*Please see our disclaimers at the bottom of the page and our full disclaimer here. By using our website, you acknowledge you have read our disclaimers and agree to our terms of use.

For ease of understanding numbers, we converted most Yen figures to USD at a rate of 120:1, including historical periods. We do not fluctuate these conversion rates in line with historical exchange rates in many exhibits because we want the reader to understand the core financial operations of Fast Retailing before foreign currency fluctuations, but in USD as many of our readers (like ourselves) do not know how to conceptualize the magnitude of say ¥350bn for example.

This was our first foray into the retail industry, and we found it fascinating. We hope you do too!

Background History.

Tadashi Yanai would create UNIQLO and ultimately their holding company Fast Retailing Co., but the groundwork was laid down by his father years earlier. Hitoshi Yanai opened a men’s tailoring store in 1949 called Ogori Shoji. Opened just a short while after WWII decimated Japan’s industrial capacity, he initially sold mostly suits as the Japanese economy was restarting. With a growing sartorial need as Japan entered their “miracle” growth phase, Hitoshi opened more stores until the chain reached 22 locations and grew the selection to include foreign brands, women’s dresses, and casual wear. Around this time, his son, Tadashi stepped into the picture fresh off of his first job as a supermarket stock clerk—a job that usually started with his manager chastising him for not wearing a tie, which he saw as unnecessary for such a low-level job. This preference for comfort over formality was an early indicator of the kind of practical attire Tadashi wanted to bring to the Japanese people. After working under his father’s tutelage, in 1972 he took over the business, but it wasn’t until over a decade later that he would shift their focus.

Inspired by a trip to the United States, and particularly from The Gap, in 1984 Tadashi opened a store called “Unique Clothing Warehouse” which focused on simple, high-quality, casual clothing that could be easily browsed through and purchased at affordable prices. The new store format was a success, and they quickly expanded the chain, opening a second location a year later. Propelled by the popularity of the car and recognizing that customers were making large purchases, Tadashi decided to make the 2nd store a “roadside store”, which made it easier for customers to pull up and make bulk purchases.

The clunky name was going to be shortened to UNICLO, short for Unique Clothing, but when they registered the brand, the “C” was mistaken for a “Q” resulting in the creation of UNIQLO. The name grew on Tadashi and they kept it. A few years later, there was another name change, renaming the business group from Ogori Shoji to Fast Retailing. By 1994, there were over 100 UNIQLO stores in Japan, at which point they listed on the Hiroshima Stock Exchange. Interestingly, they focused their original footprint on less developed and more suburban areas, only opening their first urban location (in Tokyo) in 1998. To help increase consumer mindshare, they launched one of their most successful promotions, a ¥1,900 fleece campaign (~$15 at the time). The comfortable, yet good quality garment proved to be wildly popular and UNIQLO sold 2 million of them in the first year, 8.5mn in the second and a further >20mn in 2000. In a matter of a few years, UNIQLO catapulted from moderate recognition to nearly 1 out every 3 Japanese having purchased one of their fleeces. In short order, they would have over 500 stores in Japan.

Riding this momentum, they opened their first international store in London in 2001 and a store in Shanghai in 2002. They initially had ambitious plans for London, intending to open 50 stores over 3 years, but after opening just 20, they started to reduce their footprint, closing all but 5 stores as they learned that they would have to reconfigure their game plan if they wanted to be as successful internationally as they were domestically. Later, they would codify their new market launches into 3 phases: in Phase 1—the brand building stage—they launch large stores to drive brand visibility and consumer awareness. In Phase 2, they build off this platform to launch a network of standard-scale stores at a careful pace until the operation turns profitable, at which point Phase 3 would commence, which comprises a concerted acceleration of new store openings.

As they adjusted their UK plans, they also closed a nascent business venture, FR Foods, that launched them into the grocery business with their “Skip” stores. The idea was to serve the Japanese consumer with premium quality produce, but they learned that most consumers weren’t interested in spending more on groceries, and supply chain complications meant periodic shortages of products and a bloated cost structure. After expanding to 6 stores, they decided to shutter the entire division in 2004, since a path to profitable was ambiguous. Tadashi clarified that while they would continue to run experiments, they would close anything that wasn’t working within 3 years and noted that they would stick to clothing related ventures going forward.

That same year, Fast Retailing acquired Link Holdings, the owner of the Theory brand, giving them a new label to grow that focused on the high-end market. Despite these activities, UNIQLO remained Fast Retailing’s main focus and they continued to refine the concept. In 2004, they reemphasized a focus on quality products over low prices and distanced themselves from cheap quality clothes with them believing that consumers would prefer a higher quality garment even if it meant a slightly higher price. To help support this elevated brand image, they decided to focus on building larger stores that could not only accommodate their increasing collection size, but also help imprint an image of quality with “coordinated clothing displays” and a “convincing atmosphere”. With this shift they also expressed their desire to become the #1 Casual Wear company globally, supplanting the likes of Gap, H&M, Next, and Zara. In 2005, they would continue their global expansion by opening stores in South Korea, New Jersey, and Hong Kong.

Over the next decade, they would scrap and replace many of their Japanese stores to refresh them in line with the new brand image and larger store format. UNIQLO’s commitment to “LifeWear” meant a focus on comfort and quality, while still being affordable. In order to execute on this promise, they opted to produce fewer SKUs in larger amounts which allowed for greater economies of scale to hold prices down, as well as less inventory complexity. Whereas their peers like Zara and H&M would focus on quickly producing clothing in-line with the last trends, UNIQLO veered towards “timelessly” designed clothing that was often simple and clean in presentation with no visible branding (explored in more detail later). This helped reduce their need for discounting or lower batch orders that were common in the “hit-driven” fast fashion industry. The net result of this was the best quality clothing per dollar available, which fit as a staple of a shopper’s wardrobe, pairing together easily with more trendy fashion items.

UNIQLO would have a few more false starts in their international operations similar to the UK (more on this later), but eventually they would build up the UNIQLO business to over 2,200 stores, over 1,400 of which would be international. In total, Fast Retailing reached ~$20bn in annual sales in 2021 and over $2bn in operating income. Along the way they would also acquire a few other brands (Comptoir Des Contonniers, Princesse tam.tam, J Brand, among others) and launch a few of their own, the most successful of which is GU, a profitable fast fashion brand with over $2bn in annual sales.

Fast Retailing’s tremendous success, going from a handful of local stores to a global phenomenon, has made Tadashi, who still retains the President and Chairman title of Fast Retailing, one of Japan’s richest people (he periodically trades spots with Softbank’s Masayoshi Son for #1) with his 21.6% ownership stake worth ~$20bn at 2021 year end.

Business.

Fast Retailing is a holding company that owns several clothing brands including UNIQLO, GU, Theory, Comptoir des Cotonniers, J Brand, Helmut Lang, Princesse tam.tam, and PLST. Each brand designs, distributes, promotes, and oversees the manufacturing of their products and earns revenues from the sale of their clothing to consumers through their owned branded stores. Fast Retailing refers to this category of retailers as SPAs—”Specialty-store retailer of Private-label Apparel”. Retailers in this category are fully integrated, owning the full process from initial clothing design and directly working with the manufacturer (or in some cases even owning the manufacturing process) to distribution through their owned stores that exclusively carry their products. Fast Retailing commonly refers to The Gap, Zara, and H&M as the other leading SPAs. As shown below, UNIQLO is 84% of total revenues with the GU brand, their largest other brand, at 12% of total revenues. Given the size of UNIQLO relative to Fast Retailing’s other brands, the majority of our efforts will be spent analyzing UNIQLO. UNIQLO Japan is 40% and GU & their other Global Brands also over-index to Japan, which means revenues are probably split close to 50/50 Japan to non-Japan.

Below you can see their revenue segments historically. Note that while Japan is still one of their most important markets, growth has slowed considerably for the past 7 years to a ~2% CAGR versus an 8% growth rate the prior decade (2004-2014). As expected, UNIQLO’s International operation has experienced stronger growth since 2014, compounding at a ~12% CAGR. However, both UNIQLO operations have experienced net negative growth the past two years. While the pandemic has no doubt been an impediment with mandatory store closures and lower foot traffic resulting in 2021 sales still below their pre-pandemic peak in 2019, it should be noted that not all retailers suffered similarly. We will explore this more later, but while competitors Zara and H&M still haven’t fully recovered, others like Nike and Lululemon are well above their 2019 revenue levels. There is a lot to unpack here, which we will do in the Retail Industry Analysis section. GU, who we have more limited financial info available for, has grown at a 6% CAGR since 2018, and in contrast to UNIQLO, has surpassed their 2019 sales levels. Their global brands, which is a mix of 5 businesses, has had very lackluster performance. GU was broken out from Global Brands in 2018 (included in the figures below prior to 2018), so we can see that the success of GU was covering the weak performance from the rest of the group: from 2019 to 2021 Global Brand revenues are down -28%. Total group revenues are ~$17.7bn USD for 2021 (LTM, which adds one more quarter that ended in November, is only ~1% different, so for ease we will quote fiscal 2021; their fiscal year ends August 2021).

On ~$17.7bn of revenues they generated roughly $2bn USD of EBIT for a ~12% operating margin with their most mature operation, UNIQLO Japan at ~15% versus UNIQLO International at 12%, GU at 8% and Global Brands at -1%. Long term they have guided to 15% margins, but occasionally have teased the possibility of getting to 20%. In contrast to most other firms, Fast Retailing’s guidance practices tend to not layer in any conservatism and rather are used as somewhat plausible, but challenging goals to hit. As a result, they often miss their guidance, especially their longer-term goals, but Fast Retailing still believes it is important to set targets that encourage management to push harder rather than just appease Sell Side analysts. Below you can see that the UNIQLO Japan generates roughly ~$1bn in operating profits with their international UNIQLO operations and GU generating a further ~$930mn and ~$170mn, respectively. Their other Global Brands are operating at a small loss, despite the majority of the brands having been owned by Fast Retailing for several years.

As seen below, UNIQLO is responsible for the majority of their ~3,500 stores. However, while UNIQLO is 84% of revenues and >90% of operating profits, only 65% of their stores are UNIQLO’s. Part of this discrepancy is explained by UNIQLO’s larger ecommerce presence relative to the other brands, but also owing to UNIQLO’s superior sales per store.

In a given year, Fast Retailing may close well over 100 stores and open more than that, so their footprint changes often. Even within that store count, there is a lot of variation as there are many different types of stores, from the large-format global stores that are designed to draw first time consumers to the brand to small “Ekinaka” subway station stores.

We will start our analysis below with an industry analysis, looking at Fast Retailing relative to competitors.

Retail Industry Analysis.

We all know that the retail industry is huge, with the world spending well in excess of $1tn on apparel annually, which increases another trillion or so if you include other fashion items like handbags, jewelry, leather goods, etc. We know the “TAM” is there, so rather than focus on the industry from the top down, we have opted instead to focus on a set of various public retailers to get a sense of what a well-run operation looks like and let that help us build an intuition for analyzing UNIQLO.

Generally speaking, there are two strategies in apparel retail: 1) working hard to get people to spend a lot for your product, so you have a high price or 2) working hard to get the product cost down so you can charge a lower price. The first strategy bodes well for luxury goods whereby the absolute price charged is rather high and since inventory turn is low with capped product runs, the high margin enables the low sales velocity to translate into meaningful earnings. The first strategy is commonly employed with retailers who are trying to build a brand, employing ample advertising, sponsorships, and events all aimed at getting the consumer to have a “positive valence” towards a product (positive valence is a psychology term for a good feeling towards something that is usually not consciously created by an individual). They do this through “association”, one of the main principles of advertising. By putting their brand next to things that you feel good about, that feeling gets transferred to the brand as well. This is partly why Nike spends billions on athletic sponsorships: they want Nike to be synonymous with sports, training, and excellence, so anytime you work out or improve your game, you buy Nike. Charlie Munger talks about how this worked for out magnificently for Coca Cola whereby they made the soft drink an icon of American culture, prosperity, and happiness globally by inundating the consumers with ads of smiling people and Coke, so when you bought the carbonated beverage, you weren’t just getting a sugary drink, but also a feeling (one that identically tasting private label products couldn’t mimic). LVMH uses the same principles Coke did when they pay millions for celebrity endorsements: their return on investment here comes in the form of consumers who are willing to pay vastly higher sums for a Louis Vuitton handbag than an unbranded one of similar quality (there is also a social proof and Veblen good/exclusivity aspect as well).

With the second strategy, a retailer is focusing on increasing volumes, rather than price. In fact, they hope to decrease cost as much as possible in order to pass off the cost savings to consumers and spur more demand, which in turn would allow greater economies of scale to further decrease cost. These sorts of retailers work at cost efficiency and will position their brand in terms of consumer value, usually even having their biggest competitive weapon, low prices, stated in their moto. Think of Ross’ “Dress for Less”, TJ Maxx’s “Get the Max for the Minimum”, or Target’s “Expect More. Pay Less”. Their advertising is aimed at convincing you that you will get the best deals at their stores and so their operations and pricing strategies have to align with that. This means that increased earnings largely come from improving their cost structure and increasing volume, whereas a Hermès increases earnings largely from price increases with very limit volume expansion. In fact, increasing volumes too much is sure to be the quickest way for their earnings power to decrease in the long run.

Now, Ross and Hermès are the extreme examples of these strategies, and in actuality many brands and retailers fall in between. For all of the brands that are not focused on the ultra-high-end or low-end markets, retailers will shift their brand positioning to focus on another element. Lululemon, Nike, Patagonia, American Eagle, Zara, H&M, Topshop, Quicksilver, Vans, and Allbirds are all brands that price very differently, but if you were to think of the Consumer Hierarchy of Preferences (introduced in our JD piece), price is seldom a sufficient variable to induce a purchase at any of these brands. What is happening as we move from the low-end of the market to the higher-end, is that the Consumer Hierarchy of Preferences shifts from the lower order desires “I need clothing” to incorporate a myriad of different factors concerned with comfort, looks, perception of appearance, functionality, wardrobe compatibility, weather versatility, environmental impact, labor practices, and identity, amongst others. As of late, many corporations may be jumping at the opportunity for their brands to be seen as environmentally-friendly or socially-just, but for branded clothing retailers, this has been a part of their advertising recipe for decades and we don’t mean so cynically either (at least not always…). Think of Patagonia, who originally started out as a climbing hardware manufacturer and over time saw the opportunity to sell clothing to outdoors enthusiasts. They prided themselves on being “in business in order to save our home planet” and this ethos helped give their brand a unique positioning. They would become associated with all sorts of pro-environmental activities and go to lengths to reduce the environmental impact of their clothing. The test of whether a business is genuine in its mission, and not just greenwashing for greenwashing’s sake, is whether their mission came to fit a business need or whether a business was built around the mission. (We didn’t look in-depth into Patagonia, but a cursory look through their history makes it seem genuine given the founders love of nature preceded the business). However, whether a company is genuine in its mission or not is seldom clear, you can even be cynical about Patagonia’s 1% self-imposed “Earth Tax” as simply being savvy marketing, but frankly the perception matters much more than the reality.

Summing this all up in an example, a Consumer’s Hierarchy of Preferences may go from 1) sweater that fits, 2) sweater that fits that is under $60, 3) comfortable sweater that fits that is under $60, to 4) comfortable sweater that fits that is under $60 and is sold by an environmentally friendly company. Perhaps meeting just the first 3 conditions was sufficient to induce a purchase, but if there was a sweater that also met the fourth condition (environmentally friendly), then that company would win the sale every time. Companies that are able to meet more conditions on a Consumer’s Hierarchy of Preferences, past the point that the consumer would have already satisfactorily purchased the item are effectively increasing the consumer surplus. Getting more higher-level items filled on the Consumer’s Hierarchy of Preferences is crucial to creating loyal customers with a unique value prop that cannot be easily mimicked by competitors. Think of how many competitors that have rolled out products similar to Lululemon’s leggings, yet they still have a large and growing customer base. This is simply because Lulu’s brand fills some higher-level consumer preference, even if it is not obvious what that is (and could be slightly different things to different people). A good brand doesn’t have to explain what it is though; all of the emotions and narratives it evokes are simply distilled down into their name or logo. Just think of how long you could talk about what Nike means to someone who has never heard of them without ever actually conveying the full “sense” of the brand. This is precisely why most brands use imagery, music, and videos to express themselves, as much of it is outside the realm of language.

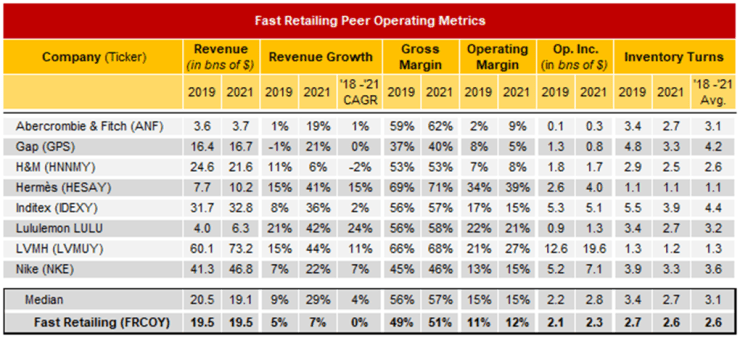

Naturally, the question arises as to which strategy is better: strategy 1 (convince people to pay more) or strategy 2 (work to charge less so people buy more). We wanted to be able to compare retailers on a level footing to address this question and in order to be able to do so we created our own metric called “Inventory Value Capture”. (For a fair comparison, we adjusted currencies and re-calendarized some financials since their fiscal years did not align with the others—see adjustments in the table below).

The table below shows select operating metrics from various retailers. We show pre-pandemic revenue and the most recent year as well as a ’18-’21 CAGR so you can get a sense of how different companies were impacted by the pandemic. Note LULU’s CAGR is higher than pre-pandemic revenue growth, showing they were actually a beneficiary. On the other hand, Inditex, H&M, and Fast Retailing still haven’t made back their pandemic losses (in terms of missed revenue growth) with growth CAGRs of 2%, -2%, and 0%, respectively, vs solid positive growth in 2019.

We also show gross margins and operating margins, as well as inventory turns, so you can get a sense of the retailer’s strategy. Clearly Hermes, with their 71% gross margins, 39% operating margins and an inventory turn ratio of 1.1x is employing Strategy 1, whereas GAP with a ~4x inventory turn and 5% operating margins appears to be employing Strategy 2. There could be some idiosyncrasies in each specific year or each company’s financial definitions that skews the metrics (we didn’t go through in-depth if any adjustments needed to be made), but at a high level we think it is a helpful framing of the retail landscape to build intuition for where Fast Retailing fits in.

Now, in order to rank the tradeoff between higher inventory turnover and higher margin, we created a metric that takes both into account. Our Inventory Value Capture metric is calculated as operating income/average inventory. Conceptually, the idea is to see how well a company turns a dollar of inventory into operating profit, while also taking into account how much inventory was needed to sustain that level of operating performance.

We will dive into the logic more now starting with the numerator. We put operating income in the numerator because it includes the full benefit of whichever strategy a company embarks on, whether that be high turnover/low margin or low turnover/high margin—either way, the resulting operating profit is captured. Some might be tempted to use gross profit, but we wanted to fully load the cost structure for all SG&A expenses in order to get a holistic impression of a company’s performance. For example, a high advertising expense, which is recorded in SG&A, might be essential in order to charge more for their product, but the expense would not be captured if gross profit was used in the numerator.

Moving to the denominator, using average inventory ties the metric to inventory turnover as well as inventory intensity of sales. The higher a company’s turnover is, the lower average inventory they would hold per dollar of revenue generated, and thus their performance on this metric would be better as more operating profit dollars are attributed to less inventory. Conversely, if a company has a lower inventory turnover ratio, then more inventory is held per dollar of revenue generated and thus it saps the company on our metric. The correlation between inventory turnover and inventory as a % of sales is shown below (R2 is high at 0.81).

The higher inventory is as a % of sales, the higher the inventory intensity of sales. The implication of this high correlation means that a company couldn’t just reduce inventory without impacting sales (by and large). Thus, if they did reduce inventory (which would improve the denominator) then the numerator (sales x operating margin) would be adversely impacted too. We break out the formula below to make that explicit: notice that sales is on top and average inventory is on bottom, which would get us sales per dollar of average inventory, the mathematical inverse of average inventory as % of sales which we showed has a high correlation to inventory turnover above. Thus, this metric accounts for the two variables we wanted to focus on, turnover and margin, with the aim of answering our question of which retailer is better when they are operating disparate strategies (convincing people to pay more vs. charging less and selling more).

In summary, meshing these two financial figures together gets us operating profit generated per dollar of average inventory held. The output is essentially how well each dollar of inventory is monetized. We dub this “Inventory Value Capture” and think it is a clean way to compare retailers who utilize very different strategies.

To apply this to our groups of peer companies below, we start by common sizing sales at “100” and input their respective operating statistics. We can back into average inventory by dividing COGS by their inventory turnover ratio, then simply taking their operating income (operating margin x 100) and dividing by average inventory to get our Inventory Value Capture ratio for each company.

Using this method, we see some interesting insights. Hermes and Inditex come out as the leading retailers despite very different approaches with Inventory Value Capture ratios of 1.57 and 1.41, respectively. Whereas Inditex has a turnover ratio of ~4x, Hermes is barely at 1x, but wallops Inditex with margins that are >2.5x higher. The net of this means that for every dollar of inventory Hermes holds, they turn it into $1.57 of operating income—better than any of its peers, but Inditex is close behind despite a very different financial profile. Hermes is the embodiment of Strategy 1, whereas as Inditex works hard at Strategy 2. As you can see, either strategy worked at dutifully can lead to retail success.

Fast Retailing looks to be towards the back of the pack at 0.63, which is suggestive of a sub-optimal optimization of inventory turns versus price. However, we should note that this is a consolidated figure so it includes their Other Global Brands and less mature international operations which no doubt drag it down. To better get a sense of how a mature UNIQLO market operates, we added in UNIQLO Japan below and took the average of the same metrics across the past four years. Many retailers suffered in 2020, the peak of the pandemic, but then some had a strong 2021 that largely offset this. Rather than trying to adjust out the Covid impact, we thought it was rather telling of the quality of business including it, as some retailers were able to weather it much better than others. Notice for instance that Abercrombie & Fitch moved from an Inventory Value Capture ratio of 0.65 above to 0.28 below (note that there could be some other idiosyncratic explanations for this though). Inditex, on the other hand, generated the exact same $1.41 in EBIT per dollar in inventory. UNIQLO Japan moves up in ranking with a margin that is ~300bps higher than the consolidated company’s and has a slightly better inventory turn. We will dive deeper into the UNIQLO operation and strategy in the next section, but this higher ranking is indicative of the fact that at maturity, and stripping out the loss-making Other Brands, UNIQLO is a solid performer. Do not get distracted by the fact that we show UNIQLO & Fast Retailing towards the bottom of the table, as the companies we included were somewhat arbitrary and we could no doubt add many more mediocre companies that UNIQLO would beat on this metric. In a similar vein, look at the companies that “beat” UNIQLO on this metric: Lululemon, Inditex, Hermes, Nike, and LVMH—these are all top tier retailers. While we are reticent to suggest improvements to Fast Retailing on the basis of some high-level analysis (and never having run a multi-national retailer with tens of thousands of employees and hundreds of millions of inventory units), nevertheless this analysis does suggest that UNIQLO could better optimize their balance of price-taking vs inventory allocation. In another sense, this is the opportunity that UNIQLO has in front of it.

Below, we will continue our analysis focusing only on UNIQLO, going in-depth into the business’ strategy, unit economics, and competitive positioning.

UNIQLO.

UNIQLO is not only Fast Retailing’s most important businesses, but one of the largest private label fashion retailers globally with $14.7bn in global annual revenues and a store footprint in excess of 2,000. From their roots in Japan (36% of stores today), they have expanded internationally with a large presence in China (41% of stores) and the rest of Asia (18% of stores), with growing operations in Europe and North America.

While it’s true that from UNIQLO’s creation the clothes they stocked and their positioning has somewhat changed, their clothes have always focused on the “timeless” element of designs. They would never take cues from the latest seasonal fashion trend, nor have their logo visible anywhere. For the past ~2 decades, they also focused exclusively on creating clothing that was high quality, axing the cheap items that were diluting their brand. Instead of charging the most they could for this quality, they kept prices affordable so more people would shop there and consider UNIQLO a “staple” of their wardrobe. In 2004, this shift to high-quality clothing was explicit. Below are two slides from 2004 that show their shift in strategy. Notice how UNIQLO wants to move up on the quality scale commensurate with their price moves, showing how the quality improvement was more about changing their brand positioning and consumer value prop rather than increasing pricing (or margin).

To keep in line with their market position, they would selectively retain dual lines of products with different materials for those that are more value-oriented vs quality-concerned. For instance, you can buy a Dry Crew Short-Sleeve T-shirt for $9.90 or dish out for the nicer Supima Cotton T-Shirt for $19.90. In both cases though quality is higher than more alternatives at that price point.

Alongside quality and affordability, they aim to create clothing that is “Made for All” and serve functional needs. Their HeattechTM and AirismTM fabrics are their inventions to cater to body temperature needs and their “Made for All” ethos means their clothing is designed with a variety of different people in mind versus other brands that may only focus on athletes for instance. “LifeWear” is another one of their mottos, and it embodies the fact that most of their clothing is very versatile, basic casual wear that can be dressed up or left as is. Most of their clothing is solid colored or patterned, but there are limited designs (with the exception of their more recent graphic T’s), and you will almost never see the UNIQLO logo. We will refer to this style of relatively plain and accessible clothing non-derogatorily as “low-fashion” (in contrast to high-fashion which is used to describe exclusive and trendy dress). In short, UNIQLO mostly focuses on “low-fashion” basic casual wear and wardrobe staples for everyone.

Their stores are designed to feel open with a lot of stock visibly out, which not only helps portray the illusion of excess choice, but also encourages consumers to help themselves which leaves employees to do other stuff like folding (not a joke, their multi-step folding process requires a lot of training to master and their sheer amount of inventory means it is often an employee’s most time-consuming task). When you finish shopping and check out, an employee will use both hands to accept your credit card, a sign of respect in Japan. The ease of grabbing clothing with limited need for much browsing seems to speak to men, since it is one of the rare unisex brands that tilts more heavily towards males than females.

Despite UNIQLO’s focus on basic fashion pieces, they would still have a lot of “hit” products. Fleeces mentioned in the intro were one, and their “Ultra-Light Down” jacket shown below is another. Unlike other fashion retailers whose hits tend to be short-lived, this jacket was first introduced in 2009 and continues to be a top seller. Whereas other fashion companies work hard for a design that gains seasonal success, the UNIQLO approach allows them to reap the rewards of a successful product for many years.

The Ultra-Light Down jacket is a good example of the UNIQLO formula. They started by innovating around the form of a down jacket, which they thought looked too bulky and unfashionable. Their aim was to create a jacket that was as warm as a traditional down jacket but was also light and compact. In order to do that, they produced a new methodology (in partnership with Japanese manufacturer Torray Industries) that allowed them to eliminate a step in the manufacturing process. Whereas conventional down jackets put the down in a “down pack” to prevent the material from escaping, they were able to design a process that applies pressure and heat to the shell of the jacket to eliminate the need of a pack.

After introducing a new manufacturing process and utilizing it to design a basic jacket, they employed their scale to order millions of them. Such a large order allows them to reap the benefits of economies of scale, reducing their ultimate cost per jacket and allowing them to sell them for an affordable price to the end consumer. This jacket launched at just ¥5,990, which is materially cheaper than what an equivalent quality jacket might cost (available for $70 in the US currently). UNIQLO stands alone in the size of the orders they place, which are in the millions versus peers who place smaller orders since they change their SKUs so often and carry a much larger selection. In a single year, UNIQLO has <2,000 SKUs, while Zara has ~6,000 and H&M >17,000. This focus on enduring styles also means that the risk of inventory obsolesce is lower, resulting in less discounting behavior versus peers. Given the low retail margins to begin with, any discounting is detrimental to profitability. To summarize, the UNIQLO formula in theory is as follows: smaller selection and a focus on universal, relatively generic clothing allows massive orders to be placed, which decreases their cost per unit of quality, making them the best value retailer around. The high quality for price drives high demand and the “timeless” nature of the design limits the need to discount, which protects margins. High sales allow even larger orders to be placed, further bringing down the cost per product and distancing UNIQLO from peers even more so. This strategy carried out earnestly is sound, while increasing their moat as a retailer overtime. However, as we will discuss shortly, the reality is more mixed than our synopsis of their formula.

The issue with retail generally is that it is extremely difficult to keep the perfect amount of inventory in stock to match demand: order too little and you lose an opportunity to sell and order too much and you’re stuck with product that no one may want. A lot of fashion products only sell well in certain seasons (think jackets in cold weather), and there are also larger fashion trends that can make certain styles obsolescent. When there is extra inventory at the end of a season, there is the impetus to clear out the old stock in order to make room for seasonally appropriate and fashion-current clothing. Not clearing out old styles quickly and leaving scattered amounts of last season’s items gives customers a poor perception of the store and they will rank it lower mentally next time they need something.

This creates two issues though:

1) Given retailers have low margins (~10-20% operating margin), discounting items can not only wipe out all of their profit, but make each sale loss-making. In fact, retailers budget for estimated discounts with a contra revenue account and net it against gross sales, but these estimates can be wildly off, especially if weather patterns show different seasonality than historically, or their products don’t resonate with consumers. This can whip-saw a retailer’s profitability, particularly if their value prop is fashion trend sensitive, in which case an entire collection could become obsolete if there is a miscalculation. And miscalculations are hard to avoid as most apparel orders will be placed 4-12 months prior to arriving in stores, requiring the purchasing manager and designers to perfectly estimate demand and style to avoid markdowns—a herculean task when done just a few weeks in advance, a total crapshoot when done a year prior.

2) Getting rid of inventory leads to a second issue—it dilutes brand image and can inadvertently train bad consumer behavior by rewarding the customer for delaying purchases and telling them that they do not need to pay full price. This isn’t a trivial issue–Hermès will literally destroy inventory rather than discount it and entire outlet mall complexes sprouted up precisely so their discounting behavior wasn’t associated with their full priced retail channels. Like everything in retail though, there is a balance to discounting. Sometimes a brand wants the sale to happen in their stores to drive traffic and in hopes the customer will buy other items while browsing. If the brand runs sales too often a consumer will wait for a discount to purchase or come to believe that the clothing is of lower quality than otherwise. The desire to get rid of obsolete inventory quickly, while driving traffic to the brand’s stores leads many retailers to run large sale promotions. However, in the long run, this can be detrimental for many brands. The best brands will either almost never put their products on sale or will go to lengths to disassociate the discounted products from their typical retail channels and inconvenience the consumer to get the sale. Outlet malls are far from the brand’s traditional stores since they don’t want consumers thinking of the two synonymously. They are literally imposing distance between the two to mentally separate them in the minds of the consumer (said another way, creating a hassle helps the brand enforce healthy price discrimination and avoid unnecessary discounting).

Lastly, even if you did all of this perfectly, if your competitor didn’t, they can flood the market with uneconomically cheap clothing that steals your sales (provided they are substitutable). This is all to say that retailing is a tough industry, and any level of sustainable success must be celebrated.

If we think about UNIQLO’s strategy in theory, we can see how it allows them to avoid some of the worst aspects of the industry, but doesn’t totally insulate them.

-

- Low-fashion, basic clothing style. This means they are not as susceptible to the whims of the fashion industry as their products have more longevity which should lead to less discounting. For the same reason, this gives them comfort in placing larger orders. While all clothing may go in and out of favor over a long period of time, the relevant period for UNIQLO would be from when they place the order to when they sell it in stores. In which case it seems pretty unlikely there is a dramatic shift in the demand for plain colored t-shirts, quality but innocuous down jackets, or jeans from year to year (but it can happen).

- Scale Economies Shared. The larger orders they place allows for greater economies of scale and thus a lower cost. This strategy is enabled by the basic clothing style as they would need to have confidence that the attire wasn’t a miss in order to place such large orders, which also require more time. UNIQLO takes about a year from planning to get the clothing in the store, which is the longest versus peers. The scale allows them to provide higher quality clothing at a lower cost versus others. Instead of holding prices high and increasing their profitability, they try to keep prices affordable for their consumers and rebate cost savings back in the form of lower prices.

- Limited promotion. Many lifestyle brands have to spend prolifically in order to build their brand and get customers interested in their products (especially if they are at high price points). UNIQLO’s approach of charging affordable prices for high quality items means that customers don’t need to be convinced much to buy from them– UNIQLO just needs to get them into the store. Rather than run promos to get customers in (training bad behavior) they rely on making huge global flagship stores that are intriguing enough that passersby check it out. Once you buy from UNIQLO and understand their positioning, there is a good chance that when you need more quality staples, you will return. The benefit to UNIQLO is limited advertising and promotional expenses, which frees up more money to build out their store footprint while still keeping some margin (advertising expense runs about ~half of what some peers are at).

However, as we alluded to earlier, this is an idealistic formulation of the UNIQLO strategy. In actuality, UNIQLO is not immune to the same issues prevalent for everyone else in the retailing industry—from mis-forecasting weather seasons to fashion misses and relying on sales to clear inventories and drive traffic. Despite UNIQLO’s best efforts and sound strategy, they cannot escape the fact that consumers are fickle and being an unbranded apparel retailer focused on “low-fashion” clothing is putting them in the position of competing mostly as the lowest cost (per unit of quality) operator. While UNIQLO has built out their competence and has advantages here with their scale, it is an area of the Consumer Hierarchy of Preferences that is relatively easy to compete against if one wished to.

UNIQLO’s strongest competitive weapon is their reputation for quality and affordability, whereby consumers first visit UNIQLO for these basic items, not giving a competitor a chance to fight for the sale. Once a consumer comes to rely on UNIQLO for these staple items, they may value the ease of finding what they want all in a single UNIQLO store, knowing that they won’t be dissatisfied with the purchase. For people who don’t tend to like shopping, this is a very valuable (and quite likely why they over-index to males), but it is a competitive position that is replicable by a competitor in a way that Nike-branded Jordan shoes are not. Thus, UNIQLO wins by weaponizing their operational efficiency to reduce price per unit of quality offered in hopes that supports increasing demand. However, the problem is that incremental quality is somewhat subjective and marginal reductions in price may not yield incremental sales. This means that the flywheel may not be as self-reinforcing as we initially laid out.

Another issue is their focus on low-fashion and high-quality clothing could actually hurt them in two ways: 1) having clothing that is always available eliminates the urgency to purchase it, so unlike Zara where customers buy things for fear they will never find them again, a UNIQLO customer can virtually be assured that the Ultra-Light Down Jacket they are eying will be available next year too. 2) Higher quality also means garment longevity, which when coupled with clothing that is low-fashion and designed to be a “staple” of the wardrobe, means that once a customer gets their fill, they have no reason to repurchase until their clothing wears-out. But thanks to their focus on quality, their clothing lasts for many years—many shoppers we spoke with noted that they owned UNIQLO clothing that was at least 5 years old with no visual signs of wear. In short, they could be too good at their job, which translates to consumers not needing more low-fashion “staples” and UNIQLO needing to produce something else to draw them in (this is an issue with durable goods in general).

We believe this has pushed UNIQLO into more fashion-collaboration and limited-productions like their graphic T-shirts. Whereas a loyal UNIQLO customer might have all of the “staples” they need, limiting the need to revisit, limited run productions give new reasons to return. They will often also introduce slightly new materials, colors, or cuts of their existing styles to keep the line fresh. However, the net of all of this means that they get back on the “fashion-treadmill” to some extent, especially as a larger portion of their customers already own “staples” and return just for the new items.

The outcome of all of this is a product offering of low-fashion basics like solid-colored t-shirts, sweaters, sweatshirts, pants, underwear, and slightly more fashionable items like jackets, dresses and button-down shirts coupled with limited-run items. This translates to shoppers (per our consumer interviews) that like UNIQLO, but don’t go there as often as Zara or H&M and consider those to be “younger” and lower quality than UNIQLO. The consumers we spoke with said they tend to buy more “practical” items from UNIQLO and say it is a less “exciting” experience. Anecdotally, they felt that it seemed UNIQLO had sales more often than Zara or H&M. They consider UNIQLO “innovative in a practical way” with new materials, but they spend more elsewhere.

Hopefully, you have a good sense of UNIQLO by now, and we will now move into judging their operations in Japan , where there are the most disclosures.

UNIQLO Japan.

In our UNIQLO Japan analysis we looked back over the past 15 years to try to build a sense of how the unit economics of their stores worked out, as well as how well that operation has been run since that is their only “mature” operation we have disclosures on.

At the end of 2021, UNIQLO had 810 stores in Japan (including 30 franchised), up from 637 in 2004. However, while net store count has increased by 137, total stores opened has incredibly increased 884! This is because they have been aggressively refreshing their stores and reconfiguring their store network with many years of 30-40 stores closed annually. With these new stores they wanted to increase the average size of the store, believing that larger stores would help convey higher quality products and draw more consumers in. Bigger stores would also allow them to display more of their clothes and provide more room for inventory.

With dozens of store closures and openings every year, we wanted to check if we could prove that these were indeed strategic closures and launches. In order to triangulate this, we calculated two figures. The first calculation is a simple sales per store calculation which uses all stores reported at the end of each period (this is the grey line below). The second calculation is a modified sales per store calculation which takes the prior year’s sales and grows them at their reported SSS growth rate and then divides by prior year’s store count (plotted as the orange line below). This should give us an approximation of what Sales per Store would be if they didn’t open or close any stores.

If UNIQLO is indeed strategically improving their store footprint, we would expect that the total sales per store at the new footprint would be higher than the prior year’s footprint grown at the SSS rate, which is exactly what the below chart shows. The difference between the two lines is plotted as the red bar which shows that on a per unit basis the new store base is regularly outperforming the old store base. This is impressive in light of the fact that many of these stores may have not been opened for a full year and many retailers need to ramp up a store for a period before they reach their full potential. For UNIQLO though, in the first-year, new stores can outperform their old base.

One pushback to this analysis is that new stores are bigger, so you would expect them to generate more on a per unit basis than the prior footprint. And while that is true, it is also true that sales per square meter having been trending up.

Above we see that sales per square meter increased from 2006 to their pre-pandemic peak in 2019 at a 1.9% CAGR. While this may not seem impressive at first glance, making each square meter work more every year is extremely difficult, especially since they didn’t take price. This is even more impressive when taking into consideration their total footprint grew 73% over the same time period, or at a 4.3% CAGR.

From 2006 to 2021, Japan sales grew at ~6% compounded, but we wanted to see how much of that growth we can attribute to their footprint growing versus their stores becoming more “efficient”, which we defined as increasing sales per square meter. Below you can see the output of that analysis; on average over the past 15 years 80% (or 4 points of total growth annually) can be attributed to them growing their footprint, whereas 20% (or 1 point of total growth annually) can be attributed to them growing sales per square meter.

Take note of how the growth composition changes over time with the red (growth from square meters increasing) becoming an increasingly smaller portion of growth. This impact starts around 2015 (and is slightly reversed after stores reopen post covid). What this is suggestive of is footprint saturation since increasing their national footprint is no longer reliably leading to greater sales at it did for many years before. This is partly owing to ecommerce as a portion of total sales increasing, which would support sales per square meter increasing, but ecommerce was only ~4% in 2015, growing about ~1 point in 2016 versus growth from square meter increases in the high single digit range for the years before. Below we show total UNIQLO Japan sales growth, and we see that the period after 2015 sees a markedly lower growth cadence of ~3% (prior to pandemic) versus an average of 8% in the period from 2006-2015.

Their sales totaled ~$6.9bn for 2021 which comes out to ~$8.5mn per store, which includes attribution for their ecommerce operation under the thinking that the store network supports and creates online demand. (If you want to back out ecommerce sales, it would be roughly ~20% lower). Each store produces about $1.25mn in EBIT, which yields margins slightly under 15%. Their margins have been incredibly inconsistent and have generally been trending down over the past decade for reasons that aren’t entirely clear to us. Importantly, these are not consolidated margins that include other loss-making brands or newly launched geographic markets which we know to be in their under-earning phase—Japan is their most mature market. Their operating margins peaked over a decade ago and they haven’t hit their 2010 operating income level in $ terms again either.

It isn’t obvious what the largest contributor to this deterioration of performance was, but we think it has to do with the weakening Japanese Yen and new store builds (investor relations has a policy of not responding to inquiries outside of their Q&A and events). In 2010, the Yen hit it’s all time high against the US Dollar (as a proxy for strength) at ~80 Yen to 1 USD, but has since weakened over the subsequent decade, trading in between 100-120 Yen per 1 USD. The weaker Yen would increase their costs denominated in other international currencies (most of their production is in various Asian countries and not in Japan), although admittedly the years they disclosed their Japanese gross margin do not show a huge impact (2010-2014 gross margins are as follows: 49%, 49%, 48%, 47%, 50%). In their annual reports they call out excess discounting and seasonality that was different from what they expected as the cause for margin compression, but the latter seems to be mentioned almost every year and neither would explain a prolonged contraction in margin unless we assume discounting significantly increased over the past decade. Our other hypothesis is that the aggressive scrap and rebuild store plan, which increased the average size of their stores led to increased costs (our accretion analysis above could only be applied to sales). However, we don’t see a meaningful increase in rent, D&A, or personnel as a % of sales on a consolidated basis and this was at a time when UNIQLO Japan was the vast majority of the business. Whatever the reasons may be, it doesn’t look like we should expect to see margins recover to their prior >20% high without meaningful cost rationalization.

Some cost improvements could come from their Ariake Project, which was launched in 2016. This is what they refer to the digitization of UNIQLO to become a “digital consumer retail company”. They opened up a fully automated warehouse in Ariake Tokyo with a 16,500m2 open-floor plan corporate office above. This was done in order to flatten the organizational hierarchy and lower division separations so there could be greater cooperation. Communicating closely can directly impact margins through better demand forecasting and production planning, which paired with live data from their stores and customer feedback can help by better matching inventory to real demand. This reduces or eliminates excess inventory at the end of each season, which means less discounting—the most critical factor to margins.

The other factor of this is enabling omnichannel and keeping direct communication with the customer through digital marketing. Ecommerce is clearly an important channel and UNIQLO is working to mesh the channels—today 40% of online purchases are picked up in store. This ability to leverage their store footprint, while still giving consumers the convenience and selection that online offers is an advantage versus up-and-coming pure online retailers like Shein.

Competition.

Shein, recently valued privately at $100bn, is essentially a digitized version of Zara. They iterated on the fast fashion model by taking the M2C (manufacturer to consumer) trend that Pinduoduo helped popularize and apply it exclusively to fashion. As there are a ton of clothing manufacturers in China that have the capability to pump out all sorts of variations of garments at cheap prices, the question is “what do you produce?”. To answer that question, Shein will create designs and only produce small batches of them before putting them on their app/website. Consumers browse the thousands of styles that are constantly refreshed and if an item proves to be particularly popular, they can increase the production of it or quickly roll out similar styles or more colors. Since the feedback from the consumer is immediate as they do not actually have to wait until the goods are shipped to a customer to get a sense if something is working or not, they are an even faster version of fast fashion. They also gamify the experience and have been an aggressive marketer on Tiktok, but a lot of publicity came organically with many users posting their “Shein drops” on Tiktok that include the dozens of garments they bought for extremely cheap prices. Interestingly, Shein does not sell in China since there is already a ton of cheap clothing there, but instead focuses on international markets like the United States where extraordinarily cheap clothing that is constantly changing is very popular with the youth and because of the purchasing power parity, they can afford it too with $10 blouses, $18 sweatshirts, and $28 skinny jeans.

However, this isn’t a direct competitor to UNIQLO because in Tadashi’s words: “We don’t chase trends. People mistakenly say that UNIQLO is a fast-fashion brand. We’re not. We are about clothing that’s made for everyone”. UNIQLO’s value prop is not only not “fast fashion”, but it also isn’t cheap either. The most common complaint you’ll see from buyers on Shein is the quality is very cheap. However, for their consumers, quality isn’t valued as much as being able to rapidly change their wardrobe for little money. For a similar reason, Zara and H&M aren’t direct competitors either as they focus on getting the latest fashion trend right versus UNIQLO who focuses its design principles on what it thinks will be “timeless”. Funny enough, despite Tadashi insisting they aren’t fast fashion, they invite that comparison by constantly ranking themselves against Zara and H&M in investor presentations. Nevertheless, despite them not being direct competition, in reality every clothing company that can sell to UNIQLO’s consumers is a competitor.

There isn’t a point in pretending that UNIQLO’s value prop is so unique that it shrinks the pool of competitors because no clothing retailer has such a strong competitive position that they are insulated from competition. There is nothing in clothing that is protectable other than manufacturing processing technology, patented materials, or a brand. The last of which is the only one that seems to be enduring as other players can create similar feeling materials and most manufacturers aren’t owned by the brand/retailer anyway so they can share their technology with the competitors. Furthermore, many consumers often prefer wearing things that others don’t have and like to switch up their attire which means they are constantly on the hunt for something novel. While brands/retailers work to acquire customers, customers are working to acquire different brands. UNIQLO’s position as low-fashion means a lot of their product lines aren’t susceptible to this behavior (we spoke with consumers who just get all of their plain t-shirts or workout clothes from them for example), but this portion of retail is inherently limited in reoccurring sale opportunities since there is a limit to how many “staples” you need. As mentioned prior, this means that in order to get an incremental sale from an existing customer, they would have to introduce something new which then puts them in the same competition pool as many others. Competition can come not just from established retailers, but also a ton of new upstarts with Shopify stores and Instagram ads. Historically, getting in front of the consumer was a tougher thing to do with TV commercial costs, full-page newspaper ads, or sponsorships being prohibitively expensive for most, but now it is easier than ever before to get in-front of a consumer. With low barriers to entry getting even lower, no switching costs, infrequent purchases that are all one-off, capricious changes in consumer tastes, and clothing being a durable good allowing purchase delays and creating cyclicality, the retailing industry is incredibly tough. Layer in complex material sourcing with global manufacturers historically needing to be policed for labor rights abuses, dealing in multiple currencies, coordinating logistics worldwide, in a business where demand needs to be accurately forecasted far in advanced, it’s a wonder anyone consistently makes money at all.

However, despite all this, UNIQLO has carved itself out a niche in the fashion industry and has a multi-decade history of being profitable. Nevertheless, it is not a very protected business and the consumer surplus they have built over the years by providing many shoppers with clothing they appreciate at affordable prices is always at risk of being superseded by another player. That said, their value prop, style, quality, and price point resonate with many consumers, and it would be hard to replicate it as efficiently as they do it. When we think about what UNIQLO will look like in the future for our revenue build, we assume their Japan operations stay more or less the same. However, as we cover next, their international operations are much trickier to size up.

UNIQLO International.

UNIQLO’s international operations are a very different animal than their domestic chain of stores. Unlike in Japan, when UNIQLO was rolled out internationally it received very mixed reception in Europe and North America. However, their Asian operations, particularly in China, have been very strong. In this section we will dissect their international efforts more to get a better sense of the growth opportunity and how well UNIQLO transports overseas.

As mentioned in the intro, they started their international operations in London and Shanghai. Their efforts in the UK were not received well and they had to shutter most of their footprint and reset with larger global stores to introduce the brand. After a while, UNIQLO gained limited traction in Europe, but still is far off of the penetration they have in Japan. Their positioning in Europe is similar to Japan, but Europeans have far more options and their tastes tend to skew higher-end with it being more common to judge someone based on their clothing. The idea of “Made for All” doesn’t fit as well in cultures that historically had strict dress hierarchies, of which consumers still have lingering derision towards low-priced, mass-produced clothes (it isn’t a coincidence that virtually all of the most popular ultra-high end clothing brands are European). Nevertheless, they are growing in popularity in Europe and have the runway to grow further, but have not moved outside of mega European cities yet and only 64 stores.

Their US operation launch was more akin to their European experience than China’s (as we will go over momentarily). When they rolled out in New Jersey in 2006 they had clothing that was mis-sized for the market, as Americans tend to be taller and bigger than the Japanese. Additionally, their minimalist style that was popular in Asia reminded shoppers of The Gap and other similar retailers, rather than a unique concept. The retail industry is also more developed in the US than anywhere else globally with the consumer having a plethora of options, so UNIQLO with their limited advertising didn’t stand out. Over time, they would reboot the concept, scrapping existing stores and opening larger global ones, particularly in NYC, that drew large foot traffic with their very conspicuous flagship stores. In time, they would continue to expand their footprint, launching on the West Coast too. However, despite over 15 years of operations in the US, they only have 57 North American stores (this includes the 14 stores in Canada). Ecommerce has been a bit of a saving grace for them, now representing 40% of North American sales, higher than their global average of 30% and China and Japan which are at 20% and 15%, respectively. UNIQLO considers North America one of their bigger growth opportunities remaining, but it has been hard for them to meaningfully penetrate it.

China was a very different story than Europe or the US, finding almost instant success, and they very quickly ramped up their store footprint, opening close to 100 stores annually at one point. At 932 stores in China, their footprint is larger than in Japan, and given that China has ~11x the population, there is clearly the scope to keep growing. They have come closest to meeting their ambitious targets in China more so than in any other international operation (in April 2019 they guided to 1,000 stores by August 2021, when they were at 673). Part of their success is owed to the fact that China is home to a ton of low-quality, but incredibly cheap clothing. When UNIQLO offered their same quality clothing they do elsewhere, given the gap in quality differential it seemed even higher end than it does elsewhere. The value for quality was a new consumer value prop and the Chinese consumers enthusiastically adopted the UNIQLO brand, making it one of Chinese most popular apparel brands (Chinese publication YiMagazine ranked them as a Top Brand for 10 consecutive years).

The brand and retail concept ported well to other Asian countries as well. UNIQLO has proved popular, particularly in Korea (134 stores), Philippines (63), Thailand (54), and Malaysia (48), but their presence in other Southeast Asian countries is still growing. In total, their international operation now generates ~$7.8bn, surpassing UNIQLO Japan which brought in $7bn in 2021. However, while international operations generate just 11% higher revenues, they have 80% more stores (810 in Japan vs 1,457 Internationally ex-Russia). This shows how relative to their domestic operations, their stores earn much less at ~$5.2mn internationally vs $8.7mn domestically, almost 40% less. Purchasing power parity may explain a good portion of this difference, but nevertheless it is still less valuable growth to Fast Retailing.

As you can see above, their International segment’s growth is pretty lumpy. From 2014-2021 they grew at a 12% CAGR, putting UNIQLO International at 44% of total revenues for 2021 (UNIQLO Japan is 40%). In fiscal 2021, their China operation alone generated about ~$4.4bn or 57% of their international revenues, making it by far their most important foreign market. Their sales per store in China are $4.8mn, lower than Japan ($8.7mn) and International ex-China ($5.8mn). However, their operating margins in China are very strong at 18.8% versus the consolidated international operations at 12%. So while they earn in absolute dollars 45% less in China than Japan per store, their profitability is better.

As seen below, their margins are also pretty volatile. In addition to all the vagaries of the retail business, there also are new market launches and store opens that conceal their true margin. They have previously guided their retail operations to 15% with the possibility of reaching 20% long term.

Interestingly, if we back out China EBIT from their international segment, we see that all other markets look like they are under performing with $93mn of EBIT on $3.3bn in sales. It is true that a few markets could be incurring a large loss that is bringing down the average, but still, this is suggestive of sub-par performance at most of their international operations. In our revenue build below, we will show what their earnings would look like if they improved this to 10%, but in long term there is upside if they can improve it to the same level as their other operations. Frankly though, when a retail operation isn’t working it is very hard to tell why that is from just the financial statements. We couldn’t tell you if it was because of excess discounting, slower turnover, weaker demand, higher costs to operate, or something else. So absent of a clear reason of what the issue is, it is hard to be confident in how it will improve. This is to say, a more conservative investor would want to discount the operations that are not working, rather than assume they will improve.

In order to help spur more demand internationally, build brand recognition, and better differentiate themselves, UNIQLO has embarked on a variety of art collaborations and licensing deals. While we already mentioned the graphic t-shirts, many of which have well-known paintings printed on them, they go a step further by partnering with museums directly. When launching their Rivoli store in Paris, they partnered with the Louvre Museum, sponsoring mini-tours and rolling out a special collaboration of works with Louvre pieces featured.

They also did something similar in New York with MoMA (The Museum of Modern Art), sponsoring free Friday nights and rolling out a MoMA collection. These initiatives essentially act as brand advertising and help build consumer awareness, while (usually subliminally) building a positive affect for the brand.

These efforts though are also suggestive of how their same playbook in Japan couldn’t be imported wholesale to their international markets and they had to get creative, trying new things to improve their international reception. With the impact of Covid, it is hard to see exactly how well they have been fairing, but we know for instance that their United States operations have been very problematic with Tadashi saying they have moved from the US being in crisis mode to being just a big underperformer (you have to appreciate management’s honesty). The push to ecommerce has helped a bit, but it is still ultimately too early to tell whether they will succeed in a meaningful way in the US and Europe. However, we are more positive on their progress in other Asian countries.

Other Brands.

Fast Retailing has several other brands, most of which they acquired. GU, their most successful of which, is actually now broken out separately. Last year GU contributed 12% of total revenues and 8% of EBIT. Their other 6 brands are still grouped together under “Global Brands” and contribute just 5% of total revenues and together net out to a tiny loss (-60bps margin). We will spend a bit of time going over each, but we do not see these brands as being the core driver of Fast Retailing.

GU. Pronounced Jiyuu (G-U), which means Freedom in Japanese, was launched in 2006. Originally positioned as a cheaper UNIQLO, it was not well received. They tinkered with the format and created clothing more in line with current trends, with monthly installments of new clothes, essentially happening on the fast fashion model. They claim to be a little more original than Zara that often copies popular designs and couples it with a “Japanese sensibility”, while tending to target the youth with a tilt towards women. We don’t see them as meaningfully different than other fast fashion brands though. UNIQLO focuses on basics, while GU chases trends (and attempts to create them). They leverage UNIQLO’s manufacturing capabilities and often keep stores within a close vicinity of one another to improve distribution synergies.

To keep prices low, GU puts clothing on hangers to avoid needing the timely folding that UNIQLO employees incur and allows them to have fewer staff in each store. GU only has a meaningful presence in Japan today, which is where virtually all of their 439 stores at 2021 year end are located. They opened 3 stores in South Korea only to later close them, largely driven by boycotts that fomented from the prior occupation of South Korea by the Japanese empire during WWII (a commercial where a young girl asked an elderly women what she wore when she was younger was translated to “who can remember something that happened 80 years ago”, a time frame that coincided with the occupation, initially stoked the protest—UNIQLO wasn’t immune from it either). Outside of South Korea, they have a handful of stores in mainland China and Taipei, but they still haven’t ramped up their store network there like they have with UNIQLO.

GU’s financials were broken out in 2018, and they have grown at a 6% revenue CAGR since. They grew 13% in 2019, but have since averaged ~2% post-pandemic. Store closures have no doubt weighed on their operations, and higher costs also hit their margins with EBIT margins of 8% versus ~12% in 2019. With operating earnings of $168mn in 2021 versus UNIQLO’s ~$2bn, they have would have to materially increase their footprint in order to have a more material contribution to fast retailing’s bottom line. However, the fast fashion concept is very tough and has even more direct competitors than UNIQLO, which still found themselves with limited adoption outside of China and select South East Asian countries. While this concept has done very well in Japan, we are still hesitant to assume any material international growth in our build.

Theory. Theory is a brand you may have heard of as a large portion of their >400 stores are based in the US. They are a luxury brand that was 89% acquired by Link Holdings in 2003 for $100mn, and Fast Retailing took a ~33% stake in Link Holdings shortly thereafter. In 2009, Fast Retailing acquired the remaining stake and now it is a fully owned subsidiary. Link Holdings’ other brands include Helmut Lang, PLST, and footwear label Jean-Michel Cazabat. Theory is a unisex brand that positions itself as higher-end, with their men’s T-shirts starting at $75 (versus UNIQLO at $10). We don’t have detailed financial information to dive into, but we will say it seems that Theory has generally been received well and had some success slowly growing their operations. However, despite ~15 years of ownership, they still aren’t at the level of materiality that Fast Retailing has reported their results as a separate financial segment.

Other Brands. Their other brands include Comptoir Des Cotonniers —a French brand that focuses on women’s casual wear internationally, Princesse tam.tam —a French lingerie and loungewear brand that is international, PLST—a chain of stores in Japan that focuses on “top quality comfortable clothing”. We haven’t spent much time diving into these given their relative size, but its worth noting that last year Comptoir Des Cotonniers footprint was drastically reduced from 260 in fiscal 2020 to 135 as of Feb. 2022. This was done to rationalize cost and close structurally unprofitable stores. Princesse tam.tam similarly underwent large store closures from 119 to 85 over the same time period. Both brands only opened a handful of stores over the same period. PLST fared better, only closing net 11 stores to 92 as of Feb 2022. In the quarter ending Nov. 2021, Fast Retailing actually moved the Global Brands segment into the black with a tiny ~$20mn EBIT profit on the back of stronger sales from Theory and lessening losses at the two French brands. Given that they have owned most of these assets for a tremendous amount of time and still haven’t meaningfully drawn a profit from them, we remain reticent to attribute much value to this segment.

In fact, we think rather poorly of their capital allocation in regards to M&A. In 2012 for instance, they bought an 80% stake in a jeans brand called “J Brand” for $290mn. They used to sell the brand through various department stores (store in stores), stand alone stores, and online, however they have shuttered all operations as shown below.

We cannot judge their other acquisitions so cleanly, and you can make the argument that it isn’t a very meaningful amount of capital they used for acquisitions so has a relatively minimal financial impact, but it can still be costly in terms of focus and human capital. It is also true though that all of this M&A was done a while ago and they seem more focused on UNIQLO and GU than the other brands. This would be a positive because there are very limited synergies between owning multiple brands beyond perhaps maybe some supply chain knowledge, although the very different products limit this. Needless to say, we do not assume anything herculean comes from their Global Brands in our build.

Revenue Build.

To get a sense of Fast Retailing’s valuation, we will estimate how much we think they can grow earnings under our “base” case and under an “upside” scenario. The band between the two is what we highlight in our valuation sensitivity. Of course, as with all estimates, you should think of our outputs as existing on a probability distribution with the numbers explicitly shown likely to be wrong. However, it is still helpful to get a gauge of valuation.

Before we dive into the numbers, we want to note that Fast Retailing tends to be very ambitious in their long term guidance. In 2014 they put out a ¥5tn revenue target with 20% operating margins. That implies a 23% CAGR and a ~doubling of their consolidated operating margins from 9.3% in 2014.

Just 2 years later, in 2016 they reduced that by 40% to ¥3tn yen and operating margins of 15% with an ambiguous allusion that they will eventually hit their prior 2020 targets.

Despite the lowered targets, in 2021 they only generated ¥2.1bn in revenue with 12% operating margins. While we like that their outlook was set without particular concern for managing expectations, it seemed unrealistically optimistic. While we like Fast Retailing’s ambitious attitude and most of their rhetoric around constantly improving and not letting success make them arrogant, we will focus more on their recent history when extrapolating out the future. Since 2014, they grew revenues at a 6% CAGR, or just 4% over the last 5 years. It’s true that the pandemic, with store closures, was a headwind, but other companies were able to make that their opportunity, leaning into more online and direct to consumer sales, which actually improved profitability. Instead, we see Fast Retailing is still below their 2019 fiscal year in 2021 by about ~6% (their last quarters results were only +1% y/y improved) with EBIT margins that were 50bps higher.

In our build below, we give our base estimates of ~$22bn in revenues and ~$2.8bn in EBIT at a 13% operating margin. In the upside scenario, revenues are ~$3bn higher with margins that are 400bps better, driving EBIT that is 50%+ higher. (As always our Members Plus can download the excel exhibit and input their own estimates).

We then feed these figures into our sensitivity analysis to help set the bands of what to vary around. In the exhibit below, we sensitize around both revenues and EBIT margin. We apply a 35% tax rate that is rather high for a global average, but in line with what they have incurred recently. Then we apply a 25x multiple, which we frankly think is somewhat generous given the durability of their business model with no naturally reoccurring revenues and slowing growth. Today they are priced at a 40x multiple, but that drops to a ~32x earnings multiple after backing out their almost ~$10bn in cash.

At a 25x multiple and assuming they generate ~$10bn of cumulative free cash flow over the next 5 years, we see a 5-12% annual total stock return (TSR) after including their current ~0.9% dividend yield. This multiple would likely only be warranted if they have a clear scope to increase earnings high single digits to low double digits for several years thereafter. At 20x, which would be appropriate if they are only growing mid to low single digits, the TSR drops to 2-8% annually. Given the difficulty of running a retailer without issues and the likelihood that a new competitor weighs on your sales is quite high over a long period of time, we would be biased towards insisting on a larger margin of safety. However, it is your prerogative as the investor to decide what is the appropriate return for the risk you see in Fast Retailing and relative to your alternative investment opportunities. Our opinions of their competitive positioning may differ from yours.

Clearly, with ~$10bn of cash currently and the expectation for them to double that over the next ~5 years, they have ample room to either increase their dividend, initiate stock buybacks, or do a large acquisition. The last of which we frankly would view as a source of risk, and they haven’t done a stock buyback since 1998. Their capital allocation will ultimately be a large variable in their warranted multiple.

Risks.

-

- Less Demand. Consumers in fashion are fickle and they could shop elsewhere for many different reasons.