for just the official logo or $11,000 which includes more ad spend for keywords and help creating product posts. As of last disclosure in 2020, they had 190,000 paying members with 76% renewal rates and 1.6mn DAUs and DAU buyers growing at over 100%. Renewal rates seem somewhat low, but it is likely that the free offering is compelling enough for suppliers that if they only see a muted increase in sales, they downgrade their membership. Alibaba could devalue the free service to push memberships more, but we don’t see them doing that as it would weaken the overall ecosystem. 1688.com has a lot of the same listings as Alibaba.com, but tends to be cheaper with more selection and better customer service, thanks in part to all parties being in the same time zone with no language barrier. Alibaba.com has since implemented machine translation messaging to help bridge the language gap as well as virtual factory tours to help instill further buyer confidence. Additionally, they have some other services, like omnichannel data visualization, intelligent marketing, and financial services.

Local Consumer Services.

This consists namely of Ele.me, Koubei, and Fliggy. Ele.me and Koubei were each acquired in 2018 for $9.5bn and $8bn respectively. Alibaba then merged the two companies, along with several other assets, to form Local Consumer Services. They separately raised ~$4bn of capital in 2018 at a $30bn valuation from Softbank and others. Alibaba currently retains ~73% of this business.

Ele.me, which translates to “Are you hungry?” is a food delivery service that has expanded to delivery any local goods. As mentioned in the Meituan Competition section, Ele.me is the #2 market share leader in most markets with ~35% share versus Meituan’s ~65%. In our conversations with consumers, most preferred Meituan but a few have use(d) Ele.me. While they were satisfied with the experience, they felt Meituan had better selection and delivery speed. This was due in part to Meituan having a restrictive policy that made restaurants make Meituan their exclusive delivery provider if they used them, which limited Ele.me’s ability to onboard restaurants given their smaller user base (whereas usually a restaurant would just consider the incremental demand as worth it). Since this practice of “two choose one” is no longer allowed, we may see Ele.me gain more restaurants and perhaps even more relevance. Alipay’s super app serves as a funnel for traffic for Ele.me where users can order food in the Alipay app (40% of new users in 2020 were from Alipay). In the New Retail section, we discussed Alibaba’s initiatives in grocery—and having the best grocery selection could also help boost Ele.me’s market share. Commanding a higher market share is important in local delivery as the local density effects can draw more delivery carriers and users, which kicks off a virtuous cycle: more orders allow better route matching to more carriers who can deliver more orders more quickly, which reduces the cost of delivery while increasing the carriers’ total pay and decreasing the users’ delivery costs, thus bringing in more users. Ele.me still has a smaller footprint with presence only in Tier 1 and Tier 2 cities, vs. Meituan who has started expanding out. However, it is questionable how well the economics pencil out when you go to lower tier cities which likely have smaller average order values (AOVs) and less density. Alibaba is likely still losing money in this business and will continue to for some time. It is somewhat strategic as they tie it to their grocery initiatives which tie into their core marketplaces, but it is hard to see them becoming the leader in this space anytime soon (and owing to the local density and network effects mentioned above, the winner takes a disproportionate share of the industry’s profit).

Ele.me’s standalone offerings are not quite as diverse nor built out as Meituan’s, but it is still a force to be reckoned with.

Koubei is a leading restaurants & local services platform similar to Yelp. However, Meituan owns Dianping, which is a similar service and more popular. There are natural synergies between a platform that helps in local search and Ele.me’s local delivery network that can deliver those items to the consumer, but they are still a distant 2nd to Meituan. In a consumer survey, ~70% of respondents viewed Meituan Dianping more favorably than Ele.me and Koubei. Given Meituan’s relentless focus and sharp execution, we don’t currently expect this to change. And while it is possible that Alibaba’s New Retail initiatives breathe life into their local consumer businesses, that is not our base assumption.

Fliggy is an online travel platform used for purchasing plane & train tickets, booking hotel rooms, and finding local events. Fliggy uses Alipay traffic to drive usage, but nevertheless is still a distant 2nd to market leader Ctrip. Consumers we spoke with viewed their experience on the app poorly.

All of these businesses are interesting and do have some strategic value, but as of now they are likely destroying shareholder value as investment and management focus is poured into areas they are unlikely to win outright, if at all. Investors may wonder why they don’t simply partner with the best-in-class, which could achieve much of the same benefits at a cheaper cost. That does not seem possible as Tencent is involved in most of these competitor companies and would not likely welcome a partnership. To management’s credit though, even if these businesses are losing money now, ensuring access to a fast delivery service and local services platform (even if a #2 service) could turn out to be a wise strategic move, as we can never know how the future of commerce unfolds. Today, we assign very little value to this segment (detailed in the valuation section), so we consider it largely a call option should things turn out much more successful.

Cainiao.

As touched on, Cainiao logistics is essentially their software integration with various 3rd party logistics providers that makes shipping items for merchants very simple, with the merchant able to use Cainiao to clearly see who the best logistics provider is for each order.

Alibaba started this effort in partnership with several large logistics providers and thus didn’t have a majority stake. However, they have since then been increasing their ownership stake (they now have a majority stake and it is consolidated on their P&L). Their last investment of $3.3bn in 2019 increased their stake ~12% to ~63%, implying a ~$28bn valuation (and later upped it to 66%).

Since Alibaba’s platforms source around ~half of all packages delivered (and as high as 70% by some estimates), having direct integration with the logistics providers helps increase efficiencies and speed-up delivery times. Their smart routing and sorting services reduce logistics partners’ delivery errors by >40%, which is key to reducing customer churn from poor experiences. Improvements in shipping times can be exemplified by their progress on Single’s Day: it took them 9 days to deliver the first 100mn packages in 2013 but only 2.6 days in 2018. Alibaba is continuing to invest in speeding up deliveries for their 5mn+ daily packages, including by investing in robotics and autonomous trucks.

Apart from Cainiao, Alibaba has also made direct investments into logistics providers and now holds stakes in several, shown below. (These stakes are accounted for using the equity method and are not recorded as revenues in Cainiao).

Additionally, Cainiao has built out a smart warehouse platform that enables fast product picking and packaging that leans heavily on robotics: products are packed in an average of just 3 minutes. They also have a network of over 60,000 package pick-up locations at last disclosure.