Hi! Thanks for checking us out at DJY Research. Every month, we will do a deep dive on an Asian equity. If you like our research, please subscribe. This is our first report! We have a second free sample deep dive on Sea Limited, which you can read here. Our first paywalled post was on Alibaba, which you can see the table of contents here. Those who join Members Plus will also be able to download our excel worksheets and get occasional company “updates.”

This month, we will be doing a deep dive on Bilibili.

*Please see our disclaimers at the bottom of the page and our full disclaimer here. By using our website, you acknowledge you have read our disclaimers and agree to our terms of use.

Bilibili

TLDR:

Bilibili is an online video platform that hosts various user generated content, fostering a dedicated community initially built around ACG (anime, comics, and games). Since then, the platform has broadened its user base to cover a diverse set of interests and added live streaming, gaming, and e-commerce. Below we give a brief overview of Bilibili and dive into how we think about analyzing and valuing each of its businesses.

Product Primer/Introduction

Before we jump into the analysis, check out this slideshow to get a feel for what it’s like to browse Bili’s home page on a desktop. You can see advertisements, promoted videos, weekly schedules, and leaderboards (what’s trending).

Background:

Founded in 2009 by then college student, Yi Xu, out of frustration because ACG niche websites (namely ACFun and Nico Nico Douga) were low quality and unreliable. The Bilibili site was officially launched in 2010, but still suffered from the same low operational expertise and inadequate resources that plagued other ACG websites. Nevertheless, it garnered enough traction to popularize the novel Bullet Chat feature that allowed users’ comments to flow over the video. Rui Chen, then an accomplished entrepreneur with a fondness for anime, appreciated what Bilibili was trying to achieve, but nevertheless was prepared to set up a competitor that could better execute. However, Chen was reticent to go all in as he was managing another successful business that would invariably split his time. After meeting with Yi Xu, he instead opted to invest and lend his business expertise to Bilibili as an advisor until he took over as CEO in 2014 with Yi Xu focusing on platform development as President. Shortly after taking the reins, Chen secured the rights to license Fate/ Grand Order for a mobile game in China, which would grow to be their first (and only) material revenue stream for years. It was on the success of Fate that it could continue to reinvest and grow the platform, setting themselves up for the next stage of their expansion.

*These are a few screenshots of the actual viewing experience. Rather than relegating the comments to the bottom of the page, Bilibili runs the comments over the video (these are called “bullet comments”). Users love the floating comments (they can be toggled off if not), because it’s a “constant reminder that they are not watching alone” and that they are part of a bigger community (think of how everyone cheers in a movie theater during a Marvel movie). The different colored/animated bullet comments are “premium comments” that you must pay for, typically in “Bcoin”, Bili’s on-platform currency which can also be used to purchase virtual gifts (for streamers) and toys.

For a deeper dive into Bilibili’s product and bullet comments, please be sure to check out our Details post: Bilibili and Bullet Comments.

Service:

While until last year mobile gaming comprised a majority of their revenues (~80% at the beginning of 2018), Bilibili’s mobile gaming success is mostly owed to a fortuitous licensing agreement with already popular IP (Fate/Grand Order) that fit well with its preexisting user base, and thus shouldn’t be over emphasized as we think about the fundamental value of its service. At its core, Bilibili is a video aggregation platform allowing creators to upload video content and users to easily find something of interest. It has matured meaningfully from the ACG community it was born to serve, as content has broadened to offer something appealing for virtually everyone. Nevertheless, the aura of the close-knit ACG community continues to permeate the platform, with more thoughtful and less offensive commentary than other open social communities. The quality of the community is in no small part thanks to the 100 question test users must pass to gain commentary privileges, which covers various interest-topics and acceptable etiquette, cultivating the desired user behavior best for the community. Sending a bullet chat essentially incorporates the user in the content, making it a more engaging experience and providing an opportunity to monetize as users can pay for special bullet chats like color. This friction to comment, not only selects for higher quality users and lowers the need for moderation, but also creates “buy-in”, which reduces churn without limiting their funnel of users. MAUs just reached 202mn, +55% YoY and “official members” who passed the exam reached 103mn, +51% YoY. Today, Bilibili also offers live streaming, subscriptions for premium content, and e-commerce in addition to its initial video hosting and mobile game distribution services.

This is the exam interface. Swipe right to see some of the types of questions one can expect on the exam. Of Bili’s 202 MAUs, 103mn are members who passed the exam. Of those 103mn members, 2mn are uploaders.

Monetization:

Bilibili monetizes primarily through four means:

1) Advertising.

This includes display ads, feed ads, and a prominent ad at the app’s opening screen. Notably, Bilibili has eschewed pre- and mid-roll ads, an ad format popular on YouTube, to better ensure a positive user experience amid many other video alternatives, while also keeping that “community” Bilibili originally envisioned by not over-commercializing. Rui Chen mentioned they plan to keep ad load flat at 5% (ambiguous metric), but there is still room for inventory expansion before it becomes a cumbersome experience. In our advertising analysis below, we estimate that there is an ad impression roughly every ~2 minutes, which has been corroborated by our channel checks, although it does vary by user.

*Here are a few of the types of ads run on the Bili platform. There are full video/photo ads that are displayed right when the app loads, an expanding half-screen ad that also allows you to browse the advertisers’ website, and e-commerce conversion cards that allow viewers to go directly to a store.

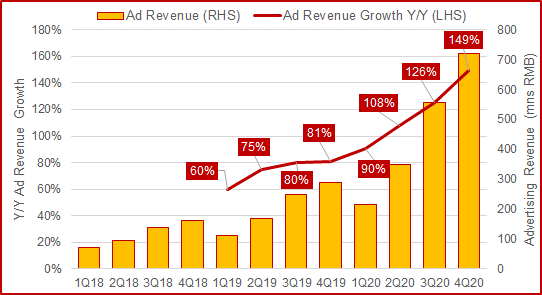

While impressions could go up overtime, the big unlock for their advertising initiatives is building better ad products for advertisers. Namely, an amped up direct response product with an easy-to-use self-serve platform and high quality attribution metrics. Coupling this with more advertisers is a powerful way to raise ad pricing (CPMs) on the platform as ad buyers spend to achieve specific ROAS targets that tend to be multitudes ahead of traditional channels. This was the playbook for the U.S. Social Media companies. Our estimated ARPU from advertising is lower versus peers like Kuaishou (~70rmb) vs Bili’s run-rate of ~50rmb. On a CPM basis though, we can see a more meaningful discrepancy with WeChat ranging from 50-150rmb, Douyin from 70-200rmb, and QQ at ~25rmb versus Bili’s ~4rmb. Below you can see that Ad revenue growth has recently been accelerating, with revenues +149% in the last quarter, almost twice as fast as they were growing just a year ago. However, the advertising story isn’t just about ad CPM parity with peers, but also the Chinese ad industry maturing with more advertisers joining the relatively new digital ad pool and buying ads on attributable return metrics (which before digital ads could never be done). While the US isn’t a great yardstick, Facebook does monetize users in their most developed North American market at ~$165 (~1,075rmb) and is still growing. PPP (purchasing power parity) adjusted by 3.5x (estimates vary) we get an ARPU of ~300rmb, which can be thought of as the full opportunity in a more mature ad ecosystem down the line. We go into more details below in our segment build.

2) Gaming.

While Tencent is the 800lb gorilla in gaming, Bilibili has been able to find some success by focusing on niche titles that fit well with its original ACG user base. Fate Grand Order (pictured below) is a Japanese game that Bilibili licensed in China with knockout success. Two years ago, it generated over a billion RMB in revenues for Bili, representing over half of its revenues. While a blockbuster gaming-hit is always welcomed, it changed the narrative of Bili in the investment community, and few felt good about the sustainability of a business model predicated on a single mobile game whose underlying IP it didn’t own.

*Fate/Grand Order is Bili’s flagship gaming product — it made up the majority of Bili’s revenues for it’s first few years, and acted as a cash flow generator that allowed it to invest in other areas (think how Search made up 99% of Google’s until recently).

However, those focusing on existing revenue pools missed the bigger picture: Bilibili’s audience was basically unmonetized. As other revenue initiatives became more mature, the top line importance of Fate/Grand Order started to fade–it represents just ~11% of revenue this year. For those unfamiliar with the Bilibili story, it might seem odd to start the gaming segment by downplaying its contribution, but it’s important to dispel the notion that Bilibili is just a one-hit mobile gaming company, as well as have a sense of how sentiment and the story has changed overtime.

As far as its current gaming strategy goes, Bilibili continues to license and partner with developers, although with middling success so far. It is also investing in developers and started an in-house studio to produce proprietary games, although not much has come from this yet. Notably, some game developers are looking to Bilibili for distribution in hopes of circumventing the Tencent ecosystem and their high take-rate (estimated ~80%). As long as Bilibili keeps its audience engaged on the core of its platform, it will have plenty of time and multiple chances to break into mobile gaming in a bigger way.

*Bilibili recently spun off Bilibili Gaming, which just raised a $28mn financing round. Bilibili Gaming was formed in 2017, operates e-sports teams for a number of games (ie League of Legends, Overwatch), manages players, and organizes and broadcasts tournaments. They still own their gaming distribution, first party studios and other licensed IP.

3) VAS (Value Added Services).

There are two main items housed in this segment: Premium Subscriptions and Live Broadcasting. Premium subscriptions are for exclusive content and include content Bilibili produces itself. Subscriptions range from 20-25rmb a month depending on subscription length. Today they have 14.5mn premium members, up over +60% YoY, which represents 43% of this segment’s revenues. Bilibili plans to continue to invest in their OGV (occupationally generated video, basically proprietary videos) content to further convert users to premium paying members.

Live Broadcasting revenues are generated from selling virtual items during live video streams. Essentially, a creator will live stream with users interacting with them through messages. It is common for users to send virtual gifts which show up on the screen and can produce special effects like fireworks, with the gift sender often receiving public acknowledgement from the creator. Bilibili has an estimated 30-45% take-rate (depending on creator size) with the creator getting the rest. While virtual gifts may seem like an odd novelty to Western readers, they are common across Asia and growing in usage. 34% of VAS revenue comes from virtual items, but their importance is much broader than the direct revenue impact. Virtual gifts are a vital revenue stream for many content creators as it allows them to directly monetize their userbase. This is important because the more money creators earn from Bilibili’s platform, the more time and energy they will put in to produce more content for it, which in turn brings in more users. Having creators make money is an essential underpinning of a vibrant and durable platform ecosystem. However, having to share a majority of revenue is also a negative and will weigh on incremental margins (expanded on below). Additionally, Bilibili has started to pay up for exclusive rights, like their 800mn RMB, 3 year contract to broadcast the League of Legends eSports World Championship. This helps increase brand visibility, decrease churn by offering something exclusive, and could have a symbiotic relationship to cross sell with their gaming and e-commerce offerings down the line.

The last pieces of VAS are Bilibili Comic, a standalone comic app, and Maoer (80% ownership), a premium platform that offers audio drama. While disclosures are limited, we know that together they are responsible for 23% of this segment’s revenues, which equates to a non-inconsequential 7% of Bilibili’s total revenue.

4) E-commerce and other.

Bilibili’s e-commerce initiatives are still very nascent, and currently focus on IP related to ACG content. Given ACG fans are fervent consumers of merchandise and they still have a large core audience here, it makes sense to start with this vertical. To speculate though, they could eventually allow creators to add shoppable posts alongside their videos or live streams, enabling frictionless purchase of whatever the creator wants to sell.

One of Bili’s e-commerce efforts showed in the form of a partnership with Taobao. The platforms aimed to connect creators and users in a virtual bazaar, with Bili creators becoming Taobao KOLs (Key Opinion Leader) and promoting merchandise through interactive content. The deal was created in the hopes of finding new ways to commercialize popular shows created by not only Bili’s creators, but also by Bili itself.

Right: Bili Mall Physical Goods

Beyond the Taobao partnership, Bili has been putting in much effort to build out their own e-commerce platform, expanding beyond physical goods to include real world events, such as anime conventions, movie showings, and festivals.

The Thesis.

Bilibili has all the classic benefits of a best-in-class internet platform: network effects, high and steady engagement, unpaid viral growth, and its users providing high quality content for others to consume. While this is an oversimplification as Bili has started to invest in content and spend on marketing to better entrench themselves, at its core Bilibili is a fantastic, capital-light flywheel and could be a phenomenal business if they fully capitalize on their monetization opportunity. Growing users means more creators want to join the platform to serve those users, while the increase in content from creators brings more users. As the user base becomes large, there is an opportunity to add other types of content, which increases time spent on the platform and draws in new users, which again draws in more content creators. While still most popular among Gen-Z, there is some signs that they are aging up and Bili now hosts all sorts of content to appeal to a variety of users. To see how far Bilibili has come from its niche ACG roots, just look to last month when a 22 year old college student garnered enough clout from his Bili videos to land an interview with Apple’s notoriously media-shy CEO Tim Cook, which generated more shares than Bilibili had users. All of this was implausible for Bili just a few years ago. With their core platform broadened, they can move into other services which simultaneous bolster their ecosystem, while helping them monetize: Livestreaming helps creators monetize their works while also increasing user engagement and loyalty, the “Sparkles” tool helps connect creators to advertisers who have a product their users would actually want, and mobile games can allow consumers to play games with characters from their favorite shows. All of this helps spin the flywheel and continues to push them towards the scale that is needed to become profitable.

The key is that there is near zero incremental cost to onboarding additional users, which gives Bili strong operating leverage and margin to spend on content, marketing, and platform improvements. By and large, the cost to produce the content on the platform is borne by the creators with a slightly delayed payout that produces positive working capital. This is the opposite of a traditional production studio (or Netflix), which has the outlay upfront and hopes to recoup the costs over many years afterwards. More importantly, the studios need to know what the viewers want and hope their bet pays off. The social media platform approach is lower risk as it outsources the creation function to users and allows them to “tell” creators what to create with views, shares, likes, and comments. The key to this model working though is scale: you need a significant number of users who are very actively engaged on the platform, directing creators to make what they want. Over time, there are feedback loops between the platform and the user with machine learning improving recommendations and the user improving the machine learning. Incredibly, Bilibili is unique in that they don’t just get signal from the user passively interacting with the platform, but actually get very valuable data from the users proactively taking a 100-question test (!!!), providing Bili with a further data advantage. (If you have ever played “20 questions,” a game that allows the guesser to pinpoint what the other person is thinking in 20 questions, then you can understand the power of this). This large time commitment (which can take as long as 3 hours for each attempt with a substantial fail rate) also builds loyalty to the platform and molds users’ habits. As Bilibili forays into content creation, they have the benefit of some of the most granular data on viewer habits, which reduces the risks of producing content no one wants. This is all before even mentioning the community, which is what users often say is their favorite thing about the platform and also the hardest to emulate.

Want to set up a competitor? You’ll start from scratch.

However, that’s not to say that there aren’t some serious concerns with their ultimate profitability. Their margin structure is rather gross for an internet platform due to their high payouts to creators. Gross margins are just 24% compared to 38% for Kuaishou and 47% for Momo, which also feel low in the context of Facebooks’ 80%. Although this could also be construed as the cost to compete against Bili is raised given how much they pay creators. Furthermore, proprietary content, which doesn’t have a revenue share would be very margin accretive, albeit with worse cash flow dynamics. Bilibili’s ambitions for exclusive content and IP can be parsed out on the cash flow statement which shows an RMB 1.6bn outlay against just 750mn of operating cash flow. It’s up in the air how much this will pay off, but it seems like the right strategy, which if successful will increase margins and raise the bar to compete against them. With RMB 9.6bn in short term liquidity, plus an upcoming Hong Kong listing slated to raise ~$3bn USD, any short term cash burn concerns should be allayed (even after layering in the other RMB 600mn+ in PPE on servers they spent last year).

While the competitive response needs to be monitored as the Chinese internet ecosystem is ruthlessly competitive, at this point the real concern is, can Bilibili execute? Never underestimate the open green fields that management can never develop. For years Twitter was very under monetized and what was flaunted as a huge opportunity by bullish investors and management ended up being a case study of mismanagement, brain drain, poor incentives, and tech debt laden decision paralysis. Maybe that is changing now, but Twitter is just finishing building the ad products Facebook built almost a decade ago. To that end, Bili does look like it’s on the right track and won’t be in monetization purgatory forever. Last quarter, revenues were up +91% Y/Y, the third consecutive quarter of revenue growth accelerating. Their efforts to broaden the service out to more users also look promising as they added 70mn+ MAUs in the past year to reach 202mn at year end, albeit with some help from COVID. To reach profitability though, they need many more years of strong growth (how much is laid out below) and it’s not clear if the Chinese ad ecosystem at maturity will be as lucrative as their counterparts in the US.

Bilibili’s success and importance has not gone unnoticed with Alibaba, Tencent and Sony all making strategic investments (making Bili one of the rare companies with investments from both Alibaba and Tencent), while Bytedance set up a competitor, XiGua. In an effort to solidify its spot as the go to long form video hosting platform, Bili is fervently investing in marketing to increase its brand awareness, which doubled in 2020 to 60%, with its goal to reach 90% awareness in 2021. In 2020 advertising expense increased to 29% of total revenues from just 18% of revenues the prior year. Part of this spend was to build out their offline presents with events like Bilibili World (annual entertainment carnival) and Bilibili Macro Link (largest ACG concert) which serve to increase engagement and brand awareness. These efforts are all to help Bili meet their 2023 year end MAU goal of 400mn (2x their current user base). Earning and entrenching consumer mindshare could help obviate the long form video market from further fractionating, although it seems likely that others will gain share as they can subsidize user acquisition indefinitely and use their other platforms to help funnel users to new products. There are other legacy video platforms like YouKu (Alibaba owned) and IQiyi (Baidu owned) that pose some threat, but they seem relatively stale and use cases don’t seem to overlap much. Anyway, we are skeptical that copying what Bilibili does will yield success, but competition can come from anywhere. Everyone is competing for the same “eyeball time” and Bilibili could still be the best long form video hosting platform, but users’ time spent on the platform could drop as other new and novel things become more popular. No one knows the future, but Bilibili’s competitive position within the existing social media ecosystem is strong and seems to be improving.

Right: Bilibili Macro Link

Unit Economics Revenue Build.

Below is our Bilibili segment revenue build. We start by annualizing year end 4Q20 results (thus it will not match reported 2020 figures) and break down each revenue driver given limited disclosures. If you’d like a copy of the excel model to play around with, consider becoming a Members Plus subscriber.

Advertising.

Our advertising build continues from our advertising table above, which shows that an ad is shown roughly every 2 minutes and they are currently monetizing at a rate of 0.117 rmb per user hour, which sizes up to roughly ~50rmb annually. This is roughly in line with how Kuaishou was monetizing last year, but they are also just ramping up their advertising efforts too. It takes a while to onboard enough advertisers to build advertiser density where they bid against each other for impressions, which coupled with better targeting, drives CPMs higher. Our current CPM of ~4 is triangulated from our ad load analysis and directionally supported by our industry contacts, but it does vary by advertiser. With users growing to 750mn, ad impressions doubling to ~1 per minute, and CPMs increasing from ~4rmb to 25rmb would equate to revenues increasing from ~3bn RMB to ~ 200bn RMB over a decade. While this might seem gargantuan, the assumptions are plausible if all goes well for Bili, but it is considered a “blue sky” scenario. The implication of this thesis playing out is that not just Bilibili will prosper, but the maturation of the ad industry will mean a “tide lifts all boats” with positive ramifications for all advertising platforms with ROAS driven buyers beyond just Bili. This will be an important trend we explore in future write-ups as well. However, it is possible that China’s market proves to be structurally different with more impressions to bid on across platforms and fewer SMBs & ROAS driven buyers that keep ad pricing from rising, but we are not convinced of that.

Mobile gaming.

In contrast to our ad build, our gaming revenue build is less aggressive. We assume paid penetration only ticks up to 1.5% over a decade with ARPPU decreasing. Of course it can exceed this, especially if Bili produces a few in-house hits where it keeps all of the economics. Even so, it’s not easy to produce a gaming hit and certainly too hard to predict it.

Value Added Services (VAS).

Our VAS build assumes some increase on ARPPU from 26rmb (implied ARPPU after annualizing 4Q20) to 40rmb as they can exercise some latent pricing power. We see paid penetration increasing from ~8% to 15% as they continue to invest in OGV (occupationally generated video).

E-commerce.

Given the limited info on e-commerce, it is probably the trickiest to model. In our conversations with Bili users, it seemed that the few e-commerce purchasers were either ardent fans of ACG with very high purchase frequency or they didn’t care about the merchandise. This informed our decision to model very few buyers (1% of MAU) with high frequency. Overtime, we think they will expand their e-commerce merchandise beyond ACG, bringing more buyers, but new buyers will be less habitual purchasers than the ACG fans and so frequency will drop.

Mature Margin Structure.

Below we extend our revenue analysis above to the rest of the P&L. There are few mature, pure play, public, internet companies to draw a comparison to so these are low confidence assumptions, but seem fair from first principles.

Gross Margin.

Overtime we have given them credit for expanding gross margin as 1) scale leads to more efficient compute and storage and 2) their proportion of proprietary content increases.

S&M.

This is another long-term question mark. If their brand strategy works then we could see tremendous operating leverage here as the majority of users go directly to Bilibili. However, it is also possible that users could be coaxed to spent time on another service and develop a habit to directly visit that site. For instance, ByteDance recently launched a long form competitor, XiGua and they could flood consumers with advertising for it. After a consumer clicks a XiGua ad they may find themselves going directly to that service in the future and Bilibili will then have “to reacquire” that user. However, this isn’t an inevitable scenario given Bili’s highly engaged users and large content library with users’ favorite creators, but helps demonstrate the ambiguity of what mature S&M looks like.

NOPAT.

We assume some operating leverage on G&A and R&D as well, which all together shows them making ~50bn RMB in EBIT or ~40bn RMB after tax (taxes of course could also change and currently benefit from the tech tax break). We assume some operating leverage on G&A and R&D as well, which rolls up to them making ~50bn RMB in EBIT or ~40bn RMB after tax (taxes of course could also change and currently benefit from the tech tax break).

Valuation.

It is important to remember our valuation is predicated on various assumptions that could be overly optimistic and others that are probably too conservative. As mentioned, the margin structure of Bili at maturity has a wide band of outcomes, so we run the range between 12-22%. Assuming the base case of 18% and a 15-25x EV/ NOPAT multiple at maturity with cumulative excess net cash of 120bn RMB (another rough assumption), Bili’s intrinsic value in 10 years would be ~$90-150bn USD or 1.5- 3x higher than what it traded around yesterday. With your required rate of return in mind and given the significant execution risks, this may not be a sufficient return unless an investor could have high confidence towards the higher band of assumptions. There is also definitely some “option” value that we are not capturing below.

Risks.

1) Mature margin structure doesn’t materialize because: a) increased gross margin pressure from content costs increasing, b) S&M proves to have limited leverage with Bili having to reacquire users, c) users or time spend drops decreasing revenue and thus limits operating leverage, d) CPMs don’t increase limiting operating leverage.

2) A glut of ad inventory keeps advertisers from having to bid each other up despite Bili building ad density. Ad density is harder to build in China than elsewhere because there are fewer SMBs (or SMEs) and ROAS driven buyers.

3) Users leave or spend less time on Bilibili because either competitor offerings are better or an entirely new platform/ service disrupts Bili.

4) Regulation of gaming and other high time spend content reduces growth opportunity and revenue.

5) China regulation like the CNSA (China Netcasting Services Association) and Central Cyberspace Administration have broad, sweeping authority and can impart rules without notice. Bilibili’s app was temporarily removed for a month from Jul 2018 to Aug 2018 after a platform content review. Any change in the relationship of the VIE structure for a non-Chinese investor also could present downside.

6) Theoretically, a creator (or group of creators at a talent agency) gets big enough that they try to negotiate a special deal with Bilibili to increase their payout, further reducing Bili’s gross margin. However, this is not likely as they already have the highest payout, not to mention the difficulty of porting an entire audience over to another platform.

7) Bili is still a cash flow negative company and if they burn through their liquidity (~3 years of runway at current burn-rate) they would be reliant on access to debt or equity markets, which may not be accessible to them.

Bilibili Model Summary.

The Bilibili model summary below is not meant to match perfectly with the other exhibit assumptions throughout the write-up. Rather it is presented so you can get an approximate picture of how different line items flow through. Of course, Members Plus subscribers will have access to the underlying excels and can change any assumptions.

Special thanks to Post M, MBI, Ram P., Dennis H., Damir B., Matt M., Tina H., Wina H., Avery S., Joe P., Joe P. (yes, another one lol), Jack G., and several others for reading early versions of this report and providing invaluable feedback.

If you enjoyed this report, please consider becoming a Member! Every month, we will publish a deep dive report on an Asian company similar to this one. We will release one more sample report next month, only Members will have access to these reports. Those who join Members Plus will also be able to download our excel worksheets and get occasional company “updates.”

*Disclaimer: I have a position in Bilibili and people who have helped craft this analysis may individually (or through funds they work at) have a position in the company. Absolutely nothing in this report is investment advice nor should it be construed as such. We make no claims to the veracity of all facts and figures presented in this report. Certain figures could be stated erroneously and certain analysis could be incorrect. Please see the full disclaimer linked above.

DJY Research, its author(s), any of its contributors, and any funds they may advise at may own securities in the companies, or related companies, written about on this website.

All rights reserved. No content on the DJY Research website can be redistributed without the express written consent of DJY Research.

3 Replies to “Bilibili”