*Please see our disclaimers at the bottom of the page and our full disclaimer here. By using our website, you acknowledge you have read our disclaimers and agree to our terms of use.

Thank you to all of our subscribers! We hope you enjoy our Coupang piece and please join our Discord to continue the conversation!

Background.

Bom Kim, the founder of what would become one of South Korea’s largest leading-edge tech companies, started his first venture with much more humble ambitions. While studying as an undergraduate at Harvard, he created Current Magazine, a “for students, written by students” publication that he later sold to Newsweek in 2001. After a short stint at the Boston Consulting Group, he wound up back in the media industry, raising $4mn for a Harvard alumni magazine dubbed 02138 (after Cambridge’s zip code). It folded in the midst of the 2009 financial crisis, but not before Bom sold it, protecting his investors from the worst of outcomes. Bom then headed back to Harvard to get his MBA and buy some time to come up with his next idea. Seoul-born but having lived in the U.S. since he was 7, he wondered whether there were U.S. businesses that could do well in Korea where entrepreneurial-spirit was often lacking, and he could marry his experience with start-ups to his knowledge of the native culture.

In 2010, just six months after starting his MBA at Harvard, Bom dropped out to create a Korean Groupon, becoming the 30th entrepreneur to mimic the very popular U.S.-based business that VC’s were falling over themselves to fund. Groupon’s revenue growth was nearly parabolic (they 20x’ed the $30mn they generated in 2009 in 2010 and then matched their 2010 annual sales in the just first 3 months of 2011). After raising an initial $2mn from investors including fellow Harvard-alum Bill Ackman, Bom moved to Korea and started “Coupang”, a play on Coupon and Korean onomatopoeia for “fun” or “surprise”. Incredibly, they generated $10mn in sales and had 3mn customers in just one year. However, this was largely the byproduct of ample Facebook ad spend during a period few thought to advertise there. Facebook’s advertiser density was so weak that CPMs were cheap enough for Coupang to show every Korean 72 Coupang ads a month. This is not to discredit them, as they did adopt a novel platform to advertise far before others recognized its power. Even more remarkably–despite their early success with “top line” numbers and prodigious growth–they realized something essential to the sustainability of Coupang’s future.

While they could easily acquire customers with very cheap customer acquisition costs (CAC), what they were offering was unsustainable: customers were solely interested in saving a few bucks and merchants were only happy to play along until they figured out that the immense traffic the “groupon” brought them never translated to positive economics. Coupang (like other Groupon-type businesses) was quite successful in getting consumers onto their platforms—after all, who doesn’t like 50% off? The problem was that once a merchant realized the model’s poor economics, they left. This is in part the merchant’s fault too as the waves of customers stressed their capacity and staff, which resulted in poor consumer experience, dashing the possibility of customers returning. Coupang was then stuck trying to fervently sign up more merchants. This worked for a while, but eventually merchants came to understand that this was a flawed customer acquisition tool and they were no longer interested in participating, which meant the Groupon-like marketplaces had their deal selection dry up, which in turn lead to consumer churn. In the meantime though, Coupang did build a nice business for themselves as they had very high gross margins and attractive cash flow dynamics with low CACs and customer payment far in advance of merchant remittance. However, there were signs that this was not maintainable. (Since we couldn’t resist, full tangent on the flaws of the business model below).

The basic Groupon business model is as follows: a merchant offers a steeply discounted deal contingent on a minimum number of customers participating. In the picture below, a merchant is offering a 50% discount contingent on getting 100 people to participate in the deal. As a consumer, you first sign up for the deal and put in your credit card info, but are only charged for the deal once the minimum number of customers join it. Since you only get the deal if you reach a critical point of participation, you are incentivized to share the deal with friends and on social media.

After the deal “tips”, meaning the minimum number of customers are reached, you are charged the discounted 50% off price, ₩24,700 in this case, and receive a coupon to redeem your deal in person. This discounted amount is then split between the merchant and Coupang (the split varies, but on average Groupon took ~40%). Assuming a 40% Coupang take-rate, the merchant in this case is effectively getting 30 cents on the dollar of what they usually get for the steak meal.

Given the low gross margins of restaurants, this means that the merchant is most likely losing money on the deal and hopes for two things that could make this make sense: 1) they can upsell the customer other items that they can make money on and 2) the customer is going to come back even without a promotion. If it was indeed just a one-time discount to get reoccurring business, then a local merchant would run the deal and lose some money initially but then have a larger regular customer base that paid full price giving them a sustainable business: the lifetime value of the customer would more than payback its customer acquisition cost.

Of course, this is not what happened: the customers interested in groupons were very price conscious and seldom bought anything other than what was included in the deal. And rather than becoming a loyal customer, they moved on to participate in the next deal. Once the merchants realized that these customers weren’t coming back, they either stopped listing groupons or rolled back their discounting. This led to worse deals and a smaller selection, which disappointed consumers and resulted in them leaving the platform. When users left, Coupang had to find new users to acquire so they could still provide merchants’ consumer demand.

Compounding the issues with the groupon business model is the fact that these are largely local deals so there is a limited pool of merchants they can churn through before saturation. This means that no matter how fast they ran, they would eventually run out of track. When merchants rationalized their deals, the growth stopped. Today, the original creator of this business model, Groupon, seesaws between middling profit and loss on contracting revenues.

Their stock is down more than 95% from its peak.

While they faced stiff competition from TicketMonster and Groupon Korea, Coupang was still #1 in the space and their business model was stronger than their overseas counterpart with very cheap customer acquisition costs that led to a marketing expense that was a fraction of global competitors. This, coupled with the fact that they received money for the groupon far ahead of time, helped them become cash flow positive early on and were set to IPO in 2013. However, despite the business humming along nicely, Bom recognized the flaws of this business model: while it was a good business for them (at the time), it was a frustrating consumer experience and merchants were also often unhappy with the outcomes. He thought that that would eventually catch up with them, and six months into their listing process, at the eleventh hour, Bom decided to indefinitely postpone their IPO.

Just one week before the prospectus would be printed—Bom pivoted the business. At the time, Bom noted that they had a service consumers liked, but not one they loved. He recalls, “if we really wanted to provide something that really mattered to customers—100 times better, exponentially better—we had to go through an enormous amount of change”. Since Coupang already had consumer awareness and some (non-restaurant) merchant relations, they opted for an eBay-like 3P marketplace model and started listing products on their website. But the 3P marketplace offered an inconsistent experience across a motley crew of sellers and very slow and limited logistics coverage nationally (half of their complaints were about shipping). This was hardly a “100x better experience”. Recognizing this—and having learned the importance of keeping customers happy so they stay on your platform obviating the need for excessive CAC spend—Coupang shifted their focus to 1P, mimicking Amazon and building out their own logistics and fulfillment network. They raised $100mn from Sequoia in May of 2014 and then another $300mn from BlackRock a few months later to build out their logistics network and refine their mobile capabilities (mobile was ~80% of traffic). They first focused on diapers and other categories for mom’s with the logic that this new period of change usually creates a window for new habits to form. Their delivery force was known for conscientious deliveries, with notes on when to ring the doorbell to not awaken a sleeping baby and leaving hand-written notes for new mothers. Despite the 180° business pivot, Coupang become Korea’s first Unicorn. Coupang’s continued execution with their ecommerce initiatives including building out their own delivery network, dubbed Rocket Delivery, allowed them to raise $1bn from Softbank in 2015 (who is now their largest shareholders with a ~35% stake after several successive investments).

By 2018, 99% of deliveries were completed within 24 hours and Coupang launched the Rocket Wow membership for just ~$2.60 a month, which, like Amazon Prime, gave free delivery on all orders without minimums. After achieving 1-day delivery, they launched dawn delivery (if you order something before 12pm midnight, you get it by 7am) and same-day delivery (if you place an order before 10am, you get it that same day). Around this time, Coupang started to become a top ecommerce provider in Korea and extended this position to the clear market leader in subsequent years. Later they would roll out Coupang Eats—their restaurant delivery platform, Coupang Play—their online streaming services, Fresh Eats—grocery fulfillment and delivery, and several other initiatives. In March 2021, they IPOed on the NYSE, raising $4.55bn, putting the company at a $60bn valuation and making Bom Kim one of Korea’s richest people with his 10.2% ownership.

Business.

Simply put, Coupang is an ecommerce company that owns their own logistics and lets 3rd party merchants sell on their platform alongside their own product offering. This is very similar to Amazon, but one key difference is Coupang actually employs their own delivery people, who number over 15,000, which allows them to control the full logistics loop from warehouse to the consumer’s door. We will touch more on alternative logistics providers later, but in short, they did this because to achieve 7-day-a-week delivery and squeeze out more delivery efficiencies. Consumers simply search for the item they want and frictionlessly buy it with their payment and address information preloaded. Coupang has the most SKUs of any Korean ecommerce player (in the millions) and the most products available with 1-day shipping. They are known to be very consumer friendly with returns as easy as leaving the product outside your door. We will elaborate further on these points in the competition and flywheel sections, but below we talk about some of their specific core offerings. Below are some product walkthroughs for their core offerings and we will touch on their other initiatives later.

Swipe through to get a sense of what it’s like to use Coupang’s app. These photos are screenshots of Coupang’s home page.

Below you’ll see a more granular selection of screenshots that show what it’s like to shop for apparel on the Coupang app.

Swipe through to see how Coupang lays out a specific category – this one is fashion. You can see a number of ads breaking up sections like the home page and the ability to further segment by item.

Rocket Delivery: This is the name of their delivery network and items available on Rocket Delivery usually are delivered in under a day. Items are either dawn delivery or same-day delivery. As mentioned, dawn deliveries are orders placed before midnight and delivered by 7am the following day and same-day delivery is for orders placed before 10am. 3P merchants who give their inventory to Coupang are eligible for Rocket Delivery as well (even though the 3P fulfillment and shipping service is technically called Jet Delivery) and items show up with a rocket next to the listing as shown below.

Rocket Wow Club: This is their membership program that allows customers to order items with free delivery and no minimums. It also allows consumers to order Rocket Fresh. They are adding more benefits to this membership like Coupang Play (a video service). The monthly fee to join is $2.50.

Swipe to see the Rocket Wow section of the app.

Rocket Fresh: This is their grocery delivery services whereby groceries are ordered before 10am are delivered by 6pm and orders placed the night before arrive before 7am. There is a minimum spend for free grocery delivery, but it is low at just $12.75 per order. There grocery delivery services utilize some different infrastructure from the rest of their ecommerce offers, such as mini fulfillment centers that are closer to the consumer.

Swiping through these photos will simulate browsing the Coupang Fresh section of the app. You can start to see the similarity and guiding design principles of Coupang’s category pages. The last few photos dive deeper into what it’s like to shop for items like fruits and meats.

Coupang reports revenues in three segments: 1) Net Retail Sales, 2) Third-party Merchant Services, and 3) Other Revenues.

Net Retail Sales consist of sale of products from their 1P business. Revenues are recorded at the price of the product sale (see our Sea Limited report for a discussion on nuances and accounting implications of 1P vs 3P). Coupang takes ownership of the inventory and houses it in their fulfillment centers which allows for rapid delivery through their owned logistics system. Often, they are able to pay the supplier on a delayed basis (trade credit) which allows them to reduce their working capital invested in inventory, which we will touch on more later. While they don’t break out segment profitability, Bom Kim has noted that the core business is profitable.

Third-party merchant services includes Coupang’s seller fee for 3rd party merchant sales–which varies by category from 3-15%, but averages around 10%–and also includes advertising revenue and delivery fees. Similar to Amazon, Coupang allows 3rd party merchants to promote listings, so it shows up in preferred placement in a customer’s search engine result page for relevant product searches.

Other Revenue includes the Rocket Wow subscription, Coupang Eats, and their other new initiatives.

Net Retail sales increased at an incredible 65% CAGR since 2016, from $1.5bn to $14.1bn LTM. Their Merchant Services, which are only disclosed since 2018, grew ~5x over just a 2.5 year period to $1.3bn LTM. GMV per customer increased from $720 in 2018 to $1,481 LTM, a 33% CAGR. Gross profits (which are consolidated across all segments) grew at a 93% CAGR from just $131mn in 2016 at an 8% gross margin to $2.5bn at a 16% gross margin. This is understating their gross margins as it consolidates money losing new initiatives, which we will explore later. Below we breakout each segment.

Today Coupang has a total of 17mn active customers, which is up +26% y/y and almost double the customer base they had in 2018.

The GMV figures below are estimated with the following methodology. 3P merchant revenues include seller fees, advertising fees, and logistics and fulfillment fees. The latter of which is dubbed the “Fulfillment & Logistics by Coupang Program” also referred to as FBC (fulfillment by Coupang). Essentially it is the same thing as FBA (Fulfillment by Amazon) whereby 3rd party merchants send inventory to Coupang’s warehouses for storage with the purposes of improving delivery speeds. We noted that seller fees range from 3-15% based on category, but our channel checks put that figure around 9-10% on average. There is no company info to inform our advertising and logistics as % of GMV assumptions so we back into it by triangulating what we have heard from our industry contacts and 3rd party GMV estimates. We place advertising today <1% of GMV with fulfillment and logistics slightly higher today. We know from talking to merchants that using Jet Delivery–Coupang’s 3rd party delivery services–and fulfillment services runs around ~30% of the item’s price, but we do not know how popular this service is among merchants. Our estimates imply that adoption is very low currently (only around ~3% of merchants) but these are very new initiatives still. As we will talk about later, this is a significant source of upside. Taking 3P Merchant Service revenues and our assumed total take-rate on that GMV gets us an estimated 3P GMV. Adding Retail Sales (which is all 1P and thus the equivalent to GMV) gets us to our GMV estimates. In the future we expect total take-rate to go up significantly, driven by higher fulfillment adoption and continued advertising up-take. More on this later.

As shown below, GMV growth is estimated to have almost quadrupled on the back of continued ecommerce penetration further fueled by the pandemic. We believe GMV grew ~80% in 2020 and if they keep up their LTM run-rate, that would imply ~70% full year GMV growth. We will loop back to GMV estimates later on and better contextualize the magnitude of this in the competition section.

Before we dive into competition, we will further explore their market, spending more time on the TAM than we typically do, given that Coupang is the market leader and Korea’s ecommerce saturation is the highest in the world.

Market Background.

We usually aren’t too focused on the TAM for most companies so long as we can confidently say it will not be a constraining factor, but with Coupang it could possibly be. As we will show in the competition section below, Coupang is the clear market leader in ecommerce in South Korea and their share gains have been accelerating in recent years as their flywheel comes together. However, they don’t have any significant international presence yet, so their future is entirely dependent on how the Korean market develops until then. (This is distinct from Alibaba who was entering many new markets and lines of business and didn’t “need” much or any core commerce growth to support the valuation. This also contrasts with Sea Limited where S.E.A. ecommerce penetration was in very early innings and those economies were also less mature so we were comfortable assuming the TAM wouldn’t be a limiting factor anytime soon). Since Coupang’s ecommerce business is the most material driver of value for them today and they currently only have a command of the Korean market, we will spend some time exploring to what degree the retail ecommerce industry will be a tailwind going forward.

With the caveat that TAM “analysis” tends to be wrong with estimates varying wildly, we will proceed cautiously. Most estimates of Korea’s ecommerce penetration put South Korea and China neck-to-neck with ~35% ecommerce penetration (portion of retail sales conducted online). This number is very high for many of the same reasons we noted in the Sea and Alibaba reports. In South Korea, there was never a developed retail market for “specialty” stores, and given the limited physical retail footprint from land being scarce (South Korea is 70%+ mountainous), stores are smaller and in-store selection has been historically limited. South Korea has internet and smartphone penetration close to 100%, which created a great combination to enable ecommerce providers to fill a gap in legacy retailers’ offerings. The retail environment used to be dominated by a few big department store chains—Lotte, Shinsegae, and Hyundai—with many other small convenience stores. This makes it distinct from the US, since there were never many specialty retail concepts that owned a category (no Sports Authority, Best Buys, or Home Depot) so selection on verticals were limited to what the big department stores provided. Furthermore, given the limited consumer options, the large department stores got greedy and often provided mediocre service. Multiple contacts noted that they price-gouge, selling products for multiples of MSRPs. In fact, the big department stores actually lobbied to pass a law in the Fair-Trade Act that made it illegal to disclose MSRP of electronic items, giving them the ability to mark-up items even more due to the price opacity. This recipe of poor consumer choice and high prices, combined with all of the other reasons people prefer ecommerce over physical retail led to very rapid adoption of online purchasing.

Understanding this backdrop is helpful when we think about where ecommerce penetration could go. Estimated total Korean retail spend varies but (including Grocery) it seems clustered around $400bn annually. Coupang estimates the TAM around $470bn for 2019 in their S1 but that includes travel and ambiguously named “consumer foodservices” (is that including in-person restaurant spend?). The data they quote shows ecommerce penetration is ~27% penetrated in 2019 versus our estimate of ~35% today. But since we believe the retail TAM is smaller than what they quote, we get similar amounts of online spend at ~$140bn. As we have shown above in our GMV estimates, we believe Coupang’s LTM GMV is ~$26bn which implies an 18% market share of ecommerce today.

In our estimates above we try our best to not be overly conservative nor exuberant, but of course our projections are almost assured to be wrong. Nevertheless, we need some sense of magnitude to size up Coupang’s ecommerce opportunity and around ~$300bn of total online sales in a decade is our best (not high confidence) judgement. We believe somewhere around 40% market share is attainable for Coupang, which is only slightly lower than what some estimates put Amazon at. This is also informed by looking at Coupang’s share of incremental ecommerce sales in the last year which was also estimated around ~40%. This implies around ~$120bn in GMV in a decade or about a 17% growth CAGR. (Amazon grew at a ~30% CAGR when they were a similar size, but the comparison isn’t appropriate because they operated in many international markets and ecommerce penetration started from a much lower point). Just as a check, we layered in population and household figures to the same estimates above to see how spend per capita would increase. Total ecommerce spend per person is only increasing ~8% versus Coupang’s growth rate that is almost double that, demonstrating that a lot of Coupang’s growth will come from taking share from others. Next we will go through competition to see why we believe Coupang will be a share gainer.

Competition.

Coupang has three main types of competitors that we lay out below: 1) Department stores/Big Box Retailers, 2) Ecommerce platforms, and 3) Internet Companies.

The Korean ecommerce market is more fragmented than other developed markets like China or the US. Coupang was actually a rather late entrant into the ecommerce market, entering in 2013, whereas other players like eBay Korea started in 2000. 11Street, TMON, and WeMakePrice all started before Coupang moved to a commerce model. The result of this was that many players have a relatively sizeable share, but their inconsistent consumer experience has meant that they hit growth plateaus as customers left. eBay Korea was the dominate ecommerce player for a while, only to be surpassed by Naver, the “Google” of Korea, who started their commerce efforts around the time that Coupang did. Coupang only usurped Naver as the largest ecommerce provider in South Korea last year, propelled by Covid tailwinds. With slight hesitation to show GMV estimates as many of these are informed from 3rd party data and not company disclosures, the graphic below shows competitors GMV estimates and the implied market share (based off of our online TAM of $140bn noted above. There is a slight distortion because we are using 2020 estimated GMV figures but an online spend figure ending in 1H21, but the competitors are not growing at the rapid rates Coupang is so it shouldn’t make much of a difference. Nevertheless, this shows the relative competitive environment and that Coupang is emerging from fairly stiff competition to claim the lead.

The development of the Korean online market is an interesting situation because the leading player, and who we will argue has the strongest competitive advantage, came relatively recently. The same way eBay was reluctant to take on logistics and fulfillment in the US, all of Korea’s 3P players (including eBay Korea) do not want to invest in a full closed loop from warehouse to doorstep as it is very capital intensive and margin destructive. Coupang opted for that playbook, and as a result they not only took the lead commerce spot, but seem to be growing the ecommerce market. Since ordering on Coupang is so frictionless with no trust issues, their growing selection means more purchases are done on their platform. Before we go through what Coupang does well though, lets touch more on each competitor.

eBay Korea. eBay launched their Korean operations in 2000 and acquired Auction in 2001 to build a foothold. In 2009, they acquired Gmarket, the leading marketplace at the time with $2.6bn GMV, cementing their leading ecommerce position until they were surpassed in 2015 by Naver. (Gmarket focused on fashion, while Auction focused on electronics and sports goods). Similar to the US version, they ran a 3P marketplace and never got involved in logistics. Buyers were encouraged to look at the sellers’ profiles and ratings to get a sense of trustworthiness, which made buying items higher friction as you never were sure if the seller was legitimate. It also meant you had to act as a detective before each purchase, making most consumers feel it was easier to buy something next time they were near a store instead. In June 2021, Shinsegae bought an 80% stake in eBay Korea for $3bn to build out their ecommerce offerings.

Shinsegae (SSG). SSG.com is a dedicated Ecommerce platform launched by one of the largest physical retailers, Shinsegae. Similar to the Walmart/ Jet dynamic, they felt they needed to retrench in order serve the online market. In 2019, they launched a Dawn Delivery service and in and a few months later they had three dedicated online fulfillment centers. In March 2021, SSG.com completed a $221mn share swap with Naver and they are exploring different omni-channel strategies to work together. As noted, their parent company bought an 80% stake in eBay and they are looking to IPO the combined company with a rumored $10-15bn valuation. Most consumers like that SSG has physical inventory where you can try on items before purchasing them, but these customers often opt to complete the purchase online (often through another provider) who offer cheaper prices and free delivery. Coupling their physical footprint with online offerings could create a good shopping experience, but they are fighting against a reputation of decades of customer price gouging.

Market Kurly. Market Kurley aimed to be a category killer in the grocery vertical, being the first to launch a dawn delivery option (even before Coupang). Their cold chain supply chain set them apart from any competitor when they launched, however Coupang was fast to follow. Kurly tries to position itself as higher quality that is sourced locally. They do have a more limited coverage area than Coupang now, but are working to address that with CJ Logistics help. Management has reported remaining laser focused on curation of food and consumers have reported higher quality groceries available through Kurly. While the perception of Kurly being fresher than Coupang Fresh is still largely still there, some of the users we spoke with noted that gap has been drastically shrinking. Grocery is an important verical because it is high frequency and spend is high. Additionally, once you can build a grocery habit with a consumer, the opportunity is ripe to cross-sell them on other products. This is why this has become an increasingly important initiative for Coupang, as they want to make sure no competitor wins this and can eventually displace their consumer relations.

Coupang’s Fresh service utilizes fulfillment centers that are closer to the consumer that ensure fresh food and quick delivery, but they are able to use their other commerce logistics infrastructure across their Fresh offerings too. This means that Coupang has a formidable advantage in logistics, which was one of the original domains Market Kurly tried to compete in. Now admittedly Coupang Fresh is still behind Market Kurly in terms of food quality, but that is because their competence in product procurement did not extend to grocery since it is a different supply chain, often relying on cold chain technologies, with a sensitive product. However, these are all solvable problems and we noted that customers have already seen an noticeable improvement. We think Coupang will continue to get better overtime, closing the quality gap, and Kurly is likely to face their own growing pains as they try to expand their service out of select metropolitan areas.

Lotte. Lotte On is the online platform operated by Lotte, one of Korea’s largest retailers. It was launched in 2019 (same year as Shinsegae’s SSG.com) to give consumers seamless access to all 7 of Lotte’s retail offerings. They also launched a membership service called LOTTE ONers, which 125,000 people had joined by the end of 2019, but limited info since then suggest it has not had the success they wanted. They are heavily investing in next-gen tech like an AI voice commerce platform, “Moving AR,” 3D virtual spaces, “Molive TV,” and more. Despite all of the buzzwords, none of the consumers we spoke with reported using Lotte On, although they do visit the physical retail stores to browse (on often purchase elsewhere). This is evident in their 7% growth during a period which Coupang grew ~70% and SSG.com grew 35%+.

11Street. 11Street is an e-commerce platform that was launched as a subsidiary of SK Telecom in 2008 and spun off in 2018. They expanded internationally with N11.com in Turkey and later entered Indonesia in 2014, Malaysia in 2015, and Thailand in 2017. In April 2021, they announced a partnership with Amazon to allow Korean consumers to search Amazon for goods in Korea and pay in Korean Won through SK Pay and other credit cards (this is Amazon’s first shopping service partnership). In 2021 they also launched a subscription brand called T Universe which gives subscribers discounts on partners like Amazon, Starbucks, E-mart, Baemin, and more. We were not able to speak with any users who used 11Street before, although several had heard of it.

WeMakePrice. WeMakePrice was founded in May 2010 as a mobile-first, social commerce platform. They focus on offering customers the cheapest prices anywhere and are currently known for their “Hot Deal” marketing tactic, which offers heavy discounts for certain products. WeMakePrice recently standardized the commission fee charged to open market sellers at 2.9% in a bid to onboard more sellers. They currently have 100,000 sellers on their platform. In 2019, they launched WeMakePriceO, a pickup/delivery service that works with over 20,000 stores nationwide. In April 2020, they partnered with GS Fresh to provide same-day fresh food service. No one we spoke with was a regular user of their service.

TMON. TMON, short for Ticket Monster, is an e-commerce platform initially founded in 2010 as a Groupon clone and currently is majority-owned by KKR and Anchor Equity partners. Once a lead e-commerce players, TMON had a failed IPO attempt in 2017. As of 2020, 30% of their revenue came from concert tickets and traveling. They also abandoned their fresh food sales and turned their focus to “Time Commerce” – selling certain items at clearance prices for short windows of time. This pivot allowed them to turn profitable for the first time in 10 years. They currently have 11mn users and are looking to IPO again. We do not view them as a direct competitor to what Coupang’s core value prop is and no one we spoke with was a user of their service.

Naver. Naver was started as an inhouse endeavor inside of Samsung, but was spun out in 1999 (Samsung sold the last of its shares in 2004). The first product they launched was a search engine and they later expanded into other areas like Q&A (think Quora or Yahoo Answers), WebToons (online comics), Naver Café (similar to Reddit), Naver TV (their YouTube but not as popular), Naver Financial (Naver Pay is the most popular eWallet in Korea by payment volume), and several other products. Today, similar to Google, most of their revenue comes from advertising via keywords bidding in search and display ads across their properties. In 2014 though, they launched Naver Window, which was designed to make offline brick and mortar stores inventory shoppable online. This 3P initiative eventually turned into Naver’s full shopping experience, which includes their Smart Stores (mini stores that host inventory for merchants without websites).

Naver is interesting because they have captive users from their search business with 28mn daily unique visitors and virtually every Korean uses at least one of their products. They can leverage this traffic to their shopping portal when relevant. Going to their shopping tab allows users to search for merchandise across the entire web and gives consumers multiple different retail options which either directs users to the retailer’s webpage or Naver’s on-platform Smart Store, which allows SMB’s to list products without building out a full website. This strategy allows Naver to “have” more searchable inventory than anyone, since even Coupang’s inventory is searchable. However, the traffic is often ported to other platforms where the transaction is completed there, with Naver only serving the top of funnel discovery function. Naver is trying to be more critical to the transaction and create a more connected system with payment and logistics common across merchants. With Naver Pay accepted across many retailers (both online and off) and in Smart Stores, they are giving consumers a more homogeneous experience with lower friction to transact.

However, it seems like all of their efforts are trying to solve for “how do you create the best consumer experience if you’re an internet company with a dominant search engine”, rather than just “how do you create the best consumer experience”. The latter Coupang is undoubtedly solving for. And if you recall, Bom Kim’s original impetus to pivot the business to 1P with fully integrated logistics was precisely because of the inconsistent consumer experience hobbling together an ecosystem of disparate sellers creates. Naver isn’t going to build out their own warehouses or logistics, so they are partnering with CJ Logistics to try to build a 3PL (3rd party logistics) provider that is capable of competing against Coupang. Naver and CJ Logistics swapped ~$530mn of stock and forged a partnership aimed at creating faster delivery. While this is an important step in making 3P transactions a better experience (recall Bom Kim said half of complaints were originally around shipping), they will likely never be able to match Coupang on speed of delivery until they have inventory that is unpacked and sorted in their warehouses, ready to ship as soon as the customer buys it. Naver recognized this and rolled out the Naver Fulfillment Alliance, which allows Smart Store operators to store their inventory at warehouses owned by one of seven different logistics companies that each plug into Naver’s data platform (this sounds similar to Alibaba’s Cainaio with some difference we will note below). This allows inventory to be ready to ship as soon as a customer orders it. But having the capability is different than having the competence.

The issue Naver faces with getting merchants to send their inventory over is that they do not have the consumer demand for a merchant to justify sending it to them. Coupang is able to turn over inventory in an average of ~3 weeks, which means that as a merchant you are fairly confident if you send your items to a Coupang fulfillment center that they will be sold pretty quickly and you will not be stuck with inventory that is exclusive to the Coupang Platform, yet can’t be sold on the Coupang Platform. So, Naver has a bit of a chicken and egg problem: Getting more merchants to send more inventory is contingent on getting more consumer demand, getting more consumer demand is predicated on having quicker delivery, getting quicker delivery is centered on having more inventory presorted in warehouses. Further complicating the issue is the fact that Coupang already does all of this!

Coupang already has 17mn customers and ~5mn subscribed to the Rocket Wow membership. If Naver wanted to go in the direction of Coupang they would likely lose, since in order to build the consumer experience Coupang has it requires a lot of demand and density. Mimicking Coupang’s playbook would require winning over users that are already very satisfied for an experience which will likely be worse than what Coupang currently offers (since a lot of the shipping improvements are slow process innovations that Naver would be behind on). Naver relying on partners like CJ Logistics can help get them started since CJ Logistics already has volumes, but their logistics network can never be as optimized as Coupang’s is for delivery (we defend this stance a little more later).

The other issue Naver faces, and perhaps most important, is that they have to balance interests of SMB and merchants far more than Coupang does or ever will. The best thing to increase conversion would be to simply keep the transactions all on Naver’s platform. They can never do this of course because the whole reason a retailer was using them in the first place was for traffic that would get the consumer onto the retailer’s property, allowing them to cross sell products and ultimately keep the consumer relationship. This is why fulfillment is only offered to Smart Store owners today because bigger retailers would be unwilling to make their inventory exclusive to a platform as they lose the ability to run inventory through their other channels (physical stores) and, more critically, lose their “uniqueness”. If we think of Shopify in the US, which supports more than a million businesses, each with fully catalogued and shoppable inventory, Shopify could easily add a search bar to the Shopify app and let consumers search across all stores for products. However, they are adamant they would never do that and that’s because it would make all of their stores more substitutable and less distinctive. If you think about the vectors that Amazon ranks products on their SERP (search engine results page), it is on factors like price, shipping speed, purchases, reviews, ratings, etcetera. Sellers move to Shopify in the first place because they want to be able to tell a story about their products that is beyond a few sterile statistics and implementing search would subject them to precisely that. That is why one of the worse experiences of Naver Shopping, being forked to a bunch of different sites and creating a bunch of extra steps to complete a purchase, cannot be solved for simply. Naver is trying to provide products like Naver Pay and hope they are adopted to help this problem, but they can’t force it. And merchants usually want to keep payment information so they have a direct relationship with the consumer that is not at the whims of a 3rd party who may change their terms and provides more limited payment data to the merchant.

Lastly, as long as anyone can sell through Naver and without Naver taking full responsibility for transactions that don’t go well, they will always lack trust. Coupang earned consumers trust by always standing by their products and willingly refunding or replacing products without any hassle. For a company like Naver, which simply aggregates listings, this seems impossible that they would be able to do this as they would have to basically “guarantee” all commerce. They are trying to authenticate Smart Stores, but it still places issue resolution on the consumer. So as long as every issue is dealt with by a different merchant, consumers will inevitably eventually have a poor experience with a merchant who is not on board with “satisfy the consumer at all costs tenet”. Some of this is just inherent in the trade-offs: it’s hard to offer both a unique experience and be consistent.

To be sure though merchants vastly prefer to sell through Naver than Coupang because of the lower take-rates, direct consumer relationship, and more data they get to keep (Coupang only provides limited data to merchants and charges for a slightly more comprehensive full data feed). However, the question isn’t where merchants want to sell but rather where they can sell. Coupang, with its 17mn customers, generates far too much demand for most merchants to give up and Coupang knows this.

Nevertheless though, Naver is likely to be Coupang’s largest competitor. While we talked a lot about the difference in commerce approach, there are still things Naver can do and is in the processes of doing that will make the Naver Shopping experience immensely better. Their partnership with CJ Logistics is a good start but if they fully copy Alibaba’s Cainiao playbook they may be able to close the gap enough that delivery speed is no longer a big differentiator in purchasing. In some sense Naver is in the position Taobao was—they both have a diverse group of distinct merchants and are trying to make the transaction more consistent. Alibaba had an advantage as all of their merchants onboarded through them so they could standardize the check-out process with Alipay and later implement a shipping solution that could be instantly available to all of their merchants. Alibaba could also have product search without forking the consumer off platform as the stores are hosted on Alibaba’s sites. Naver’s game plan will be to try to push Naver Pay and their shipping solution to as many merchants as possible, but the merchant’s objectives will often conflict with Naver’s, hampering adoption. Naver will have to convince every merchant why something is good for them whereas Alibaba could just unilaterally impose it. Given the degree of cooperation required, it is hard to see Naver and CJ Logistics becoming the connective tissue for logistics that Alibaba made Cainaio.

Some benefits Naver has though beyond a suite of popular, high frequency apps, is Naver Reviews. Consumers tend to often still go to Naver to search for product reviews as they believe they are more agnostic than what they could get on Coupang. (There also are some reports of Coupang sellers trying to game the system with reviews–similar to Amazon). This is all to say that Naver does serve a niche, namely with demand generation for merchants through their metasearch, but also with reviews and solutions like Naver Pay and logistics.

It is worth mentioning that the “holy grail” for Naver would be to be able to offer a “Universal Shopping Cart”. This used to be a rumor with Google as well, but it doesn’t look too likely to happen anytime soon. A universal shopping cart would allow a user to add anything to their cart across the entire internet and check out with one provider, basically making the entire internet a single ecommerce platforms inventory. This could be coupled with a Cainiao-like platform (inventory management software that serves numerous 3PLs) that plugs into various delivery options and even directly with retailers. This would allow Naver to become the connective tissue between a robust logistics system and hundreds of thousands of sellers. A retailer could potentially even run the same platform software for their in-store inventory management, allowing back of store fulfillment for online orders without it being exclusive to a secluded warehouse. This would still be slightly slower than a fully integrated logistics system, but it could probably get close enough overtime that the speed differential is inconsequential for most orders. Lastly, they could add something like Alibaba’s Xiaoers (team of thousands customer service reps) to mediate disputes and instill more consumer trust. Getting something like this done is nothing short of herculean though and seems implausible given the immense amount of cooperation it entails, but it is interesting to think about.

Coupang Flywheel.

We have already mentioned some of the reasons why Coupang is superior to competitors, but we will flush out that line of reasoning below. The main vectors they compete on is 1) delivery speed, 2) order ease, 3) consistency, 4) trust, and 5) selection. We are not mentioning price specifically because they are not always the cheapest option, but they are cheap enough that the differences are not material to most consumers (Our nonscientific price checks show roughly 10-15% price differences on the high end for 3P but usually it is not a noticeable difference. 1P options are the same price or cheaper than alternatives). And as we mentioned earlier, the prices they offer are still usually far superior to the legacy department stores, sometimes by as much as 30%+ (but that is because the department stores can mark-up their products egregiously). Most Coupang consumers value the other aspects of their service more than getting a marginally better price and just trust that Coupang’s prices are fair enough that they no longer check the difference.

Delivery speed. Why this is desirable is straight forward: people prefer to have stuff delivered to them quicker than slower, but why they will continue to lead here is multifactorial. We have already mentioned that Coupang has their own logistics including warehouses, trucks, and delivery people. But Coupang’s advantage here goes beyond simply the capex for logistics assets and opex for people. It is the systems they have created marrying AI and process innovation that gives them such a leg up and will make it hard for a capital rich competitor to catch up. Forget how high volumes are necessary to rationalize the cost of a delivery network, the other thing they do is allow the network to be better optimized and learn to predict demand. With the prodigious order volume Coupang receives they can utilize machine learning to optimize how much inventory to hold and where to hold it across their 10 current fulfillment centers. It is more than just the assets that matter, but how they are optimized to be at the right place that is critical and only possible with a ton of volumes running through the system. In turn, the more volume they have, the better they can optimize their network. Today 70% of the population lives within 7 miles of a fulfillment center and that will only increase as 7 more fulfillment centers are being built.

In addition to the data and volume advantage, they also are far ahead on process innovation, which is the more incremental improvements they continually work on to shave minutes off of each parcel that is delivered. It isn’t just automation with robotics and conveyor belts that enable this, but also innovative designs that reinvent parts of the delivery. Coupang started ditching boxes and opting for bags, which while saving costs, also allows them to reduce the space an order takes up in the truck. This means more packages can be delivered per truck reducing the need for multiple delivery routes along the lane. Since re-engineering their fulfillment process, this work to reduce excess packaging has eliminated 75% of cardboard parcels. (More recently Amazon has also been shipping items in bags.) The picture of the truck above shows how Coupang sorts items upstream, allowing for a Coupang delivery person to easily pick out the latest item. This is not something that can be easily copied as most logistics providers are not integrated between the warehouse that is packaging the order and the trucks route, necessitating inefficiencies. You may have also noticed that the doors open on the side of the car, instead of the back—since they own their own trucks they can design them to be tooled for delivery, shaving fractions of a minute off of each delivery. Usually, a delivery person has to jump up into the back of the truck and walk in and then put the package towards the edge of the truck, jump down and then grab it. Coupang’s method allows them to just slide a door, pull out a tray and grab the package. It is seemingly small changes like this that add up to material time savings when applied across their entire network.

Additionally, as the picture above shows, they designed ecofriendly packages when they rolled out Rocket Fresh delivery for grocery, which are more efficient and ESG friendly as they are collected after each delivery. These bags also help enable cold-chain logistics, which is very important in order to lead in grocery. There are probably many more small changes they have implemented over the years that make minor improvements in the shipping process, but together create a formidable lead. It is all of these improvements that allow them to offer 1-day delivery on virtually 100% of orders, 365 days a year, and a sizeable amount that are <12 hours. To catch up to Coupang is much more than a capital investment at this point.

Order Ease. Consumers can very easily find what they want to buy and check-out with only a few clicks. Fixed price listing (common now, but remember eBay’s Auctions used to be the most popular platform) and preloaded payment and logistics info means a customer can find an item and buy it in under a minute. This contrasts to the Naver Shopping experience which has several extra steps and the merchant may not have your info. However, any competent ecommerce platform is capable of doing this today—they all know every extra click leads to lower conversion rates. (As we detailed, Naver’s problem is unique). Coupang though does also have the advantage of a consumers order history so they can easily reorder again. Furthermore, many commonly ordered products can be put on an “automatically reorder” setting so the customer can set it up and forget about it.

It is worth mentioning though that the focus on making it as easy as possible to order, does come at the cost of building a good “discovery” muscle. Similar to Amazon, Coupang customers come to the platform with high intentionality and utilize search to purchase what they are looking for the moment they find it. This of course has positives—frictionless purchasing that doesn’t give any competitor an opportunity to win business as the consumer will complete an order in minutes from realizing they need the item—but the negative side is that consumers are not usually in exploratory mode when they open the app. This is different from Alibaba’s Taobao or SE Limited’s Shopee (to a lesser extent) where consumers like to browse more and value the recommendations. Coupang’s recommendations aren’t especially sophisticated and often include similar items to those recently purchased (similar to Amazon). We bring this up because it has some negative implications for advertising as less time spent on the platform means fewer impressions to sell. Nevertheless, the fewer impressions will likely be offset by being able to charge a higher price for ads given the higher conversion rates. Anyway, this helps us clarify that Coupang is focused on bottom of funnel, high-intentionality purchases, rather than the top of funnel discovery. The later of which will become somewhat more of focus with new initiatives like Coupang Live (detailed later).

Consistency. This one dovetails in with the other vectors (it is a flywheel after all!), but in short, a consumer can reliably expect a good experience every time they order on Coupang. This is because they own the logistics chain and half of the inventory is their own (1P) with the other half (3P) de facto kept to high standards through the ranking system and the threat of their 1P business moving into a 3P merchants’ business if they disappoint (more on this momentarily). Items are seldom out of stock, shipping is as expected, and the item received is as described or if not Coupang will take care of it.

Trust. This is won slowly over many positive customer transactions. Perhaps even more important though, when something does go wrong, Coupang makes sure to make it right. They do not tell the customer “too bad”, but instead readily offer refunds or replacements alongside apologies. Customers who are not satisfied with an item simply leave it outside their door and submit a photo of it to Coupang to receive credit. The ease at which they allow returns and readily capitulate that almost any issue is their fault has instilled significant trust in consumers. In some sense, you can think of their strategy as instead of reacquiring customers through marketing, they obviate the need to reacquire customers in the first place by avoiding potential churn events.

Selection. Selection is a vital advantage as the more stuff a platform has to sell, the more a customer can buy. The more spend that the platform can take of the consumers online spend, the less opportunities exist for a competitor to win that customer over. The idea is to become an “everything store”, which allows them to serve all of a consumer’s needs. While that is probably too extreme as there will be products that Coupang will never be able to carry (think Louis Vuitton Belts or chocolate from a local confectionary), but honestly, they can get pretty close to everything with their millions of SKUs (it took us a while to think what you can’t buy on Coupang!).

However, wide selection is harder than appreciated to build without adversely impacting the other factors we mentioned. The easiest way to build selection is to start a 3P marketplace where merchants just list inventory they already have so you do not have to invest in inventory nor worry about managing it. However, this brings in quality and consistency issues with slower shipping, customers dealing directly with merchants (who may not share the ethos of always satisfying the customer), and damaged items or fraud. Furthermore, winning over merchants isn’t so easy as lowering your take-rate. In fact, Naver offers a low take-rate at ~5% and even free listings for a limited time, but Coupang is still gaining share among 3P merchants. This because merchants care most about the platforms demand generation capabilities and tools that making selling easy. Also, selling to multiple channels creates complexity so the their profits generated through each have to be worth the effort. To generate demand though you need selection—the same chicken and egg conundrum we mentioned early with Naver. So, if a platform cannot reliably increase selection through 3P then they will have to build out their 1P inventory. This is much tougher than it seems though. Coupang has a lot of data on what SKUs sell and how quickly, which allows them to have the right amount of millions of different items. This is essential because if a platform is constantly out of the item a customer wants, they will go elsewhere. Knowing which items to buy and which warehouses to host them at in anticipation of demand takes a skilled procurement team and engineers backed by reams of data. A newcomer will not be able to buy in bulk like Coupang does so they won’t get volume discounts, which means higher prices for consumers or worse economics for the platform.

Aside from Coupang’s ability to exercise bulk volume purchasing leverage to demand discounts (something Walmart is infamous for, but all retailers do it), Coupang can also get better terms from suppliers that they are unlikely to extend to just any upstart. This all means their 1P business is somewhat entrenched, at least from the other internet platforms, as they won’t have the scale to get the prices or terms Coupang does. Most other ecommerce players are reluctant to do 1P anyway because then they have to own warehouses and hire warehouse workers, a capital and people intensive business that is far from their core competency. Coupang started by building out their 1P business and its strength brought customers in and once they had a lot of customers it was easy in turn to attract 3P merchants, which in turn attract more customers. As Bom Kim is fond of saying, merchants go to wherever the customers are. This is also why Coupang can tilt the balance between merchants and consumers largely in the consumers favor. Their 1P offerings keep merchants on edge as Coupang can always enter the category the merchant is in if they present any reason too, whether that be charging what they see as too high of a price or if the 3Ps inventory or assortment is lacking. And even then, there is a good chance that Coupang eventually sources a similar product so having good customer reviews and ratings as well as opting for fulfillment services (so delivery is faster) is probably smart to keep your position in the SERP. 1P is a powerful tool to get all their merchants on the same page and prioritize the consumer, even if they wouldn’t have wanted to otherwise. As restrictive as that may sound, it is all in order to ensure the consumer has a great experience consistently. The upside for the merchant is the ease of accessing 17mn consumers with preloaded payment and shipping information and who love to buy stuff online.

Rehashing something we glossed over above, the point on credit terms is actually critical to growing in a capital-efficient manner, so it is worth elaborating on. Coupang often doesn’t actually have to pay for their inventory upfront. Most supplier terms let them pay 30-90 days after taking delivery of the inventory. This means that Coupang can often sell an item and collect the cash before they have to pay the supplier for said inventory. This greatly reduces working capital as most of their inventory is effectively financed for free. It’s actually a bit better than since they receive cash for it before paying it out, so growing becomes a source of capital rather than use (which makes it easier to self-finance growth).

As Coupang increases in scale, so does their ability to sell through inventory rapidly with incredible visibility into demand, allowing them to negotiate better supplier prices and decrease ASPs (or keep higher gross margins as most of their customers are not very price sensitive to a couple percent difference). Today they turn inventory at ~15x a year (using our GMV estimates instead of COGS), which takes a tremendous amount of demand and very sophisticated inventory management systems to handle well. That is all to say it will be very tough for a competitor to match Coupang’s selection advantage, especially as they already have the largest 1P & 3P SKU count in all of Korea with the most warehouse space and are still pressing farther ahead.

Rocket Wow. This is the last piece of Coupang’s lock on consumers. Similar to Amazon Prime in the US, Rocket Wow allows for free shipping with no minimums on items so a consumer can buy a single item quickly without thinking what else they need to buy in order to hit a basket minimum for free shipping. This reduces the bar to order and builds a perfunctory habit of buying on Coupang the second you need something. Coupang is also copying the Amazon playbook here too by rolling out Coupang Play, their video service that is free for Rocket Wow members. For now, Coupang doesn’t have a lot of great content (one of their biggest shows is SNL Korea), but they will keep adding to overtime as the rationale of locking consumers into a loyalty program is strong. They don’t disclose members, but they are estimated to have around 5mn who pay just 2,900 Won a month (~$2.60).

Combining all of the above factors together, you can see why consumers love them so much and it shows up in the numbers. As the above graph shows, spend per buyer has gone up from $700 in 2018 to ~$1,500 currently. In the S1 they disclosed the below spend by cohort. It shows that every year spend by cohort increases, with users spending ~3.5x in year 4 as what they were in year 1. Interestingly, the spend per cohort ramps up quicker with later cohorts than earlier ones (acknowledging Covid likely distorted this in the past year). This makes sense as they have a lot more selection and better delivery in 2019 than 2016. Note that spend per buyer is indexed to year 1, so it is not clear how the $ of spend vary in the first year between cohorts, but either way in aggregate it has been trending up.

It is interesting to reflect back on Coupang’s roots as a Groupon-clone and notice that almost every issue that plagued the original business model has solved for with their new offerings. If it was Bom Kim’s aims to create something that customer didn’t just like, but loved, we think he was successful. No one consistently satisfies their customers to the extent that Coupang does and building excess consumer surplus is usually a recipe for long-term success. With an understanding of the market and competitive dynamics, we will continue with our revenue build after briefly touching on their new initiatives and new markets.

Other Initiatives.

Comprising only $180mn of revenue LTM, most of which is the Rocket Wow membership subscription fee, other revenues include a slew of new initiatives. Most of them are not only not profitable but are not even attempting to generate revenue yet.

Coupang Play. As we just mentioned, Coupang Play is their video service that is free for Rocket Wow members. They acquired an OTT player based in Singapore, Hooq, in July 2020 to build Coupang Play off of. Today content is rather lacking with no really notable exclusive content, but they intend to invest 100bn won in content ($85mn) in the near term and longer-term plan to do more original content. There are a lot of other competitors in the SVOD space including Netflix, Wavve, Tving, and Disney Plus, but Coupang isn’t trying to make the best SVOD service, just one that is good enough to reduce Rocket Wow churn and thus increase the likelihood a buyer will be a lifetime customer of Coupang. With complaints of streaming quality and content, today it hardly locks the consumer into the Coupang ecosystem but overtime they will improve it.

Coupang Live. Announced in the summer of 2021, Coupang is going to introduce their own live-streaming ecommerce channels. In contrasts to how other global peers have utilized live-streaming, Coupang plans to create studios and select KOLs (key opinion leaders also known as influencers) to sell products they endorse live, for a commission. This controlled and closed means of introducing live streaming makes sense for Coupang given they do not have much “discovery” DNA in their company. In comparison, Taobao users often use the app just to browse—remember Taobao can be translated to “find treasure”, so Alibaba having an open system where any creator can participate with users browsing as quasi-entertainment is natural to how the app has always been used. As noted, Coupang is more similar to Amazon where users come with high intentionality and get in and out quickly. Also, a more open platform would require content moderation, a proficiency Coupang has never had to build. However, if Coupang can attract popular KOLs with fun content they should be able to earn an audience and perhaps they do open it up more 3rd party merchants. Internet giants Naver and Kakao are also active here with a head start, but it is still a developing market.

Photos 1 and 2 are the home screen of Coupang Live, where users can discover livestreams and search by product/category.

Photos 3 and 4 are an ad and the actual livestreaming interface.

Photo 5 is a popup where viewers can see discounts (none for this particular video).

Photo 6 is information about the livestream including the time and host.

Photos 7 and 8 are more products and shows to explore.

Coupang Pay (Coupay). This is their payment mechanism that was launched in 2016 as Rocket Pay and later changed to Coupang Pay in 2019. The distinct one-swipe payment feature tempted users to quickly complete a purchase. While, the original rational was to simply save on transaction fees by pushing customers to their inhouse payment mechanism, it later also became a subtle retention tool with rewards and cash back. There could also be an opportunity to expand beyond just an on-platform payment service. Last year they “spun-off” Coupang Pay off as a 100% wholly owned company, which should give them more autonomy to pursue ancillary financial opportunities. To speculate, they could extend Coupang pay to other online merchants (like Shop Pay or Naver Pay) and perhaps even move into POS to support merchants with omnichannel. On the other end, they could move into other consumer financial services like lending, BNPL, brokerage, P2P, insurance or asset management. However, Coupang is a late comer to financial services with Naver Pay, Kakao Pay and Samsung Pay far ahead with high adoption, so perhaps focusing on merchants services makes more sense.

Photo 1 shows the Coupang Pay home screen

Photo 2 shows some of the banks that can be linked with Coupang Pay

MyShops. With the popularity of Naver’s Smart Store and the rise of companies like Shopify that empower a merchant to sell while still owning the consumer relationship, Coupang launched MyShops as a response. For the merchants who complain about Coupang’s fees or lack of sharing data, they can use MyShops to enable their digital store with just a 3.5% seller fee. This is still in its early days so we do not have much detail yet, but understandably merchants who wanted to get away from selling alongside Coupang’s 1P offerings may be reticent to team up with them, skeptical that sharing data could eventually invite competition. However, their ability to package fulfillment services with customers’ information preloaded into Coupang Pay, may be a good enough value prop to placate their concerns.

Coupang Flex. This is a new effort to expand their delivery with 3rd party logistics providers where someone can sign-up to deliver parcels for Coupang with their own vehicles. As such they are independent contractors and not full employees like the rest of their delivery fleet. The idea here is likely to be able to have some ability to spin-up and down delivery capacity as needed. For many years the holiday seasons plagued Coupang as their logistics infrastructure was stretched to meet the elevated seasonal demand. In response they would quickly hire a bunch of drivers to get through the season, but then they were over staffed and without the ability to directly terminate employees (Korean laws are very labor friendly), they would neglect their new hires in hopes they left. Every year it was a similar story—one executive referred to it as “stop and go”. This is a terrible strategy to build employee loyalty and keep company moral high, but we can understand that there probably wasn’t any ideal solution under such growing pains at the time as they didn’t want to use 3PLs since they didn’t have the scale or ability to ensure 3rd party delivery quality. Nevertheless, flex capacity should eliminate that problem in the future.

Rocket Direct. This is an initiative for overseas sellers to access the Korean market through Coupang’s platform. It originally launched in the US with (3-4 day delivery times), but added China more recently. This helps them buttress their selection with unique inventory that may be hard to access easily otherwise. Shipping is free for Rocket Wow members.

Coupang Biz. To help facilitate B2B commerce, especially for SMBs, they rolled out “Coupang Biz”. They intend to add value by making transactions simpler with help on VAT refunds, payment acceptance and other tax complexities.

Coupang Eats. Launching in 2019, Coupang Eats is a food delivery service that was rolled out as a separate app with no order minimums or delivery fees to gain share against earlier incumbents. Baemin, later acquired by delivery hero, and Yogiyo are the two largest food deliveries players with 50-60% and 20-30% market share, respectively. Coupang Eats has a small foothold that is estimated around ~15%, but they haven’t launched nationally yet. While Coupang was late to the fight, they are trying to differentiate by being more driver friendly, offering to cover driver payments if an order is canceled in the middle of a trip and helping drivers who become entangled with litigation in the course of work. What is really interesting though is they used their inferior market position with weak order density to their advantage.

Usually, a successful food delivery services will have enough customer demand that they can batch orders (taking multiple orders from the same restaurant to different customers) or sometimes group them (taking multiple near-by restaurant orders to different customers). This allows a delivery person to take on more orders per trip, which increases the total value of that trip. The delivery platform can then split the earnings such that the delivery person makes more money, even after lowering their payout ratio, improving the margins of the platform. Given how minuscule margins are in the delivery business (think maybe making ~$1 at maturity of contribution margin for a $24 order) this uplift in earnings is critical to achieving profitability. As a delivery platform gets bigger, their density enables them to batch more orders and without reducing efficiency as much. However, there is no way around the fact that having a customer wait for a delivery man to drop off an order to someone else is always going to be slower no matter how much density you achieve. Baemin and Yogiyo were known to batch 3-5 orders per trip which meant consumers wait times went up. Coupang launched a “single order delivery service” which was faster than the incumbents who had shifted focus from market share to making the unit economics work. Of course though, when Coupang entered the market they wouldn’t have been able to batch orders anyway since they didn’t have density. So “single order delivery” was a clever strategy (and marketing) to spin what is usually considered a weakness in the business model. As it started gaining traction among consumers, Baemin had to launch their own one order per delivery service, which no doubt ended up squeezing their margins. This reminds us of the Bezos quip: “Your margin is my opportunity”.

Interestingly, Coupang Eats has an English-friendly version, whereas Coupang is Korean-only. This may hint that Coupang plans to expand internationally with Coupang Eats as a foothold. Photo 3 is references Coupang Pay.

Other than that smart marketing strategy, Coupang is basically using the playbook that many other delivery services used—giving consumers promotions to try their service and then continuing to subsidize them until they build a habit. Their data across 17mn consumers though should theoretically let them better tailor these offers. Coupang Eats also utilizes Coupang Pay which has its own rewards which can create more tie-in to the Coupang ecosystem. Given the large amount of spend in the food category, this could become a significant increase in TPV (total payment volume) per Coupang Pay user. Of course, their mature market share is unclear and if they can never batch, their ultimate profitability will be minimal. On the other hand, South Korea with very high population density and a large affluent population, would seem to be the ideal market for food delivery so perhaps the market dynamics help boost the business model’s profitability. We have a sketch of what success here could look like in terms of valuation towards the end of the piece.

Coupang Eats Marts. Within the Coupang Eats app consumers can access what is called “Coupang Eats Marts”. This initiative closes the gap between their food delivery service and their core commerce offerings. Marts is on-demand delivery for local services, but is supported by mini-fulfillment centers embedded in cities. Using the same network they are building with food delivery, they are coupling their competence in product procurement and fulfillment to launch a new category called “Q commerce” or quick commerce. Coupang keeps some drivers at their fulfillment centers waiting for orders to come in, which decreases time to deliver to often just 10 minutes. In the US, there are some concerns that as Door Dash increases their product selection more purchases could move from Amazon to Door Dash, while we don’t totally buy this argument, Coupang is nevertheless supplanting a potential disrupter. Baemin has launched Bmart which does a similar thing but their lack of experience with product purchasing, and warehouse stocking is hurting them here. Also since Coupang has their main warehouse that can deliver items to consumers in often <12 hours, they would presumably be very quick to restock their micro fulfillment centers which typically carry lower inventory due to size constraints. This offering is also tangential to their Fresh grocery delivery service, which though not disclosed anywhere, likely shares a lot of the same local fulfillment infrastructure. While we are not sure how many items people are sensitive to receiving in 10 minutes versus same day, it is encouraging to see Coupang is still innovating. As Bom Kim has noted before, they like to try new things for a year or two and if its not working they can shut it down. For now though, it seems to be gaining some consumer traction.

International.

With a strong presence in South Korea, Coupang is looking for new markets to expand to. However, since most adjacent markets already have large incumbents, they are looking to enter new markets with a unique value prop. For most of these markets that is an offering they refer to as Q-commerce, which is similar to Coupang Eats Marts.

Japan. They launched in Japan just 4 months ago in June 2021. Available in just a district of Tokyo for now, they are using a small fulfillment center to make local deliveries with a focus on fresh grocery and other daily essentials. Initially they rolled out with around ~300 items including an assortment of 70 different kinds of produce, 4 types of meat/fish, 10 bento boxes (premade lunches) and select other daily essentials. This is a far cry from the millions of items available in Korea, but if they can achieve some success competing on delivery speed they will be able to continue to increase selection and start to spin up a flywheel. This is a different offering than what competitors offer since the orders are coming from a single fulfillment center with delivery people waiting to dispatch as soon as orders come in, saving time from having to drive to a convenience store or supermarket.

Taiwan. A month after entering Japan they rolled out a Taiwan offering available only in a subsection of Taipei. Similar to Japan, they are operating their own fulfillment center with delivery people queuing there so they can complete delivery orders in just 10 minutes. The close launch of both markets makes us think they planned both at the same time as an experiment and does not imply they expanded because they are succeeding in Japan. However, they have launched a second fulfillment center in Taipei which sounds positive, but it is still far too early to know if either market will work.

Singapore. They haven’t launched a service in Singapore yet, but they have set up an office here, hiring in various positions across logistics, marketing, and IT. Singapore is home to Shopee headquarters and it appears they want to use this location as their global head of operations given its centric location in Southeast Asia and diverse talent pool.

All of these international operations are too nascent to consider in their valuation, but they are all call options. Now we will move back to their core Korean commerce operations to see how profitable they can be at maturity.

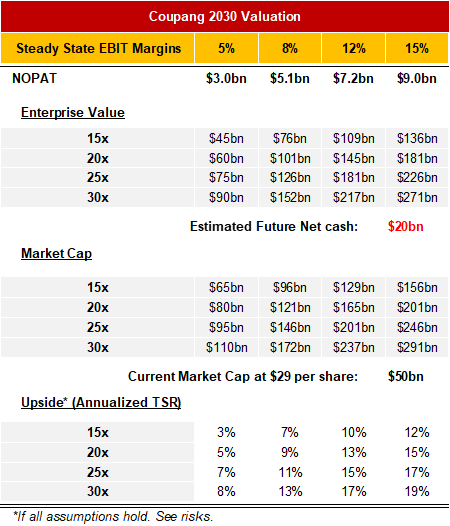

Revenue Build.

For our revenue build we took a more top-down approach assuming market share, but buttressed that by extrapolating out the implications on a spend per buyer basis Our hope is that by keeping both frameworks in mind we can approach a reasonable estimate that doesn’t implicitly assume something that is impossible (which is common if you are too high level or too granular—frankly, we think in our SE piece we tried to force precision where it wasn’t helpful and that led to a weaker estimate). We will spend most time valuing their core ecommerce business, but conclude with a Coupang Eats sketch and some commentary on their new markets.

The exhibit below takes our TAM estimates from the Market Background section. We apply a 40% market share assumption to GMV, which is informed by global peers market share. Amazon is around 40-50% depending on what you include in the TAM and Alibaba used to be 60%+. Given all of the competitive factors we discussed above we think they will continue to gain share and take a disproportionate amount of ecommerce growth. In a decade we think that a 40% market share is reasonable, driven by new buyers and spend per buyer growing. This gets a ~$120bn GMV figure for 2030 (includes grocery) which implies a 17% growth CAGR. With an ultimate 50/50 split between 1P and 3P and applying our 3P take-rate estimate (explained below), we get a revenue figure of ~$80bn or a 18% growth CAGR. However, given the 1P vs 3P distortion and various different 3P margin services, it is not a very informative figure. (We have seen some investors look at GMV or revenue multiples vs peers which is a nonsense comparison as all of these streams of revenue have wildly different profit profiles even if they are all “ecommerce”).