*Please see our disclaimers at the bottom of the page and our full disclaimer here. By using our website, you acknowledge you have read our disclaimers and agree to our terms of use.

**Thank you to all of our subscribers for supporting DJY Research! We hope you enjoy our JD Deep Dive! Just incase you are curious, the founder of JD’s name, Liu Qiangdong, is pronounced (lee-oh chee-ong-dong). Despite this being a rather long report, JD is such a large company that there is still plenty more to talk about! Feel free to reach out and ask us questions in our Discord if there is something you want to learn more about!

Founding History.

Liu Qiangdong was born in 1974 in a rural village to an enterprising family that used to transport goods along the Yangzi River before they were forcibly relocated and lost everything in the 1949 Cultural Revolution. Their village had neither water nor electricity nor roads, and they only ate meat twice a year. His dad was an accountant in the “production brigade”, tabulating farm produce, but in 1979 a local government program allowed limited borrowing and they purchased a freight boat to resume their family trade of transporting goods. While this brought in some more income compared to the other rural peasants, it also meant that his parents were often out working, leaving Liu to be raised by his grandmother. Despite their improved income, Liu speaks of eating nothing but permutations of potatoes for half of the year and corn for the other half. In 1992, Liu was one of the top scorers of the Gaokao in the Jiangsu Province, which gained him acceptance into Beijing’s Renmin University. However, his parents were too poor to spare the RMB 500 required to send him there, leading to the entire town pitching in to help him. With RMB 500 and 76 eggs, he was off to Beijing.

Liu, who adopted the English name Richard, majored in sociology. However, his real education came in the form of self-taught programming. As one of the few people capable of coding right at the birth of the internet, his part-time moonlighting earned him substantial wages, and he bought his family a new home, along with a Motorola cell phone for himself, which cost a magnitude more than the Beijing travel fare he had to borrow just a few years ago. Feeling flush, when a popular restaurant he liked to frequent was receptive to selling itself, Richard kicked in all of his savings and borrowed the remaining RMB 200k required to buy it. Aware that he had no idea how to manage a restaurant, he thought the best method would to be as hands-off as possible. In turn, the staff colluded to steal from him, inflating purchase orders for kickbacks and misreporting receipts until he had to shut it down less than a year later. To pay off his debts and reset, he worked at a health products company called Japan Life for two years, and ultimately learned that his restaurant failure was the result of not having a management structure, clear procedures, or financial oversight, a lesson he made sure to never forget. After paying off his debts and with RMB 12k in his bank, he was ready to start his next business venture.

Background History.

On June 18th, 1998 (a date that today is best known for JD’s massive 618 sales), at just 24 years old, Richard rented a small 4sqm stall in Haikai Market in Beijing’s technology hub of Zhongguancun and started selling magneto-optical products (hard drives and CDs). He called it JingDong Multimedia, or JD Multimedia, by combining his name (Dong) with his then-girlfriend’s (Jing), who he awkwardly would not ultimately marry. Whereas most of his peers sold products that were often fake and haggled over for each yuan, Richard set JD Multimedia apart by putting price labels on everything and only selling authentic products with official receipts (a practice counterfeit sellers couldn’t mimic for fear of reprisal). Price labels allowed customers to know that they were getting the same deal as everyone else, and lowered their fears of being ripped off. While his prices weren’t the lowest a customer could find in the Haikai Market, the authenticity guarantee carried weight. Richard would often tell his customers, “If you are sure those other products are authentic, you should go ahead and buy those”. Not wanting to gamble, the customers would usually end up paying the slight premium for JD’s authentic products, especially since data storage devices were not products that they wanted or could risk failing on them. While it started as a one-man operation selling a limited array of magneto-optical products, within 5 years JD Multimedia grew to 12 stores that sold a wide assortment of electronic products and was earning RMB 10mn. His goals at the time were to have 200 stores selling IT products within a decade.

But this all changed in 2003, when the SARS epidemic hit China, and JD Multimedia had to close down all of their stores. An employee suggested they try selling their inventory online, and they began posting merchandise on various online forums. Showing how building consumer trust can repay itself in unintended ways, customers who were otherwise reluctant to transact online were comforted by seeing the seller was a known trustworthy retailer and unlikely to swindle them. Seeing some success with internet sales, they launched their own website in 2004, called JDlaser.com. When the SARS epidemic ameliorated, they ran their online store in parallel with their physical retail stores until Richard decided that the better inventory control, quicker price change responses, and wider distribution made the internet a better channel. In 2005, he made the decision to close all of their stores and focus entirely on the online opportunity, despite it meaning JD’s 2005 sales would be half of what they were the year prior. Innovator’s Dilemma evaded.

JD continued to focus on the 3C category (computers, communication, and consumer electronics) initially, which had the benefit of having a more limited SKU set with fewer relevant brands (relative to FMCG) and also higher ASPs that would allow the consumer to rationalize the shipping costs easier. In the early days, Richard would push his procurement team to get the best deals possible on products, even if it meant that they would have to put in large purchase orders. When the purchasing team wanted to buy 200 units of something, Richard would tell them to buy 10k so the cost would drop and they could spur more sales by lowering the price. In a telling example, a computer display that sold for RMB 649 and cost RMB 600 could be purchased at a greater scale for RMB 550 and sold for RMB 599, which gave customers a better deal while giving JD the same unit gross profit. The only way this model would work, though, was if they could grow sales velocity, so inventory costs were manageable. While ordering products in quantities above their current customers’ needs in hopes the lower price would stimulate new demand was a risky proposition–as they could be stuck with more inventory than they could sell, which would incur warehouse storage costs, tie up working capital, and risk inventory obsolescense–it worked time and time again, and became JD’s formula. In 2007, they changed the website name to 360buy.com, and the company renamed itself to JD Mall, foreshadowing a future desire to move beyond just electronics.

During these years, they faced cutthroat competition–not from Alibaba’s leading C2C site Taobao (whose reputation for being flooded with fake goods turned off many potential customers)–but from online retailers like the China-native Dangdang and US-based Newegg and Amazon, as well as offline retail chains like Suning and GOME. Employees would wade through competitors’ product listings around the clock, adjusting JD’s listings to always be in line or cheaper than their competitors’. Everyone knew that the strongest competitive position would ultimately come from being the most scaled player, since that would allow them to place the largest orders with suppliers, thus reducing their costs of goods sold, which in turn would allow them to increase demand by lowering their prices. So to build that scale, each retailer was willing to give up margin for the volume that would ensure longterm viability. In October of 2006, with RMB 60mn in revenue (growing 10% m/m with no advertising spend) and 50 employees, Richard looked to raise $2mn to further scale their operations as customer demand inflected. He met Capital Today’s Kathy Xu, who insisted he take $10mn, introduced him to other investors, and with whom he mutually agreed to only focus on growth for the next four years and not worry about making profits until the fifth year. Sales grew rapidly– JD increased revenues more than 3.5x to RMB 360mn in 2007.

Richard Liu (similar to Coupang founder Bom Kim), noticed that over half of all customer complaints related to shipping delays and damaged packages, so he started to set his sights on not just handling the warehousing and fulfillment of online deliveries, but also the last mile logistics capabilities (which was years before Amazon would start to do the same, as China had no reliable national logistics providers like FedEx or UPS in the US). In controlling the full logistics chain, JD hoped to ensure the best and quickest delivery experience, which would also allow them to accept COD (cash on delivery), which was still popular at the time (most 3rd party logistics providers wouldn’t provide this service–or if they did, they commonly stole the money or at best remitted payment back very slowly). This capability would be a differentiating factor vs. the competition who were admant that logistics was too capital intensive and would be too risky. They weren’t wrong–at the outset, Richard estimated that it would cost at least $1bn to build last mile capabilities and would require 2k orders/day in most cities to break even–when they were averaging around just 20 orders/day. Around this time, in order to help spur the orders required to support their logistics network, they launched general merchandise categories with the aim of eventually selling everything. Sales increased over +250% y/y to RMB 1.3bn in 2008.

However, despite the strong sales growth, the financial crisis hit JD hard, and Richard had to scramble for more funds. Many suppliers began to demand more stringent payment terms, which drew on their cash flows. JD’s valuation dropped from $150mn to a low of $30mn. Capital Today made several bridge loans during this time, but JD was still often operating with only a few days of runway and under constant pressure of missing payroll. However, the stress this period inflicted on JD also neutered some of the competition. After successfully pulling through the crisis, JD earned a $265mn investment from Zhang Lei’s Hillhouse Capital at a $1bn valuation in 2010. In a telling show of Richard’s character, he insisted they get audited statements at the company’s cost so the investors knew there was nothing dishonest about their figures. This investment gave them a war chest to take share from other leading e-retailers right at the time competitor Dangdang IPOed on the Nasdaq, raising ~$272mn.

In 2010, JD also launched a “book war” against Dangdang and Amazon, who had close to a duopoly in the online book market (Taobao had a sizeable presence with used books). They launched aggressive promotions, giving free books out to their most loyal customers (Diamond users who spent more than RMB 30k) and steep discounts to everyone else. Within a year, Dangdang’s gross margins dropped 600bps to 14% and their stock dropped over 70%. Gaining share in the book category was also helpful to JD since most of the oldest ecommerce users were book buyers who first used Dangdang or Amazon who learned about JD for the first time through these promotions. JD, which was run very leanly and efficiently (for instance, they figured out six box sizes was the optimized number between increased logistics complexity and wasteful costs from mix-matching item size to box), was able to stomach the losses better and Dangdang was effectively defanged. Amazon would also soon decide its resources were better utilized in other markets.

A similar war would play out a few years later in appliances (yes, they shipped huge items like air conditioners, refrigerators, and washing machines) against the big box retailers Suning and GOME. Ultimately, JD, with fewer distribution layers and lower inventory cost, coupled with the advent of JD Service Stores in remote locations (local authorized dealers that provided delivery, installation, and later maintenance, but where JD would still be the product seller), gained material market share. Winning this category also meant building out robust logistics networks with a “bulky supply chain system” capable of handling large and heavy goods like stoves and ovens.

A few years prior, back in 2010, JD started opening up their platform to 3rd party sellers with their online marketplace. Similar to Amazon’s FBA, JD started providing sellers logistics services, which increased the volume running through their network and helped it scale more effectively. They also started developing services for sellers like advertising and financing, breaking out their finance unit as an independent business group in 2013. Also in 2013, JD Mall made another name change, dropping the “Mall” and moving their online website to the doman JD.com from 360buy.com. They also announced RMB 100bn in GMV and prepared for an IPO. A few months before their IPO, JD announced a strategic investment from Tencent, which was a game changer for them that greatly increased their reach to the Chinese consumer. In March of 2014, Tencent agreed to invest ~215mn and give JD their ecommerce assets (Paipai among them) in exchange for a 15% stake as well as a promise to subscribe at the IPO price to an additional 5%. JD IPOed on the Nasdaq in May of 2014, raising ~$1.8bn at a share price of $19, giving them ample liquidity to continue to invest in logistics and take advantage of their newfound partnership with Tencent.

In the years that followed, JD would add over half a billion new customers, going from 38mn in 2Q14 to 552mn in 3Q21. On the growth of their ecommerce platform, they were able to create new businesses that would later become their standalone companies with significant outside ownership or having gone public. JD Health, JD Technology, JD Logistics, JD Auto, JD Properties, and JD Industrial Technology (MRO), are just a handful of them–with others currently being incubated. Richard Liu continues to run JD today with a ~14% stake in the company (reduced after a recent charitable donation).

Business.

As it is probably clear by now, JD is an online retailer that facilitates the sale of their own first party goods and 3rd party merchants’ products through their online platform that is vertically integrated with their own logistics solutions, giving consumers the fastest delivery and strong customer service on a large selection of quality goods (over 9mn 1p SKUs).

87% of their revenues come from their direct product sales segment (1P) with the remainder attributed to Marketplace, Marketing, and Logistics Service revenue. Given the accounting of reporting 1P revenues at the full cost of the item vs 3P where only the commission is reported, this understates the importance of their marketplace business (see our SE piece for an accounting walkthrough of this). JD has not broken out 1P vs 3P GMV since 2016, where it was about 57% 1P and 43% 3P. We figure 1P is still higher than 3P, but the gap is likely less. Also last disclosed in 2016 was their GMV mix of Electronics & Home Appliances vs General Merchandise, which was split exactly 50/50. However, from 2013 to 2016, General Merchandise as a % of GMV grew 1400bps and it is likely it today represents a larger portion of GMV than Electronics & Home Appliances. However, this difference does not show up in the segment revenue mix since JD overindexes in Electronics & Home Appliances 1P (>60% of 1P). Below, you can see that 1P revenues from Electronics & Home Appliances and General Merchandise are 54% and 34%, respectively. Marketplace & Marketing revenues are at 7%, slightly higher than logistics sedrvices at 5%.

Revenue Segment Definitions:

Product Revenues. These are all 1P transactions (whereby JD is acting as the principal and responsible for fulfilling the promise to provide the sold goods). They further split up product revenues between Electronics & Home Appliance and General Merchandise (a byproduct of having started as an Electronics retailer). It is worth noting that for all 1P transactions, revenues are recorded net of value-added taxes (VAT), but the VAT would be counted in GMV (which is industry standard accounting).

Electronic and Home Appliances. This includes sale of 3C (computers, communication, and consumer electronics) as well as Home Appliances (including large items like refrigerators, air conditioners, ovens).

General Merchandise. This includes everything not listed above, but they specifically call out the following categories in their annual report: food & beverages, fresh produce, baby & maternity products, furniture & household goods, cosmetics & personal care items, pharmaceuticals & healthcare products, books, automobile accessories, apparel & footware, bags & jewelry. This is also all 1P.

Net Services Revenues. This is further broken down into two segments.

Marketplace and Marketing. These are revenues from charging 3rd party merchants commission fees that are either negotiated or a fixed rate, but 2-8% is the common seller fee range. Their 3P marketplace business is also referred to as POP, which stands for “Platform Open Plan”. Additionally, JD provides advertising services that allow sellers to place ads across their website and apps, as well as affiliated internet properties through their ad network. Their two categories of ad products are performance (pay for clicks or on the basis of a successful transaction) and display ads (more for brand advertising).

Logistics and Other Services. JD allows their 3rd party sellers to utilize their fulfillment and logistics infrastructure, as well as other sellers not on JD’s platform. The revenues generated here are from providing warehousing, distribution, freight, and express delivery services. Included in the “Other Services” is JD Plus, their membership program that provides users various benefits (more on this later).

It’s worth noting their revenue segments shown below are different than their operating segments (JD Retail, JD Logistics, and New Businesses) which we will discuss later.

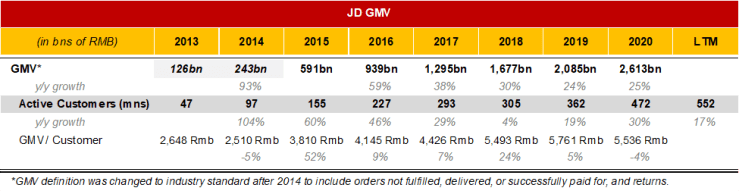

As seen above, LTM revenues are RMB 900bn ($140bn) and have grown ~8x since 2014 for a 36 CAGR%. Net Product Revenues have grown similarly at a 34% CAGR since 2014, whereas Services revenues have grown at a 55% CAGR. Today, Service revenues are growing at a >50% clip (9M21 y/y) whereas product revenues are +26% (9M21 y/y). Within Service revenues, we see that Logistics & Other Services has been growing faster than Marketplace & Marketing at 72% vs 25% for 2020, respectively (they do not disclose this breakout quarterly).

Above, we show that GMV has reached RMB ~2.6tn (~$410bn) for 2020 and as of 3Q21, active customers (at least one purchase in the prior 12 months) have reached 552mn. We will momentarily say a lot more about the GMV, how it is calculated, and frankly how it is very misleading (which isn’t a problem secluded to JD, but given their prior disclosures we can actually get a sense of the magnitude of GMV inflation. Still, this should have been emphasized more in out BABA piece). At a high level though, GMV/customer has been increasing to almost ~double over the past 7 years (the 2013 and 2014 GMV figures are prior to the definition change as we detail below). Note that GMV/customer growth can look lumpy when customer growth is very strong, as new buyers are not contributing a full year of purchase activity. Additionally, new buyer spend is less than seasoned buyers, but over time, returning buyers tend to spend more on the platform, especially as JD has continued to add more categories.

As you can see above, it looks like Covid-19 has been a boon to JD’s business, adding 190mn new customers, or almost 2/3rds of their total customer base at the end of 2018 in under 3 years. Recall Covid-19 started appearing in December 2019 for China, and in 4Q19 they added 27mn new customers (vs 11mn and 13mn for the two quarters prior). However, it turns out that a lot of this buyer increase can actually be attributed to them launching a money-for-value app under a separate brand, called Jingxi.

From 1Q18 to 3Q19, customer growth was very lackluster, with only 30mn users added in that whole period. However, it has been reinvigorated by Jingxi, Covid tailwinds, and more recently, their supermarket initiatives. Since both happened right around the same time (4Q19 Jingxi launched and first lockdown in 1Q20), it is hard to parse out what growth to attribute to each. Management’s call commentary stated over 80% of new users coming from lower tier cities might make you think it was mostly Jingxi, but Covid could have all the same been the impetus to make them another ecommerce platform, especially since JD’s logistics operation allowed them to deliver orders with far fewer disruptions than Alibaba and others.

There are 3 ways to buy something on JD: 1) their website, 2) their mobile app, 3) their Weixin mini program. The experience is very similar to other ecommerce sites, with a consumer able to complete a purchase in just 3 clicks after finding the item they want.

Swipe through to get a sense of JD’s mini program. The tabs are: 1) home page, 2) categories, 3) nearby, 4) shopping cart, 5) profile.

JD also offers free shipping on all orders over RMB 99 (~$16), but charges RMB 6 for orders under RMB 99 and RMB 8 for orders below RMB 49. Though with their loyalty program JD Plus, members can get free shipping on items under RMB 99 (but it is oddly limited to only 5 vouchers/month, which seems like an unnecessary stipulation for your best customers). JD Plus members also get discounts and access to monthly Plus Day sales. They also have other partnerships with a variety of providers that give members discounts and benefits at 15k+ hotels, free bundles with Tencent’s QQ Music and Bilibili’s premium video subscription, as well as limited promos like access to Baidu’s IQiyi video at no extra cost. Lastly, they have loyalty points, called “JD Beans” that users accrue with platform activity and purchases, which can be redeemed for various discounts. While every user can accumulate these JD Beans, Plus members get ~10x the points, which is another reason for ardent users to join the program. Similar to Prime, JD Plus members spend >2x non-Plus members. (They last disclosed 20mn Plus members in 2020, but it is likely now closer to 30mn as they noted it was growing 30% y/y.)

There are a couple things that are unique about JD, the first of which is somewhat a novelty, which is JD’s Luxury Express delivery service. Whereas orders placed are usually set to their default shipping option, which is JD’s inhouse logistics operation that delivers >90% of orders in 1 day or less (faster and more consistent than alternatives), there is an option for the “Luxury White Glove” service. As the name suggests, JD will send a delivery personnel in a suit with white gloves to delivery your package in a fancy box. While the vast majority of users will never use it, this service is popular with ultra-high-end brands like Audemars Piguet, who partnered with JD to not only provide the delivery, but also to set up their pop-up store on Weixin.

Audemars Piguet utilized JD’s Kepler Mini Program Solution to create a mini program on Tencent’s Weixin, which allows them to have a presence on Weixin to access their >1bn users, while still reaping the benefits of JD’s retail infrastructure. The Kepler program allows a seller to copy their entire JD store, including product SKUs and descriptions, into a Weixin mini program. The merchant not only benefits from easier access to Weixin’s audience and a more sharable format between their users, but is now also searchable within Weixin (and if you recall from our Tencent piece, more search is moving within the Weixin app with general search player Baidu becoming increasingly irrelevant). Tencent benefits because JD already had relationships with many brands, and this program helps move more activity onto their platform, which increases the functionality of Weixin and also creates more utility for Weixin Pay (the exclusive payment mechanism on Weixin at the time). JD benefits because they take a seller fee on the merchants’ sales and presumably, they could sell more when accessing Weixin’s audience than otherwise. This is part of the shift to “Retailing as a Service” that JD is pushing, whereby they enable the merchant however they want to sell, irrespective of whether the consumer enters directly through a JD storefront. The Retailing as a Service strategy allows a brand to control more of the consumer experience, while JD operates the infrastructure including warehousing & fulfillment, last mile delivery, returns, customer service, as well as financing and billing (more on this strategy later). This seems like a win-win-win for Tencent, JD, and the merchant, and it is this sort of beneficial arrangement that Tencent originally conceived when they invested in JD.

When Tencent invested in JD in 2014, they not only provided capital and their C2C marketplace Paipai, but they also critically helped JD with preferred placement in Weixin. There are “Level 1 Entry Points” and “Level 2 Entry Points” that Tencent can grant a company or service, and JD received both. Starting in 2014, a user who opened the “Discovery” section of Weixin or QQ Mobile (see our Tencent writeup to see these) would have an option to directly click on JD to open their mini program (this is also why this is referred to as “direct access”). This priority placement in the app meant that it was unavoidable for the hundreds of millions of people who opened Weixin dozens of times a day to not see JD. Level 2 access is in the Weixin Pay page, and shows up any time a user goes to their QR code to pay for something or check out financial services. This was invaluable promotion for JD. The year before they were promoted in Weixin, they had 47mn customers, which was up ~18mn or +61% y/y. The year following the introduction of the partnership, customer growth accelerated to +104% y/y with them adding ~49mn new customers—more than their entire customer base that they grew over the preceding decade. Following the 2nd year on Weixin/QQ Mobile, they grew customers +71%, still faster than prior to the Tencent relationship, even with a much larger base of users. Simply placing JD’s store link in Tencent’s app created enormous value for JD (and Tencent’s JD investment) by giving them a ton of traffic for free (technically valued in their deal).

JD has entered other partnerships since then, including one with Walmart that started in 2016. Under the initial partnership, JD acquired Yihaodian, Walmart’s online marketplace, but Walmart retained the Yihaodian direct sales business and started operating it as a store on the JD.com platform. This gave JD customers a marked increase in selection of high-quality goods from a trusted seller including a critical category—grocery (recall their General Merchandise push was hardly 2 years old at this point). Walmart would also become a preferred seller on JD’s O2O platform (quick local delivery) and receive a 5% stake in JD. A year later, they announced an inventory integration whereby JD customers’ orders could be fulfilled from a JD warehouse or Walmart store based on what is most logistically efficient. They also set up JD Home stores with Walmarts that primarily sold appliances and electronics (during their appliance war with Suning, GOME, and Alibaba). This “store within a store” allowed them to expand a physical retail footprint that could showcase products before customers purchased them and could accommodate returns and service requests.

It isn’t clear how many stores JD ultimately built in Walmarts across the country, but it is clear that they have a significant physical footprint today, and the vast majority of the stores are stand-alone with them significantly expanding product selection. Over the next several years, they would open up over 15k JD Home stores, virtually all of which are franchised out. The stores utilize digital price tags, customer tracking systems, facial recognition technology, among many other technologies, to feed an algorithm that helps inform what product SKUs to stock.

In addition to the JD Home format, they have started experimenting with many other formats.

JD Convenience Stores. This is a smaller store format that sells basic CPG items and food. They have intended to open (or rather, franchise) 1mn of these stores. They also have technological integrations with the rest of JD’s selling ecosystem.

JD Mini-Convenience Stores. These are even smaller than the above stores and are unmanned, relying on technology (facial recognition, video tracking, sensors) to charge a customer.

JD Mall. The JD Mall is a huge, 40k sqm physical space that houses over 150 brands and carries 200k+ products. All inventory integrates with their online channels so a consumer could have anything delivered to them rapidly. More unique though, is the space they allow brands to display their products.

JD E-Space (Super Experience Stores). These are technology enabled spaces with various “interactive zones” that include beauty services, wine tastings, coffee tastings, and gaming zones. These shopping centers are consumer-electronics-themed, but their products vary across most categories.

7Fresh. These are JD’s supermarkets that they are opening to address the grocery opportunity and tie in with their omnichannel efforts. Alibaba’s Hema supermarkets would be their most direct competitor here.

Other Physical Retail Store Formats. While JD now has ~1mn brick and mortar stores, management has signalled their desire to have 1mn brick and mortar convenience stores alone, and 5mn total brick and mortar stores by the end of 2023. In addition to the store formats listed above, they also have store chains for Tobacco (JD Tobacco), Alcohol (JD Alcohol World), Automobiles (JD Auto – more on this later), and Appliances (Jiangsu 5 Star), among many others.

Connecting the physical stores to their online channels is JD Daojia, their O2O (quick delivery service), which later merged with Dada (but is still a standalone public company that JD now owns 51% of after a $800mn investment). While it is hard to say how much consumers care about getting many goods in <2 hours (usually <1 hour), grocery is the clearest use case and thus JD and Alibaba are focusing here. However, we don’t want to give the illusion that all of this physical retail is simply to support their online businesses—the high penetration of ecommerce vs the rest of the world is largely a byproduct of the fact that the offline retailers never fully developed. Some estimates put China’s total physical retail square footage per capital at 1/10th the amount in the US. The whole array of specialty chain retailers like Home Depot and Lowes for home improvement or AutoZone, Advance Auto Parts, Pep Boys, and O’Reilly’s just for aftermarket auto parts & accessories never developed in China. While it seems likely the US has too much retail, China clearly has the scope to grow their retail footprint and JD and Alibaba are increasingly moving to fill that need. They are both adding a tech layer to their retail, revisioning retail without the legacy footprint and aged systems most retailers operate with today (Amazon is doing this too, with their Go Store).

JD should, in theory, have much higher inventory turnover with lower obsolescence risk given they can coordinate purchases between their huge volume of online orders and their warehouses and stores. However, the store format does not lend itself to quick fulfillment, which is why Alibaba and JD both felt the need to add quick delivery service capabilities (Ele.me / Consumer Local Services for BABA and Dada for JD). In grocery, this could be an important strategic advantage as grocery is high frequency, high total order value, and provides many opportunities to cross-sell, while simultaneously habituating the user to their platform. The grocery TAM in China is estimated to be in excess of $2tn and can grow as more Chinese acquire an affinity for higher end foods. Today, it is highly fragmented with the largest chain, Sun Art (now controlled by Alibaba with a 72% stake), estimated to have a single digit market share (in a 3Q20 earnings call, management said the top 10 supermarket brands only take a 5% share). With a huge, fragmented TAM, JD is pushing to take their share with JD Super, 7Fresh, Dada, and their Walmart partnership.

Grocery stores typically have very thin margins with multiple layers of distribution that mark up the product at each stage and are subject to large losses from food spoilage. Both are problems that JD hopes to be able to solve: 1) utilizing their logistics network to bypass distributors by going directly to the farm to get produce for their supermarkets, 2) using their AI technology to better estimate demand for each product to decrease food spoilage. Additionally, the consumer would receive a higher quality and more consistent product vs. the array of mom-and-pop markets that order from a panoply of different distributors. The strategy shows some signs of working—in 2Q18, they noted that their 7Fresh stores were producing 3-4x the sales/sqft of a traditional supermarket. However, there is very limited other info on their stores and essentially nothing on how the economics of these stores and franchises work.

Other Businesses.

Jingxi. The Jingxi business is a mix of three different businesses. The first is the money for value and social commerce platform, Jingxi (and when we refer to Jingxi throughout the piece, this is what we are referencing. The second is their community group buying app Jingxi Pinpin (referred to as Pinpin hereafter). The third is there convenience store business (referenced above), which is referred to as Jingxitong. We will mostly focus on Jingxi and not Pinpin, since Jingxi is far larger. Just so you know some differences though, Pinpin is more gamified with countdown timers, essentially everything on the platform requiring a group (sometimes as low as 2), and with sharing as a more focal feature. There is also more produce and food on Pinpin. Jingxi is a little less gamified with a more eclectic selection of products. Jingxi has offerings that do not require groups to buy, features more deals, and has livestreaming.

Photos 1 and 2 showcase the Jingxi homepage and a sample selection of goods. Photos 3 and 4 showcase the Pinpin homepage and a sample selection of goods.

This business originally started as JD Pinguo, and was designed to acquire users through group buying with the ultimate aim of bringing them into the greater JD ecosystem (originally designated as a user acquisition department and not an independent business). However, in 2019, when JD and Tencent renewed their 5-year deal, they opted to put the newly-named JIngxi at the Level 1 Access Point in Weixin. It was at this point that Jingxi helped JD reaccelerate customer growth, which had dramatically slowed.

The slowdown in buyers was because their service primarily targeted Tier 1 and Tier 2 cities, with lower tier cities being harder for them to penetrate. Jingxi was designed as a new channel, under a new brand, to expand their user base into the lower tier cities that JD’s value proposition was not a proper match for. Jingxi was very different than the JD.com app with users spending more time exploring, being more spontaneous in purchases, but also, critically, being highly price sensitive. This is the market that Pinduoduo brilliantly attacked early on, and at one point last year, had more buyers than, but since BABA re-entered this market with Taobao Tejia and revamped their Juhuasuan (flash sales), reclaiming their spot as the ecommerce company with the most buyers (today at 867mn vs BABA’s 953mn).

JD was late to focus on this demographic as well, but with Tencent’s Level 1 Entry Point, they were able to quickly acquire a lot of users without the same level of promotion and discounts that PDD and BABA needed (estimated ~250mn users in 2020). Some estimates put Jingxi’s GMV at ~10% of JD’s total, despite users spending less with lower AOVs (average order values).

While it may seem like they are all similar offerings, JD’s positioning is slightly unique as they rely on their preexisting supplier and manufacturer relationships to procure goods, which in theory translates to higher quality. It is also worth considering that they are the only player with a direct sales business (PDD exited theirs), which could help them procure goods at prices that a manufacturer may not be willing to offer otherwise (also recall how JD go started in the early days). Additionally, their logistics network allows them to deliver packages cheaper and more efficiently to customers than BABA and PDD, who rely on 3rd parties. While Jingxi clearly is starting out with good traction, their competitive advantages seem more theoretical with the Chinese internet riddled with complaints of shoddy ordered products that were canceled and disappointing products. There likely is some bias whereas you aren’t going to write a review if you are happy, but it’s worth keeping in mind that Jingxi isn’t just a poor man’s JD, it is through and through a lower quality service (poor customer service is another common complaint). This is why JD bifurcated their brand in the first place when they moved down market. This isn’t problematic per say as the alternatives are all similar and these customers value a low price more than anything else. Thus, they are likely to come back even if there is a poor experience to get another big deal, but the issue is if they are burning money to support this business that may never be unit economic profitable.

Their lack of profitability could come from three main reasons: 1) their customer acquisition costs are too high, 2) their retention rate is too low, 3) each transaction isn’t contribution margin positive. The first issue and second issue are inter-related, with the concern being that they are paying for a user that JD ultimately does not make a positive return on. For instance, if they pay RMB 40 to acquire a user, and that user only makes three purchases with AOVs of RMB 30; with 20% contribution margins (margin after direct variable costs), they lose RMB 22. They can make money by either keeping their acquisition costs under the user’s contribution margin (under RMB 18) or by increasing the user’s retention rate (getting them to order more than three times). With poor consumer experiences, they create churn events where the customer never comes back (like the several reviews we read who swore they would never again shop on Jingxi). However, for this business model, high churn is not totally consequential, as the cost to get that user back in most cases tends to be rather low—a small discount on already cheap goods will probably do it given how price sensitive these users are. While it never seems sane to say that high churn is okay, we just don’t think it is necessarily problematic for this sect of the market. As far as customer acquisition costs (CACs) go, we actually think JD’s CACs are rather rational. One source put it RMB <10, with a popular promotion being small cash rebates of a few RMB after you share a link with 4-5 friends. Management also noted in their call commentary that they were skeptical of some of the subsidies that were going on in the sector. A low CAC means that you do not need to sell many items to recover your cost and make a profit.

This leads us to our 3rd factor, the contribution margin of each order. With low AOVs, that means you need a higher # of orders to make back your marketing cost. The high churn, though, is an obstacle to high frequency. But putting that aside, the low absolute value of each order will make it very hard to make a profit. If customers have an AOV of RMB 30-50 ($4.70-7.80) and if the item was marked up 15-30% (recall Costco marks up items 15%), then that would be a 13-23% gross margin, or RMB 3.9-11.5 ($0.60-1.80) to cover packaging, fulfillment, and last mile delivery, not to mention all of the personnel involved in procuring merchandising. When we checked the platform, most items, despite being only a few RMB, had free shipping. (The uneconomic shipping was likely not included in our sources’ CAC calculations, but it should be.) We don’t have any hard evidence to inform out unit estimates here, but we wanted to illustrate how difficult it is to make money delivering small value packages of discounted goods to fickle customers. At a high level, we can say that it is likely burning money though. Below, we estimate that Jingxi is losing at least ~$100mn/quarter, but could be much larger (total new businesses are burning an average of ~$385mn/quarter in 2021). This run rate loss isn’t terrible in the scope of things, given their Retail business cash flow can sustain it, but we would hope that they do not continue to burn that unless there is a clear path to unit economic profitability with a sustainable consumer base.

This is all to say that this business is unlikely to ever generate meaningful profits relative to JD’s core retail business, but there could be an ecosystem advantage to having it. Suppliers like having this channel option that allows them to quickly sell goods in bulk should they need to unload some obsolete inventory, and the higher package volume helps them continue to refine their network’s efficiency. Lastly, “group leaders” (the ones who pick up and disseminate the goods in group buying), which would not only allow the shop owners to make incremental money, but it also drives traffic to their stores. JD management seems to have their focus on the right factors here, saying on a recent call that they “believe cost efficiency and customer experience are always the key to the longterm success of the retail industry”, which translates into the supply chain and logistics capabilities rather than merely competing through subsidies to expand scale at whatever costs. Assuming they can make the unit economics work, we could actually see JD having an advantage vs. PDD and BABA with their direct supplier relations, more scaled delivery network, as well as their retail foodprint which could act as pickup points. However, make no mistake—this is a much lower quality business than their core.

International. JD has started to operate international operations, mostly in Indonesia, where JD.ID is valued above $1bn. They started a trial operation as early as 2015. With an initial focus on 3C and appliances, now maternal products, food, and FMCG are among their most shopped items. Their value proposition is similar to what it originally was in China a decade prior: fast delivery and authentic products. While they have a sizeable 1P business, they have since added over 30k merchants to sell alongside them. With features like “Nearby Shops” that allow a user to see what stores are nearby and what items they have in stock, they offer something unique for merchants and consumers alike. Likewise, their logistics operation is a big competitive advantage that allows >85% of orders to have same or one day delivery on a wide range of their 1P products (competitors typically take 5-7 days). They have also partnered with Gojek (and received an investment from them), for quick, on-demand delivery for groceries. They already have 18 warehouses and 142 distribution stations in Indonesia, which cover 90% of provinces. They have an estimated 20mn+ buyers today with 350k+ SKUs.

JD is also expanding with a physical retail footprint and cashier-less stores. This will help them build a brand and draw attention to their online offerings while allowing integration with omnichannel initiatives. They also have started to move into Thailand (JV with Thai conglomerate Central Group), Vietnam (via an investment in Tiki), and The Netherlands (via 2 physical stores). While Shopee, Lazada, and Tokopedia, all currently have a lead on JD, they have a distinct value proposition, and we could see them as a dark horse, gaining a loyal consumer base over time as they address the two weakest points of these other marketplace platforms.

JD cashierless stores in Indonesia.

In additional to going international, they also help cross-border trade with JD World and their Shopify partnership, whereby they let global sellers access the Chinese domestic market through moving their listings onto JD’s platform. Lastly, they have a Google partnership where Google invested $550mn in JD, and will help provide them listings on their Shopping tab, with a focus on developing markets like Southeast Asia. However, they will also make a limited selection available globally, including the US and Europe. We are positive on their efforts to help facilitate cross-border trade, especially into China, and think their efforts in Indonesia and Southeast Asia could be a great longterm growth opportunity. That said, we wouldn’t hold our breath for any inroads in the more mature US and European markets.

JD Logistics. JD Logistics is operated as a separate busines sunit and recently IPOed on the Hong Kong Stock Exchange (HK: 2618), raising $4.5bn to continue to invest in their network and infrastructure. JD retains an ~70% stake in them and consolidates their operations on their financial statements. Their current market value is ~$20bn.

JD Logistics is JD’s inhouse logistics platform that they not only opened up to 3rd party sellers to sell on their platform, but also to 3rd parties who sell elsewhere. JD’s logistics network is one of their strongest competitive advantages that enables >90% of orders to be delivered in one day or less, so it may seem odd that they are giving this capability away to everyone. The logic is likely that more package volume increases their network density and thus decreases their cost per package. This allows them to reap cost savings, while they also can earn a return on delivery 3rd party packages. Given their scale, they can still offer low prices and make more profit vs. altnerative options. Furthermore, as Alibaba’s Cainiao stitches together many different 3PLs, over time they may be able to provide a competitive, if not better service than JD. This could mean JD has less of a lock on their sellers, who utilize their fulfillment service, as Cainiao increasingly becomes a better option. To be clear, this is far off from happening, but nevertheless, to get ahead of this, JD is taking on volumes unrelated to their own retail business in order to continue to drive down their cost structure. As they continue to entrench their position as the leading scaled logistics provider, they can offer better delivery to JD customers as a lower cost to themselves, while profiting off of 3rd party volumes.

As JD Logistics is the only global stand-alone logistics operation that grew from an ecommerce player, there are a ton of different insights we can draw that not only are interesting to JD, but other global ecommerce players. However, in order to best capture all of those, we have decided it would be best to do a separate deep dive into JD Logistics as our next report, so stay tuned!

JD Property. Established in 2018, JD Property owns, develops, and manages the logistics facilities that support JD Logistics. JD Property also helps facilitate the sales and leaseback transactions so they can recycle the capital back into other development projects. They have raised two Core Funds so far, whereby outside LP investors provide 80% of the capital in return for a steady return, and JD Property puts in 20% as the GP. Logistics properties are in high demand since they do not have the same tenant risk that commercial properties may have, and investor can diversify into a somewhat different asset class (when retailers and commercial lenders were wrecked by Covid, logistics warehouses were untouched). This strategy allows them to reduce their capital needs while allowing them to build properties to their needs and keeping them in control. They will likely IPO this at some point in the future.

JD Technology. JD Technology was born as JD Finance in 2013, and their first product was Baitiao, which is a credit product that allows users to pay for a good 30 days late, or over a 3-12 month period (basically BNPL). However, Alipay was much more popular, and their Huabei product, which was actually launched after Baitiao, blew them out of the water. JD also created their own payment system, but their market share essentially rounds to 0. They had some success with merchant financing (including Baitiao) to their 3P sellers, but generally speaking (compared to Alibaba and Tencent) they missed the finance opportunity entirely. Recognizing this, they tried to shift their value proposition, attaching AI and Cloud services to their offerings in a confusing array of services. By 2017, they were talking about the “Financial Cloud”, which confuses us as much as it seemed to confuse management, since they never found anyone who needed it. In 2018, it was restructured and renamed to JD Digits to help their “de-financialization” of the unit to broader technology services in part to avoid greater regulatory scrutiny. They had raised $5bn over several years, but struggled to find clear use cases that customers wanted. However, their motley crew of products that served intelligent cities, agribusinesses, financial institutions, and AI services generated enough revenue to put together an IPO slated for April 2021. At the time, they only disclosed 2019 revenues, which were $2.8bn, growing 37% y/y (a 1,600bps deceleration from the year prior, despite a much lower revenue base vs. peers). However, with increased regulatory scrutiny in the financial sector (Alipay IPO being pulled), they pulled their IPO. They restructured again, laid off staff, and purchased JD’s AI and Cloud assets for $2.4bn before changing their name, again, to JD Technology, in an attempt to explicate themselves completely from their original financial services ambitions (however, the vast majority of their revenue reportedly still comes from financial services, BNPL in particular). Lastly, owing to a stipulation in their 2017 fundraising round, if they do not IPO by 2022, they will have to buy the investors stakes back at an 8% annualized rate (something they could be rather ecstatic about if they were successful, as an 8% cost of capital is a rather low hurdle). Thus, they are planning a second attempt at an IPO in 2022, not even a year after restructuring their business. While JD only owns a minority ~42% stake, Richard Liu has majority control.

JD Health. Capitalizing on their consumer base and ecommerce capabilities, JD started connecting with healthcare and pharmacy providers to open up an online “Pharmacy”. While the capability to deliver products to consumers was solidly within their prior competence, there was a clear opportunity to expand into healthcare services like online consultation, prescription renewal, and telemedicine. In similar themes with other business, they saw the desire for omnichannel, so they launched partnerships in over 200 cities to help get a patient to see a doctor in person or a hospital if need be. They have over 109mn active users and are run-rating over >$4bn, but are still operating at a loss. JD IPOed this business in December 2020, raising ~$450mn in the process to continue to penetrate the healthcare opportunity. JD has retained a ~70% stake and today it has a $25bn market cap. We may do a separate deep dive on them if there is interest.

JD Industrial Technologies (MRO). MRO is an acronym for maintenance, repair, and operations, and JD MRO is a B2B service that caters to manufacturers. In a press release, they note that JD MRO is “connecting big companies with industry-leading service providers for manufacture-level omnichannel service solutions”, which sounds like a whole lot of jargon to us. But we essentially think they want to help connect manufactures to service providers so JD can sell them more specialized equipment that would require expertise to install. They note that at first, they will focus on 1) sending teams to a client’s factory to help consult with purchases, 2) offer professional installation and maintenance, 3) provide forwarding warehousing services. While there isn’t a ton of information on this segment, we do know they raised ~$230mn at a >$2bn valuation last year, and are looking to IPO soon.

JD Auto. This is a commerce segment that was carved out to focus exclusively on Automobile services. While they had auto supplies on their JD.com platform for a long time, there was a consumer desire for more auto specific expertise, as well as installation and repair services. To meet this need, JD rolled out the JD Car Club, which allows repair shops to join their network after being screened for quality. This allowed JD to extend their trusted reputation to a field that is usually fraught with exploitation and inconsistent service quality. Those in their Car Club network also get access to JD’s B2B auto parts platform, whereby they can aggregate their demand to get better terms with suppliers, passing off savings in the forms of lower costs to the consumers. Additionally, they link into JD’s CRM systems that allow JD to help control their inventory levels, including auto ordering. JD’s ability to have full visibility into the supply chain will help reduce redundant inventory, saving costs, while keep stock at adequate levels. (This is capability is called “Cloud Match” and something similar is used in other businesses). They go even further by training technicians on car part ordering policy as well as maintenance skills, which helps standardize services across their network. In total, they have a network of over 1,200 maintenance shops (and another 300+ core members who utilize the Cloud Match service). Lending their brand to 3rd parties is a double-edged sword though: it can either be an easy way to create differentiation and provide value to the merchant at zero costs to JD while simultaneously creating more merchant lock, or it can lead to a degradation and dilution of the brand value should their 3rd parties represent them poorly. As long as they keep screening new sellers and closely monitor any potential customer complaints, franchising is a great business.

Here we are seeing JD’s strategy of incubating these niche selling opportunities in various sectors into full standalone businesses (see what the standalone app looks like below). As we mentioned previously, Chinese retail environment is very underdeveloped despite “being ahead” on ecommerce. These high penetration rates are largely a byproduct of there being no good local alternatives. In the US for instance, as we noted, there are no fewer than 4 auto specialty stores that serve consumers as well as mechanics with a staff that are experts in that domain. This creates a very interesting opportunity for JD to go from general online retailers to one that caters to various specializations via omnichannel. Of course, this is no easy feat, and these new businesses will require very different focuses than their legacy consumer ecommerce business, so it makes sense that JD wants to make these independent businesses with different leadership, outside ownership, and capital. However, JD still remains a majority stakeholder in most of these for now, even after some have IPOed (ie JD Health, JD Logistics). We think this strategy allows a lot of optionality with minimal risk and helps embed JD’s commerce operations very deeply in a plethora of more merchants.

Operating Segments.

Earlier, we went over JD’s revenue segments. However, their operating segments are slightly different than their revenue segments and the way we presented them above. They operate through three segments: 1) JD Retail, 2) JD Logistics, and 3) New Businesses. JD Retail includes their core 1P and 3P business, as well as their seller services including advertising. JD Logistics is their logistics operations including warehousing, line haul, fulfillment, and last mile delivery services. New Businesses include JD Property, Jingxi, JD Health, and their convenience stores (Jingxitong). It is not entirely clear where they place all of their other retail initiatives as they are too immaterial for them to separately break them out, but we believe they are housed in the New Businesses segment.

JD Retail has a 3% operating margin (before unallocated overhead including stock-based comp) or ~$4bn in operating income, which still has room to improve. Management guides longterm retail margins to being similar to other large retail chains like Walmart, who is currently around ~4%. However, they also call out seller services (advertising is especially important) as raising that 1-3 points for a high-single digit steady-state margin. We will talk more about this later in our revenue build. Also note that 1) JD Logistics has operated profitably before, but as they reinvest in the business, they are now burning ~$650mn annually and 2) their New Businesses are run rate losing ~$1.25bn. A quick note on these figures: they are before including RMB 3.9bn (~$615mn) of SBC and amortization LTM. We are okay ignoring the amortization as it is the result of acquiring intangibles from acquisitions and not a real economic cost (although their mixed acquisition history may make you want to account for it), but either way, the SBC represents ~90% of the unallocated amount and applying a majority of that to JD Retail (given it is their biggest operation) would clip their margins ~40bps.

Before we go into China market dynamics and JD’s value proposition vs. the competition, we wanted to touch on some of the accounting behind the metrics we reference. (You may skip to the next section if in-depth accounting discussions aren’t your cup of tea, however it does allow us to back into some interesting insights on JD that we will utilize later in our revenue build.)

GMV and Revenue Accounting.

To start, JD used to report Core GMV and GMV. The difference being that Core excluded Paipai, the C2C platform acquired from Tencent in connection with Tencent’s JD investment. Paipai was relatively small and the difference between the two was around ~5%. Paipai was eventually closed down (largely due to a large presence of counterfeit/inauthentic products), but we will ignore the impact of Paipai for the rest of the GMV discussion, as relative to the other factors that affect GMV, it is trivial.

The confusion with GMV comes from the fact that the “industry standard” is a very flawed metric, which JD tried to improve on, but only exacerbated the confusion in the process. At one point, they had 3 different GMV metrics: Core GMV, GMV, and then a GMV figure in the footnotes which were in-line with the industry’s definition. The variance between “industry standard” GMV and the GMV figure JD highlighted was large, almost 40% greater (RMB 939bn vs. RMB 658bn for 2016). Compounding this problem is the fact that since JD reports 1P revenues (Net Product Revenues), when investors wanted to draw a comparison between their 1P revenues and their 1P GMV (which was temporarily disclosed), there was a further >50% difference (RMB 372bn vs. RMB 237bn for 2016). All of this added to the impression that there was some accounting malfeasance and JD was targeted with several short reports. While we will readily cede that all of this is unnecessarily confusing and could definitely be presented in a clearer way that is indicative of the actual underlying platform economic reality, we are able to explain all of it and largely piece it together. The outcome is that GMV is greatly overstated from the actual transactions that take place (remember: this is an industry problem, not specific to JD). However, the different pieces we go through are not just accounting chicanery, but actually informative to JD’s business.

As shown above, there are two GMV metrics JD reported for 2015 and 2016 (also reported for a partial period of 2014 and 2017). To help simplify, we will only focus on annual 2016, which is the last full year they reported Method 1 GMV. As you can see, there is a huge variance between the original method (Method 1) and the second method they moved to report exclusively in mid-2017. The difference between the two methods is explained in the footnote below.

As the boxes in the picture explain, Method 1 basically excludes any orders over RMB 2k that are not ultimately sold or delivered, and Method 2 raises this exclusion to RMB 100k and also excludes buyers who spend more than RMB 1mn/day. This exclusion is ostensibly done in order to reduce fraudulent transactions, or what is known as “brushing”. Brushing is the practice of creating fake purchase orders in the aim of moving your product up the search result page as well as having the opportunity to create fake positive reviews in order to entice other buyers to purchase your product. JD notes this in their risk disclosure below. Why RMB 2k is picked as a threshold is not clear, as it is still a sizeable enough sum that you could conduct brushing, but as it will be made apparent by the end of this section, it still does eliminate a ton of uneconomic activity.

Given the nature of 1P, whereby JD is the seller of the goods, there isn’t an incentive at the company level to create “phantom” transactions as JD would want the customer to be able to best delineate between mediocre and quality products. However, within the group level, there are some stories of product managers being bribed to make a certain product look more favorable by creating fake sales. That said, this behavior is rare, and JD deals with it harshly, immediately firing them and sometimes pressing charges (some have even served jail time). This very harsh crackdown partly harkens back to Richard Liu’s childhood where he would notice that the village head always had pork available to himself, but the village seldom ever had it (Richard has said that he would only get to eat it twice a year at most). He thought there was something immoral about someone using their power to accrue gains to themselves at the cost of everyone else and has since created a culture at JD that is extremely intolerant to graft and even the appearance of malfeasance. Nevertheless, there are still occasional stories of suppliers trying to bribe the purchasing managers in one way or another, but we believe that this is very rare within their 1P business. However, their marketplace business is much harder to police, and we are sure brushing was and still is widespread, which inflates the reported GMV figure. Interestingly enough (and bizarrely), they fully acknowledged this on a 3Q17 earnings call saying:

It is odd management acknowledges the futility of a metric they will continue to provide, while making clear they opted for the worse metric (that fits the industry definition), rather than their metric that they believe was more indicative of the underlying economic reality of the platform. While we can give them credit for flatly saying “it should not be relied on for financial analysis” purposes, it is very odd that they chose to provide a metric they think is nonsense to conform to industry standards over helping their investors understand the business better. We have heard they did this because the press would constantly misreport their market share, using the smaller figure that has a more onerous exclusion whereas peers had a more generous definition, but this seems like a shallow reason to us. Alibaba’s definition of GMV doesn’t actually make clear if it is the same definition that JD now uses. In BABA’s definition of GMV (shared below), we see that they use similar language as JD and note they exclude certain product categories over certain amount and buyers who spend a certain amount per day. But we don’t actually know what these limits are. Alibaba does say they try to eliminate the impact of fraudulent transactions, which seems somewhat comforting, but is sufficiently ambiguous that you can’t actually draw any conclusion from it. The more limited information compared to JD’s disclosure does make it seem a little misleading, but it is also possible they have a more nuanced system than a blanket RMB threshold. (We should have emphasized this point more in our Alibaba write-up, but in contrast to JD, BABA stands by their GMV figures, even using them to calculate their monetization rates. We have a more mixed opinion on the veracity of this having dug into JD more.)

However, we couldn’t argue if someone claimed that whatever level of brushing JD’s platform has, Taobao (and Tmall to a lesser extent) is as bad, or worse, since JD has a more stringent 3rd party seller screening process and is harsher on seller misbehavior. (We would caution, though, that it is hard to make any claim about the magnitude of brushing on Alibaba as there isn’t any disclosure that can inform us, and even when there is brushing, we don’t know whether it is included in GMV. While this isn’t an Alibaba piece, we would say that the implications would be their monetization rate could look higher than it really is and spend per buyer would be less. The former would be a negative and the latter a positive.) Another factor that could mitigate this behavior on JD is the fact that they charge seller commissions, whereas Taobao doesn’t, which makes brushing near costless.

While we have noted the differences in GMV methods for JD, before concluding with the ramifications, we first look at 1P GMV vs 1P Revenues below. As you can see, 2016 1P GMV is RMB 372bn whereas reported 1P product revenue is RMB 238bn. Given this huge disparity of RMB 134bn, or 36% of GMV, we wanted to walk through the delta below.

We first start with Net Product Revenues of RMB 238bn (2016), and we gross it up for the VAT (value-added tax). This variable is relatively easily accounted for, as they note it ranges from 13-17% based on product category. Most merchandise appears to fall into the 17% category, so we assume a figure towards the high end at 16%. We take the reported net product revenues and gross this up by the VAT to get the product amount including taxes. The difference between this figure and their 1P GMV is a grab bag of different items. Remember we are comparing 1P revenues to 1P GMV, and we are assuming that JD does not engage in brushing on their own platform for reasons mentioned prior, so that would not be a factor here. This difference would be (1) discounts that JD offers consumers, (2) orders that are returned, (3) placed orders that are later cancelled, and (4) other business taxes or fees, which we think is the least consequential factor. As far as items 1-3 are concerned, it is hard to discern how to weight them, but it is not uncommon to have a ~20% return rate. While this rate isn’t problematic in and of itself for an ecommerce company, it is interesting to see it calculated as it is seldom broken out directly. Below, we use it to inform our analysis on the 3P marketplace.

The analysis we ran in the prior exhibit allows us to estimate what 3rd party sellers net revenues are, which when layering in Marketplace and Marketing Service Revenues, gives us an estimated take-rate of 9.2%. This will be relevant later on when we think about take-rates, even if it is a figure that is 5 years old. Additionally, we note that every $1 of “Method 1” GMV turns into an estimated 65 cents of revenue (a ratio that would hold for 1P as well). We call this ratio out because it will help make apparent how much the quality of GMV has deteriorated. It should be noted that the Method 1 definition only excludes transactions that are not completed above an arbitrary limit of RMB 2k (or ~$315). So to the extent there is brushing in JD’s marketplace of transactions under RMB 2k, then seller revenues would be less and the take-rate would be higher.

Next, we run this analysis on 2016 figures, because under the latest “Method 2” GMV figures, all of this is greatly obscured as we show below.

In the exhibit above, we make up two terms to help clarify our analysis: 1) Platform Revenue which we define as total revenues generated from the underlying GMV. This is calculated by adding JD’s Net Product Revenues to the 3rd party revenue estimate we calculated in above. 2) Revenue Monetization Rate which we define as Platform Revenues / GMV. This metric shows how much revenue is generated for each dollar of reported GMV and is designed so we can get a sense of the quality of GMV. A high rate suggests that most of the GMV has a true economic nature vs. just being brushing, returns, cancels, taxes, or prices prior to discounts. As you can see, the rate deteriorated dramatically under the Method 2 accounting treatment to the point that not even half of each dollar of GMV translates to revenue for JD or a 3P merchant. In 2016, GMV increased an astonishing RMB 281bn under Method 2 accounting, but of course this was not accompanied by any increase in real economic activity. We partially want to give kudos to JD for originally excluding all of this activity (transactions over RMB 2k that were not completed) from their GMV calculation, but then are disappointed they reverted to inferior metrics for ostensible vanity reasons and have to take stock in management’s judgment for that decision. (If the issue really was the press kept taking the GMV figure at the top of the report and not in the footnotes, then why not just switch their positions…)

Market Dynamics and Value Proposition.

With a strong sense of JD’s accounting, we will now move onto JD’s value proposition vs. their competition, and general market dynamics. As we have noted in prior pieces, China’s offline retail environment never had the chance to mature before the advent of the smartphone and widespread adoption of the internet. As a result, ecommerce subverted a lot of physical retail development. Ecommerce penetration (portion of retail sales conducted online) in China remains the highest globally at an estimated ~35%, but physical retail square footage per capita is about 1/10th of the United States. The rapid rise of the Chinese middle class coupled with inadequate retail infrastructure set the perfect stage for ecommerce to thrive. While Alibaba’s Taobao (2003) was the first Chinese-born company to capitalize on this opportunity in a big way, JD was close behind, moving fully online just a year later. However, the differences in their models meant that Alibaba could grow much more rapidly with minimal capital expenditure, whereas JD’s growth would be limited by their financial credibility which constrained their ability to procure a wide variety of goods at cheap prices. Thus, JD expanded slowly category by category. Alibaba enabled merchants to conduct sales online and could disregard the merchants’ listing prices and their COGS as the marketplaces’ competition would ensure the lowest cost producer would win out overtime. When Alibaba moved into logistics, they took a similar approach in creating Cainiao, a logistics platform that 3PLs (3rd party logistics providers) plug into. This essentially empowers logistics companies to effectively compete against each other, driving down the cost of providing delivery services. Here again, JD took the more expensive route, opting for a fully integrated in-house logistics system, which had to be built out painstakingly and expensively, district by district. By the time JD opened up their platform to 3rd party sellers, they already had a strong reputation that allowed sellers to comfortably associate their brands with JD’s retail channel whereas Alibaba had to start over fresh with Tmall to bifurcate their seller base and signal higher quality to the consumer. This all means that the average consumer would associate JD with quality followed by Tmall and then lastly (and much further behind) Taobao. Below, we will touch on the different ecommerce players in more depth (taking much inspiration from our Alibaba Piece’s Competition section), but first we wanted to think about different factors that a consumer considers when weighing different shopping options. We will do this by talking about a concept we will refer to as the “Consumer’s Hierarchy of Preferences”, a term we do not believe has been used elsewhere but is very apt for the concept we want to convey.

The Consumer’s Hierarchy of Preferences.

There are ten factors an ecommerce provider can focus on to provide a distinct value proposition to the consumer. We will spit this into two groupings: the first group is 6 factors that a consumer would always want to be the best possible, and the second group is 4 trade-offs. In the first group are 1) trust, 2) selection, 3) price, 4) delivery speed, 5) consistency and 6) order ease. These are all things a customer wants to be as good as possible. The second group is 1) discovery commerce vs. intent-driven commerce, 2) product standardization vs. uniqueness, 3) gamification vs. utilitarian UI, and 4) group buying vs. independent purchasing. These are trade-offs even though a platform may try to cater to both ends: in reality, they only tend to do one well.

Similar to Maslow’s Hierarchy of Needs, once a consumer gets one of their preferences filled on some level, filling their next order preference becomes more important than improving on that first one. For instance, many consumers may want the lowest price, but once it is competitively priced, they would care less if it’s 5% cheaper than if they can receive it this week, and if that condition is met then they care more about free returns than one day shipping and so on. We will refer to these different variables that a customer weighs and shifts as lower order preferences are met as the Consumer’s Hierarchy of Preferences. (This is a concept we have alluded to, but never defined in prior pieces.) The first group of 6 preferences need to all be done well at some level for an ecommerce company to be successful, but different players may emphasize different variables more. Coupang, for instance, has competitive pricing, but they are not always the lowest, and we could find some items that were priced 10-15% higher than other online options. However, buyers in Coupang’s “Consumer’s Hierarchy of Preferences” value other variables higher, so Coupang moved to focused on those variables, accepting that a few items may be listed somewhere else for more.

How you create consumer value is finding out the Consumer’s Hierarchy of Preferences and meeting as many of those preferences as possible. Once you address a minimum level of preferences (and these preferences can be quite low– like a convenience store having some drink that can quench your thirst), you have successfully earned a customer. However, operating your business to provide customers the worst service they would still transact at (essentially their indifference point) is a dangerous proposition as consumers’ preferences will change the moment someone offers a superior value proposition and that will become their new standard. For instance, a decade ago, guaranteed 4-day shipping on any good would sound delightful, but today we would scoff at anything longer than 2 days (and 1 in most cases). So, in order to have a strong hold on your customers, a company’s aim should always be to meet as many of a consumer’s preferences as possible.

When a company addresses a Customer’s Hierarchy of Preferences beyond their “indifference point” of transacting, they are creating surplus consumer value. While there is a tendency with many businesses to want to move as much “value” to the shareholders, the best businesses always leave some surplus consumer value. The reason for this is simple: the most valuable customers are those who stay. We don’t mean this flippantly, but rather if you were to run an LTV (lifetime value) analysis on a customer you would find that the biggest factor that influences a consumers lifetime value is churn. Of course, there is no mathematical equation that tells you when you reach a consumer’s indifference point (ignore the economics lessons that say otherwise), so being obsessed with capturing value rather than creating it usually results in pushing too far and thus eroding the customer value proposition, which is very hard to recover from (customer re-acquisition cost is going to be higher than that incremental dollar you grabbed). This is clear when Bezos endlessly talks about “customer obsession” and “always delighting the customer”: he is not concerned about pricing to maximize dollars today. Similarly, Costco steadfastly refuses to mark-up products beyond 14-15% above cost regardless of whether the market would bear a much higher price. This comes from the same ethos of creating as much consumer surplus value as possible in order to keep customers “delighted” so they stay long-time Costco shoppers. Creating surplus consumer value is like digging a deep ditch where consumers just roll into it. The larger the consumer value, the deeper the ditch and the faster the consumers “roll in”, and the steeper it is for them to get out.

We can see JD exhibits some of these qualities when Richard Liu rebuked an employee for raising prices on an item that was selling out so quickly that they were almost out of inventory. Liu noted that this was short-sighted and chided him in a meeting, “You just think of earning money. Have you ever thought of the feelings of the customers that would hurt? You’ve made a few bucks in a short time, but you’ve lost heavily on the customer front”. Such sentiment demonstrates the concept of creating excess consumer value and there are many other similar examples from JD.

10 Ecommerce Variables of Consumer Value and Competition.

Below, we will define and exhibit the main different variables we see in creating a distinct consumer value proposition and differentiation vs. competition. In the first group is 1) trust, 2) selection, 3) price, 4) delivery speed, 5) consistency and 6) order ease. (We will only include a few snippets from our Coupang piece below, which has fuller explanations for why these variables matter and is worth revisiting).