*Please see our disclaimers at the bottom of the page and our full disclaimer here. By using our website, you acknowledge you have read our disclaimers and agree to our terms of use.

**This piece draws upon many of our prior research pieces, including Sea Limited, Alibaba, Didi, Coupang, Grab, and JD.

***Thank you to all of our subscribers! We hope you enjoy our Meituan piece and please join our Discord to continue the conversation!

Founding History.

Wang Xing, born in 1979, showed an early interest in computer science. His first direct exposure was an Apple II clone his parents bought him when he was in middle school, foreshadowing what would be a common theme throughout his future career. In the early 90s, he was among the first to get a modem and access the internet, allowing him to talk to the few other technophiles in China at the time, most of whom ended up founding their own tech companies. Wang Xing graduated from the prestigious Tsinghua University with an electrical engineering degree and then moved to the US in 2001 for a Computer Science PhD Program at the University of Delaware.

With the US leading on internet development, Wang Xing got to see ideas before they proliferated to China. After seeing the early US-based social network, Friendster, Wang Xing decided to return to China and with a small team—including Wang Huiwen who would later cofound several other companies with him—created a Chinese version of it called Duoduoyou. With limited traction he pivoted and created another social network, but this time aimed at Chinese students abroad called Youzitu. This latest iteration also failed to muster interest, but he luckily learned about “The Facebook” around then, which “gave” him another idea. Thinking perhaps his lack of success was owed to not creating a perfect enough facsimile, this time Wang Xing coded a pixel for pixel copy, including the tag that said “a Mark Zuckerberg creation” (they likely kept that because they wanted to benefit from consumer confusion thinking they were the real Facebook). This latest social network was called Xiaonei and in contrast to past efforts, it quickly garnered enough users to become problematic to their servers. As Wang Xing struggled to raise funds for the infrastructure needed to support their usage growth, he opted to sell it for a rumored few million US dollars to a rival social network which was renamed to Renren and had a successful IPO in 2011 and over 200mn MAUs before eventually falling into obscurity.

Thinking he had found a working formula, Wang Xing moved on to create a copy of Twitter call Fanfou in 2007. They quickly reached millions of users, but after users posted content that should have been censored, it was shut down for over 16 months, long enough to be relegated to irrelevance. He would have much better luck with his next start-up.

Background.

In 2010, Wang Xing embarked on a new project with frequent collaborator Wang Huiwen. Once again taking “inspiration” from the US, they aimed to create a Groupon clone, which they called Meituan. In a clear show of how popular that business model was at the time with VCs, just 5 months after founding Meituan, they were able to raise a $20mn Series A. They were far from the first Chinese entrepreneurs to copy Groupon, with an estimated 5,000+ different Groupon clones in China that were each trying to dominate the market. This was called “The War of a Thousand Groupons”, with the US-based Groupon themselves teaming up with Tencent and a $100mn war chest to attack the market. The land grab had thousands of start-ups dishing out tens of millions of dollars in marketing, plastering busses, subway stops, and buildings with ads calling on consumers to use their sites. Meituan considered such advertising a poor ROI and set themselves apart by focusing solely on more targeted online advertising. Given most online ad channels were very nascent at the time, they were able to hit above their weight with relatively little ad spend as CPMs were cheap (if you recall from our previous report, Coupang did the same). They emphasized analytics in allocating resources across cities and quickly throttled a city’s spend if they were not generating adequate returns. This careful provisioning of resources helped them outlast the slew of competitors who went bankrupt when their funding dried up.

Early on, Meituan made the decision to make their coupons fully refundable, even if the deal already passed, in order to be more customer friendly. The downside to this meant that they couldn’t use the positive working capital dynamics to fund growth as other start-ups were. However, this gave consumers more confidence in buying the coupons in the first place and helped earn them trust. Wang Xing always knew that the market would quickly consolidate to a few players with most competitors run out of business after burning through cash. If you slipped from the top, then you wouldn’t be able to garner subsequent funding and would quickly unwind. Meituan was able to maintain a leading position (which was just a high single digit market share, showing how fragmented the market was at the time) and they raised a $50mn round led by Alibaba in July 2011.

Among other leading players was Dianping, founded in 2003 by Zhang Tao. Dianping originally focused on user generated restaurant reviews and detailed rankings that scored not just the overall restaurant like Yelp, but also service, food quality, price, etc. Often referred to as the “Yelp of China”, the company actually pre-dates Yelp by a year. Given their merchant base, they considered group buying as a threat to their core business and moved into it a few years after Meituan. Dianping was funded by Tencent, making “groupons” and later food delivery one of the tech giants’ “proxy wars”.

Meituan focused early on on streamlining their IT systems, which allowed them to sign up merchants very quickly, which aided their sales teams in growing merchant adoption and empowered a better consumer experience. Their competency in back-end systems also allowed them to get by with a smaller support staff, which critically reduced overhead while they were still loss making—for example, their finance department had less than half the staff of one of their top competitors, despite processing 8x the volume. By the first quarter of 2013, they had grown their market share to ~30% compared to the Tencent-backed Dianping at ~17%, and another leading competitor, Lashou, at ~13%.

Despite their leading position, heavy competition and the groupon business model proving to be less than stellar drove them to diversify into other businesses (see our Coupang piece for more on why the groupon business model sputtered). Wang Xing split his employees into groups to explore different revenue opportunities that fit within their goal of being a local service platform that served O2O (online to offline). Maoyan, a movie ticketing platform was one business that was born out of the effort, as well as the groundwork for a hotel booking division, and a food delivery arm.

With the large assortment of restaurants already on their platform and many consumers already associating Meituan with food, they quietly pivoted towards food delivery as their core offering. The rationale was that food delivery is a huge market and a high frequency service, so winning this market would provide a sturdy app base with captive users to add other O2O services to. They raised another round in 2014 to focus on delivery: $300mn at a $3bn valuation. Then, just a year later, they raised more than double that amount, $700mn, at a $7bn valuation.

Dianping also had an ample war chest: $850mn they raised at a $4bn valuation. As Meituan moved into food delivery, Dianping and Tencent funded another food delivery competitor, Ele.me. Founded in 2008 to focus on food delivery for colleges, Ele.me was an early internet-enabled food delivery player. Dianping put the full weight of their platform behind it to drive them traffic. When users looked up restaurants on Dianping, they would be directed to Ele.me for food delivery. Ele.me focused their efforts on Tier 1 cities thinking the model would work best with the higher local density and above average earnings that top tier cities provided. While not wrong, they were caught flat-footed when Meituan aggressively went after lower tier cities, similar to what DoorDash did in the US by starting in the suburbs. As many businesses have learned the hard way, it is much harder to start at the high end of a market that has the best economics and move down market, than originally tool your operations to work with the worse economics that characterize the low end of the market. (The original disruption framework highlights that most disruption comes from orthogonal businesses with worse economics that then move into your core business).

With both Meituan and Dianping having raised so much capital, concerns were fomenting that it would all be wasted by the two companies fruitlessly trying to poach market share from each other. Even though Meituan and Dianping (including their partner Ele.me) were top food service players, their total market share was still relatively small with the rest of their competitors holding over half the market in groupons and food delivery. Together, they would be in a better position to focus on dominating the market, which was likely required to make any profit (owing to the slim margins of the industry). Interestingly, Sequoia China was an investor in all three (Meituan, Dianping, Ele.me) and likely had a role it was transpired next. (If there’s interest, we can do a deep dive on Sequoia China).

In October 2015, Meituan and Dianping announced an $18bn merger with Wang Xing and Zhang Tao to serve as Co-CEOs, an arrangement that was quickly discarded with Wang Xing taking the sole CEO spot. It is interesting that Dianping merged with Meituan instead of Ele.me given the common Tencent ownership, but Wang Xing and Zhang Tao’s rapport was allegedly better and Meituan’s larger O2O ambitions matched Dianping’s local platform well. Given that Tencent intended to retain their stake in Meituan Dianping, Alibaba opted to dump their ownership in the combined company and backed Ele.me as well as Dianping competitor Koubei (you can read more about these in our Alibaba report). Later, Alibaba would acquire and merge these two, along with their travel service Fliggy, into their own consumer life services unit, directly positioned against Meituan.

The Meituan + Dianping tie up gave Meituan the traffic advantage Ele.me used to enjoy and they started to win leading share in the food delivery wars. The year before the merger, Meituan had an estimated 28% market share in food delivery versus Ele.me at 31%, whereas the year after, Meituan led at 36% versus Ele.me at 35%. From there, Meituan would only continue to add market share, reaching ~65% in most markets, share that was mostly ceded from smaller sub-scale players.

While Meituan was inching towards winning the food delivery war, they simultaneously kept expanding the platforms offerings. While their movie ticketing platform Maoyan become an industry leader, what they did with their travel services was much more financially impactful. Watermelon, their hotel booking service, started out by focusing on local hotels in lower tier cities. They would sign up hotels that the larger OTAs (online travel agencies) ignored, which allowed Meituan to not only build unique supply, but sidestep the worst of the aggressive price war industry leading players Ctrip (later renamed to Trip.com), eLong, and LY.com were engaging in. The OTAs’ generally high margins (~30-40%) allowed for ample cash flows to try to steal market share from each other which drove down returns as each player had to defend their turf. Despite the competitive intensity, competitors were dismissive of Meituan’s hotel efforts, which allowed them to slowly build the lower end business without having to battle for it, which was critical given how food delivery was depleting their resources. Similar to their efforts in food delivery starting in lower tier cities, dominating 2nd and 3rd tier cities gave them a platform to launch into the higher end. To stem the pricing wars, the OTA industry started to consolidate. Leading player Ctrip invested in eLong and LY.com in hopes of turning down the competitive intensity and cooperated by sharing hotel inventory and filling in each others’ offerings on the “complete trip” package, which includes travel tickets and attraction reservations (with referral fees for completed bookings, they were more open to sharing traffic). Ctrip, with Tencent’s approval, who was an early investor in both eLong and LY.com as well, eventually merged the two into a combined platform that now sits in the holding company Tongcheng Travel—Ctrip and Tencent each maintained a ~21% stake. After the merger they enjoyed preferred placement in Tencent’s Weixin (WeChat) which resulted in over 80% of their traffic having been funneled in from Weixin. Getting arrogant with their competitive position as the industry’s competitive pressures turned down to a simmer, Ctrip hiked commissions as high as 25% and the door was opened for Meituan to pounce on the market by signing up big players like Hilton, InterContinental and Shangri-La Hotels. This marked the end of Ctrip’s golden years in travel.

The original thesis that a high frequency service like food delivery would allow a natural opportunity to cross sell other services like hotel bookings was playing out successfully: over 80% of new hotel booking users used another one of their services first. While the merged eLong and LY.com had a traffic channel in Weixin, Meituan funneled their food delivery customers to their travel services. Within a few years, Meituan was a top player in hotel bookings, surpassing Ctrip by number of rooms booked. Incredibly, just 8 years after Wang Xing founded the Groupon copy-cat, Meituan Dianping went public in 2018 on the Hong Kong Stock Exchange, raising $4.8bn at a $53bn valuation. Wang Xing’s ~11% stake made him one of China’s richest entrepreneurs. In the years that followed, they would continue to experiment and add new services, including bike share, instant-shopping, grocery, and community group buying. Today, Meituan is considered one of China’s premier tech giants alongside to Alibaba and Tencent, with a valuation that recently peaked at over $350bn. (With BAT being the acronym best known for representing Chinese tech, TMD was known as the “Next BAT” – made up of Toutiao (Bytedance), Meituan, Didi).

Business.

Meituan is China’s leading platform for local services. Initially focused on food delivery and travel services, they have continued to expand functionality to include movie tickets, grocery, bike-share, shopping, and pretty much every other local services you can think of, like haircuts, massages, and shared power banks (public phone chargers). Their strategy is to become China’s top e-commerce platform for services, focusing on mass-market, essential, high-frequency categories (like food delivery) and then leveraging that top position in the consumer’s mind by selling them other services (like travel). We will go into fee specifics later, but for most of their services they take a percentage of transactions (“take-rate”) which can range from 10-30% of an order’s value for food delivery and 8-15% for hotels (typically closer to the lower end at ~10%). LTM their business generated $28bn in revenues and grew +25% y/y last quarter, but net lost ~$3.6bn LTM. However, stripping out losses of ~$6bn from New Initiatives, they are EBIT positive (more on this later).

As shown above, Meituan has reached 693mn monthly transacting users as of 1Q22, which is more than double from when they IPOed (310mn in 2017). Incredibly, alongside their usage growth, they also have consistently increased transactions per user. This comports with their business thesis that adding more services will lead to increased usage and that more seasoned users tend to use the platform more.

Meituan has 3 reporting segments: 1) Food Delivery, 2) In-store, Hotel & Travel, and 3) New Initiatives. As seen above, Food Delivery makes up the majority of their revenue, followed by New Initiatives, with In-Store, Hotel & Travel last (the New Initiatives category includes more 1P transactions which distorts this comparison). However, in terms of profitability, the travel category is first. Whereas food delivery has EBIT segment margins (before unallocated overhead and SBC) of 6% for fiscal 2021, their travel segment is at 43%. We will be going into each segment in more detail shortly, but suffice to say travel is a much better business than their core food delivery. However, they need both in order to embark on their “super app strategy”, as we will touch on later.

As seen above, Meituan has grown total revenues since 2017 at a 52% CAGR with Food Delivery and Travel growing at 46% and 32%, respectively. Their New Initiatives, which includes some goods sold and recorded on a gross basis (1P direct sales), has grown ~25x since 2017. First, we will delve more into food delivery.

Food Delivery.

Meituan’s food delivery business is relatively straight-forward, but the accounting can be quite confusing. We will first go over how the platform works, which is similar to other food delivery services, and then move into the competitive and financial aspects.

To begin, a merchant lists their items on the Meituan app for free. The merchant—which is usually a restaurant but could be others like flower shops, bakeries, or convenience stores—sets prices, adds descriptions, and can upload photos. After creating a Meituan store for free, the merchant can either try to organically acquire users or pay Meituan for advertisements that show up throughout the app, usually in the search results of a user’s food query.

Users, after downloading and signing up for Meituan, which includes inputting address and payment info, are able to place orders at any of the 9mn merchants on their platform that are reasonably within their current location. When a user places an order they are charged an extra delivery fee which shows up as seen below. The delivery fee is often subsidized by the merchant, but if its not then it usually is just a couple RMB. There is sometimes a separate “container fee”, which is set at the restaurants discretion. Meituan also takes a “commission” which varies from 10-20% from the total value of the order, reducing the total income the merchant receives. They split this commission between a “platform fee” and a “delivery fee”.

After an order is placed, a user can follow the order progress in app. The merchant can either use Meituan’s couriers, a 3rd party courier, or their own employee to deliver the order. The last option is by far the most uncommon. Roughly 2/3rds of orders are delivered by Meituan couriers and the 3rd party couriers have strict guidelines for quality they must follow. Once the food is received, the user can interface with Meituan help support staff, which can mediate between the restaurant, should something be wrong.

As you may have picked up, that means there are three main sources of revenue for Meituan on a food delivery transaction, which they call: 1) Food Delivery Service, 2) Commission, and 3) Online Marketing Service. As seen below, their food delivery service fee is 56% of total food delivery revenue with commissions their second largest source at 30%.

1) Food Delivery. This is revenues recognized for providing on-demand food delivery services to certain merchants and transacting individuals as a principal. This is important to keep in mind as it will skew what their take-rate is, especially in light of the fact that roughly ~1/3rd or delivery orders are considered “3P” and do not have an associated food delivery service component but are still included in GTV. More on this later.

2) Commission. This is the variable fee that Meituan takes for allowing merchants to sell on their platform. The commission is usually charged as a % of the transaction value and is the main component of what is usually referred to as a “take-rate”. Usually, high take-rates are indicative of the economic value of a transaction mostly accruing to the platform.

3) Online Marketing Service. This segment is revenues generated from advertising on the Meituan app through either display ads or performance marketing, including sponsored listings. Meituan effectively is able to monetize their users’ time spent on the platform with display ads or through more targeted performance ads, which may show up only after a user expresses some intentionality. For example, if you search for dumplings, then you may see a sponsored ad for a dumpling store at the top of your results.

In the exhibit above, we show what each revenue line item is as a portion of total GTV (gross transaction value). GTV in 2021 reached RMB 700bn or $100bn annually. Meituan’s take-rate, calculated as revenue over GTV, is 13.7% today, which includes a boost of 1.6% from advertising. However, 1/3rd of food delivery orders is “3P” and they do not have associated food delivery service revenue. So if we gross-up the take-rate for that impact by adjusting the food delivery service revenue to assume it is 100% 1P, we see that their average take-rate is closer to 17.5%. We make this adjustment to get a better gauge of the average economics Meituan currently receives from a transaction. This also shows that their take is ~27% higher than the straight take-rate calculation implies.

Given that restaurants are low margin businesses to begin with, each point of take-rate can represent a large amount of profit. If a restaurant has 10% profit margins, each point they save is a 10% increase in profits. For many “take-rate” companies, part of the thesis is usually that they will be able to raise take-rates, which is usually ~95% incremental margin for the platform. However, understanding the economic viability of the full value chain is critical as they cannot take their fees up sustainably if it presses businesses to the point that they fold. While it is common amongst all of the platform companies, whether that be Uber, Didi, Grubhub, DoorDash (or even Ebay, Opentable, Etsy, Tmall, Amazon, JD.com, etc) to get the criticism that their portion of economics is too high, the unique factor here is that it is in the backdrop of a very “worker-sympathetic” government that has proven to be highly active in regulation. We will detail more on specifics later, but Meituan has already been touched by government regulation that capped certain fees. However, the tricky thing for Meituan is that they genuinely are not that profitable and rate increases are aimed at achieving some “fair” level of profitability, not price gouging. It is alleged that their take-rates have gotten close to 30% for some restaurants, which is very high, but it certainly isn’t showing up in the P&L as excessive profits. The fact is that roughly 80-85% of all delivery revenues (food delivery revenue + commissions) are paid out to the food worker, similar to other gig worker platforms. This leaves a very small amount of income to cover all of the overhead and service costs with the little left over. We think part of the reason why merchant fees are so high is because of the competitive environment that pressures Meituan to cut delivery fees to the consumer rather than charge them the real cost of delivery. The byproduct of this is that the merchant funds the delivery through paying higher commissions to Meituan. With this new regulatory regime focusing on merchants’ take-rates, perhaps that changes and the user will see higher delivery fees (for reference, when we checked, many deliveries were free or up to just RMB 4. Also keep in mind there is not really a tipping culture in China either).

A typical transaction might break down like this: a 40rmb AOV means the consumer pays 40rmb plus a delivery fee of 4rmb for 44rmb in total. Meituan takes 20% of the AOV, which is 8rmb plus the delivery fee for 12rmb. Then there is typically 2rmb of subsidy and the direct delivery cost (which varies a lot) is perhaps ~6rmb, generating 4rmb in contribution margin. This is what is left to cover all of their fixed costs as well as worker benefits. For third-party deliveries, Meituan will take ~4.5% of the AOV or 1.8rmb and give the remaining 10.2rmb to the third-party operator to make the delivery. (When we look at the average revenue per order on a consolidated basis below, these numbers will not be comparable because of the 3P accounting distortion. If you take 2/3rds of the 10rmb in revenue—12 less the 2 subsidy—and 1/3rd of the 1.8rmb then it is close, but this is just an illustrative transaction). Either way, the restaurant will receive 80% of the 40rmb, or 32rmb. The other piece of this is that the merchant may advertise on Meituan or may often fund a consumer subsidy themself, both of which reduce their economics.

Above we show that they have grown Food Delivery operating margins to 6.4% in 2021. But it’s important to realize that if their delivery payout ratio increases just 1%, then their profits will fall ~16%, which puts them in a precarious position given their limited ability to control delivery costs, especially with mandated benefits (which have not fully run through the P&L) or if weather is worse than usual, which historically drives incentives up. One source put the cost of benefits at ~1,500rmb a month, which can translate to a little over 1rmb per order if an average delivery courier completes 40 deliveries a day. This is clearly meaningful, as you will see profit per orders are sub 1rmb right now. They could potentially pass off some of this cost to consumers in the form of higher delivery fees, and in the context of a 40rmb order, it seems they may accept it. But the Chinese consumer is very price sensitive and will likely order elsewhere or simply pick up their own food at some point (a key question: if it’s that easy to raise the price 1rmb, why haven’t they already done that?).

The average food delivery order was 49rmb in 2021, of which Meituan’s take was 6.7rmb, including all sources of revenue. From this 6.7rmb they incurred 6.3rmb of costs, leaving a segment profit margin of just 0.4rmb. And this 0.4rmb does not include unallocated costs, namely stock-based comp, which if we assume only half of which applies to the food delivery unit, then their per order profit would drop from 0.4rmb to 0.2rmb.

This small profit per order is all Meituan has been able to generate despite being the clear industry leader in food delivery while exclusively operating in a market with some of the highest internet penetration and population density globally. Furthermore, you can see that their advertising revenue could be responsible for virtually all of their profits on delivery. The differentiated supply of food delivery means that there is value created in curating the options and helping surface an option that the user wants. It is because of this differentiated supply that there is an advertising opportunity in the first place, and as a side note, why food delivery is a better business than ride-hail despite much else of the economics being similar.

Advertising is just 1.6% of GTV today so perhaps there is some scope for that to grow but given the already fierce pushback to Meituan’s take-rates and them often responding with free advertising allowances, it’s not so clear. The overall low profitability of small restaurants also suggests that they don’t have much of an ability to advertise more. Theoretically, the restaurants’ ad spend should bring in incremental demand, but the return on ad spend often comes from converting a single order to a loyal returning customer, which is hard to do, especially when customers like variety and many other restaurants are competing for the same business. Most small business owners are not going to make an LTV model of the users they acquire to see if they are getting an adequate return on the users they acquire, but rather will just look at the number of orders and profit for a given period and assume any increase is due to the advertising. This effectively means that for a small restaurant to advertise, it needs to be profitable after that single transaction, which inherently limits the TAM.

There of course are large food chains that will bid on advertising with more of a lifetime value in mind, and there is no doubt that they are an important part of Meituan’s advertising base but Meituan can’t count on that alone carrying advertising growth indefinitely. Lastly, with larger food brands, they often advertise elsewhere, and with a lot of social media sites still adding inventory on increased time spent, there are a lot of options in the total advertising ecosystem. Meituan should have better conversion rates for food ads than showing that food ad on Douyin, for example, but the high conversion rate enjoyed on Meituan is offset by the potentially lower CPMs elsewhere. Having said that, Meituan does have a unique advertising offering as a user can have the item instantly delivered to them in just a few clicks with the transaction staying on platform and supported by Meituan staff should something go wrong. More to the point though, and validating a cautious enthusiasm for this revenue stream, we have seen many small merchants complain about their returns on the platform and do not advertise more than once. Having said that, the naturally high churn in the restaurant industry means that even if every business only advertises once, that can still be meaningful (since most restaurants don’t last beyond ~1 year). But we don’t like the idea of their ad growth being predicated on restaurants quickly going out of businesses just so they can suck up uneconomic ad spend from the next cohort. In the context of a “protective” government, this could become quickly problematic. Not to be too pessimistic though, we think there will be growth here over time, but would think it would be more of a single to low double digit growth rate longer term (vs 50% last year).

Below, we will say a bit on their main competitor Ele.me, before talking more about the business’ unit economics and potential steady-state profitability.

Ele.me. Alibaba invested in Ele.me in 2016 and acquired them in 2018. While Ele.me has a distant 2nd place market share at ~35% versus Meituan’s ~65%, Alibaba considers it a strategic asset so they can leverage their New Retail initiatives. New Retail includes a lot of physical stores, especially markets, of which they have several different formats. In order to mesh their markets and other physical stores to ecommerce, they are using Ele.me as a sort of connective tissue. A user who orders online can have orders fulfilled by Ele.me if they want it in <2 hours (usually takes ~40 minutes). This is not just another delivery option for Alibaba, but also opens them up to the grocery category, which they consider strategic owing to the high frequency nature of it. As Alibaba is under attack from all sides, one initiative is to focus on building consumer loyalty with essential, high frequency transactions with a physical retail footprint that is relatively harder to replicate. Meituan and JD are simultaneously going after grocery (more on this in other initiatives section), but Ele.me’s food delivery operation is a beneficiary of Alibaba’s focus on grocery as it is a customer acquisition funnel for them.

As we mentioned in the intro, Ele.me started in Tier 1 cities and Meituan launched in lower tier cities before building their way into the Tier 1 cities. The result of this has meant that Ele.me was late to most cities and has a smaller market share there. Despite several years of heavy subsidies, market share seems stable where it is and Meituan’s increasing local services offerings has made it harder for them to steal customers away. Having said that, Meituan was a beneficiary of the monopolistic practice dubbed “two choose one” which forced merchants to pick between being on Meituan or Ele.me. Merchants who didn’t pick were surcharged a 5% commission on their Meituan orders, likely wiping out any incremental profit they made by being on Ele.me. Meituan was fined ~$530mn for this practice in October 2021 and since then more merchants have started adopting Ele.me. Merchants do not like dependance on any single vendor and like the idea of having a Meituan competitor they can switch to in order to keep Meituan honest on pricing. This significantly lowered the stickiness of merchants and is a piece of why we believe fees are more likely to move down than up (regulation is the other big factor). However, despite Ele.me getting a win from the government taking action against Meituan for their “two-chose-one” policy, it has had limited impact on their market share.

Most of the consumer’s we spoke with used Meituan over Ele.me, but they noted that there wasn’t a huge difference between the two services—Meituan is just what they got used to first. A few complained Ele.me had worse selection, but that is likely improving because of the obsolescence of two-choose-one. However, few Meituan loyalist are interested in trying Ele.me again to see if it is a comparable selection to the app they already happily use. Our belief is that market share will stay steady between the two.

With Meituan’s market dominance and a profit of <0.5rmb per order, this clearly shows that food delivery is far from a stellar business, but it does display their foresight in quickly diversifying out into other business lines. (To be fair, they arguably do not use food delivery as just a profit center, but rather to drive frequency and keep a captive user base, but we think that decision was largely a byproduct of the fact that you couldn’t drive meaningful profits in food delivery even if you wanted to). The direct profit generation from food delivery is lackluster, but it makes more business sense if you think of it as a customer acquisition engine for their other businesses.

As we have mentioned in prior pieces, commanding high market share is critical for local delivery as it requires a ton of platform activity in order to kick off the flywheel of gaining enough food couriers to promise users quick food delivery and gain enough users to offer the food couriers enough jobs to earn a fair wage. Higher local density draws in more delivery couriers since the platform can match them jobs quicker and more users since food delivery wait times drop. This kicks off a virtuous cycle: more orders allow better route matching to more couriers who can deliver more orders more quickly, which reduces the delivery cost per order while increasing the couriers total pay and decreasing the users’ delivery costs, thus bringing in more users.

Management has put out a target of 1rmb operating profit per order versus the 0.4rmb they earned in 2021. However, there is more seasonality to profitability than one would expect with 2Q usually the strongest quarter: 2Q21 they earned 0.69rmb per order. This is driven by weather, which causes excess driver incentives when it is bad. This means that profit is highest when courier payouts are lowest, which makes sense, but we would not be willing to assume Meituan has any ability to decrease payouts in the context of a protective and active regulatory body. On the consumer incentive side, we have seen some analysis that extrapolates on their prospectus’ incentives disclosure to assume that Meituan still has ongoing food delivery incentives that they can cut. We walk through this thinking with the below analysis and are skeptical that this is a meaningful lever for Meituan.

As seen above, Meituan discloses two types of incentives: 1) Contra-revenue incentives and 2) incentives that are recorded in S&M. The distinction is similar to the one we saw Grab use (see our Grab piece for a lot more details on this), but to oversimplify, if the incentive is higher than the delivery fee, the amount equal to the delivery fee is recorded as a contra-revenue whereas the excess above it is recorded in S&M. In the below analysis, we assume that 100% of incentives are attributable to food delivery. This is a wrong assumption, but we make it to establish a possible upper bound of what incentives per delivery order could theoretically be given we do not have disclosure for just food delivery incentives. In reality, they also included incentives to their ride-hail, bike-share, and other New Initiatives in the S&M line, but it is not known how much that is (Travel is not included in either line item). If we had to estimate, we would attribute close to ~75% of the incentives below to food delivery, so keep that in mind, but either way it doesn’t change the analysis’ outcome.

As we show, incentives per order in 2017 were 1.6rmb, which if you recall is meaningfully above their EBIT profit per order of 0.4rmb in 2021. While we no longer have this disclosure, we know that total S&M is 4x what it was in 2017, so the logic is that there is still a meaningful amount of subsidies that are on-going. If you assume these incentives are roughly flat on a per order basis since 2017, cutting them could lead to EBIT profit per order jumping from 0.4rmb to ~2rmb, a huge increase. However, what portion of this increased S&M spend has been allocated to incentives is unknown, but we think through the logic of what would have to be true for them to be able to cut incentives.

Meituan has been the leading food delivery player for ~4 years with dominant market share, so any incentive activity that may currently be occurring is very likely necessary for them to keep their share of orders, especially in the context of Ele.me itching to take more share and JD recently announcing a potential entrance into the food delivery market (likely to better utilize and build up the network of their quick commerce delivery force). Perhaps someone can make the argument that Meituan can stop subsidizing the worst users and become more profitable, but on a shrunken user base. However, Meituan management has not indicated this intention to shrink at all, and it seems very unlikely given their historic (and on-going) focus on user growth. Additionally, there is the point that they use food delivery as a customer acquisition engine to cross-sell into other services like travel, and shrinking the core delivery platform for profitability would mean bleeding their potential cross-selling pool. Thus, for incentives to be a material factor in reaching further profitability, you would have to assume 1) that there are still material incentives across their entire user base, 2) that Meituan has been careless in keeping up incentives past their utility, and 3) that competition is more concerned about profits than market share and will not respond by maintaining or increasing incentives of their own. The most conservative assumption would be to believe they have already reached an equilibrium point of incentives and for them to reach their 1rmb profit per order, cutting down on subsidies is very unlikely a part of that path. (The dynamics with regulation could change this, with the industry cutting subsidies in lockstep to support increased worker benefits, but this too is speculative).

On an earnings call, on the topic of improving food delivery unit economics, they did not mention cutting incentives at all, which also gives us trepidation in assuming this is possible. They did note that further cost decreases can come from either increasing efficiency or technological improvements like AV. In the same breath though, they basically ceded that the “efficiency” lever has largely already been pulled. From the 2Q20 earnings call, they said “We believe we could still further enhance our delivery efficiency and further lower the delivery cost per order. Well, I’m not sure it will be very significant, but I think there’s still some room”. Other than improving order matching efficiency on higher volume, they call out autonomous technology. In 2020, they led a $500mn round in Li Auto, an EV start-up, defending it as a multi-decade investment in mobility technologies that will enable Meituan to deliver more efficiently in the long-term. They do not seem to expect anything to come of this partnership for years and even if it does come to fruition, where the economics accrue isn’t so clear to us.

There are only 9 levers they can pull to increase food delivery profitability and we quickly comment our thoughts on each.

1) Increase Merchant Commission Fee. (–) Given recent government concern with merchants complaining about high fees and recently introduced legislation, it seems their fees will be capped and in some cases they are actually having to lower them. Regulation aside, competition will also likely limit their ability to take fees up.

2) Increase Merchant Food Delivery Fee. (–) Regulation similarly applies to this fee. Meituan recently split their revenues between a commission, which is their “platform technology” fee and a food delivery service fee to ostensibly show that they technically lose money on food delivery (~2rmb per order) and it is subsidized by their platform technology fee. On a recent call, management confirmed that this was a case and noted it made sense for them to do so because it helped bring in more selection and support the ecosystem. However, we can speculate that this was done because they want to try to eventually get merchants to cover the full food delivery fee without Meituan subsidizing it from their platform fee. While this is conceivable, it doesn’t seem to make much sense that regulators will allow them to in totality raise fees, and regulators likely do not see the discrepancy that Meituan is trying to create. We think regulators will still look at the total take-rate Meituan receives when judging if fees are too high and thus it is unlikely this is a lever they can pull.

3) Increase Advertising. (+) This seems like their best bet to increase profitability. Online marketing as % of GTV is 1.5% and likely has scope to grow. It is hard to put a growth rate or range on where this could go, but we would say much less than 5% (the advertising as % of GMV we use as a rule of thumb for ecommerce platforms) owing to the much worse economics of the restaurant industry. The contribution margin structure of a restaurant (before ad spend) tends to be much worse than an ecommerce company selling products. This means that their ROAS is structurally lower and will hit a wall sooner than a higher margin company (i.e. $1 of revenue is worth more to them and they would be willing to pay more for it). To illustrate, if an ecommerce company has contribution margins of 30-50%, then they would only need a ROAS of 2-3.3x to break-even, whereas at 10-25% margins, you need 4-10x ROAS. Nevertheless, advertising is an opportunity, just one we are cautious on the upside with.

4) Increase Consumer Fees. (–/+) This seems unlikely as most consumers have gotten used to the fee rate they pay and would very likely churn to Ele.me if it was jacked up. Additionally, they want to grow user frequency and use food delivery as their platform base, so pushing on monetization seems at odds with that. Having said that, it is not impossible to think they can squeeze a 0.5-1rmb fee into an order that costs an average of ~50 RMB. We just wonder why, if they thought they could get away with it, they haven’t done it already. It surprised us how small some of the delivery discounts are with many discounting just 1-2rmb, but we imagine they wouldn’t be doing that unless they thought it made a meaningful difference.

5) Decrease Courier Payouts. (–) This does not seem likely given alternate opportunities of employment as a delivery courier and ~80% payouts seeming standard. Additionally, new regulations with benefits and driving treatment are driving costs up, not down. There technically are several classes of works: Meituan’s full-time and Meituan’s part-time workers, as well as 3rd party workers. In most cases, Meituan’s workers cost more, so pushing more labor to 3rd party delivery could incrementally improve labor costs, but it is unlikely to be material, especially as 3rd parties may now have to have more insurance and benefits than prior to the July 2021 notice.

6) Cut Consumer Incentives. (–) As mentioned above, we do not think this is likely, but it is more than possible if the industry does it in concert. Similar to our comments on the consumer fees, it seems plausible that they can get away with a 1rmb price increase, but again, the price sensitivity and discounting behavior currently on the platform suggest otherwise.

7) Improve Delivery Efficiency. (+) On margin, this can help a little as management noted, but given their high density and large network effects, they have already achieved the majority of efficiency here. The other aspect would be increasing batch (a courier takes multiple orders from the same restaurant) or group orders (user gets multiple orders at once). This has natural limitations too though as it slows down the delivery speed, but on margin it could improve a bit too.

8) Overhead Leverage. (+) As they grow orders and AOV, their overhead will grow slower and they will enjoy operating leverage. This is hard to estimate, but if you believe they can get 5 points of leverage, then that is roughly ~0.3rmb per order.

9) Other. (?) Management noted AV technology on an earnings call as an initiative driving further efficiency, but how this plays out for Meituan is unclear and also far off in the future. Perhaps the AV vehicle owners still take the same economics as a courier would or maybe the cost savings get competed away in the form of lower consumer prices. See our Didi piece for a fuller conversation on this subject, but we wouldn’t want to be dependent on a hypothetical technology to play out in a highly specific manner to improve profitability of a business.

While we can sympathize with the view that Meituan is touching a transaction with an average value of ~50rmb in a duopolistic industry, it seems wild that they can’t make a couple of RMB out of it. However, the truth of the matter is simply that when you break down the unit economics of it, that appears to be the case. There are too many parties vying for a cut of a small profit pool with customers that are highly sensitive to fee increases. Despite having a strong position for years in food delivery, they still have not been able to capture more than ~1% of this order value for themselves. The existence of a single competitor, Ele.me, has driven the industry returns down for everyone, and any hopes of raising take-rates have been almost permanently dashed by regulation. This is all to say that we do not have much of an expectation that they are able to meaningfully improve their EBIT per order figure without a marked shift in technology or the ability to increase fees. Their 1rmb goal isn’t out of question, and we think that over time, layering in advertising combined with some efficiency improvements and operating leverage, that they can get there, but it will a be slog. Of course, an investor may come to different conclusions than us on any or all of these points and perhaps even think they can earn well above management’s targets.

In-store, Hotel & Travel.

Meituan’s next segment, In-store, Hotel & Travel (which we will refer to as the IH&T segment for brevity from here on out) is their most profitable business. While generating just 18% of total revenues, or 1/3rd of what food delivery does, the Travel segment produces over 2x as much operating profit as their food delivery arm, accounting for a total of $2.2bn for 2021.

The In-store business is mostly a remnant from Dianping but is an important piece of their O2O strategy and also has some synergies with travel (particularly with restaurants). Their position in travel was born out of an effort to diversify into other businesses while the food delivery operation was sucking up cash. Travel, one of several bets placed at the time, turned out to be the most profitable for Meituan and helped solidify their strategy of earning captive users with high frequency, but low margin transactions, while cross-selling them into higher margin, albeit lower frequency transactions. Their hotel booking platform is similar to Expedia or Booking where users can browse a vast array of different local and domestic hotels with the ability to book a night in-app. The hotel owner benefits from a channel of traffic that tends to convert better since those users already have preloaded payment information making the transaction more seamless. The consumer gets the ability to compare a plethora of hotel options and compare prices without having to sign up for a separate service. As mentioned prior, part of what helped Meituan versus the incumbent players was that they started in lower tier cities that were not being serviced. Consumers would often book hotel stays in smaller cities when visiting family and having this hotel supply was unique. After they built a presence in the hotel space and continued to grow their user base, it was easier to convince the mid to high-end hotels to list on the platform as well, but they still over-index to lower tier cities and the less affluent. Meituan is also predominantly a hotel booking service within China, with limited international selection.

At the time of their IPO, they disclosed that 60% of users used a service in the IH&T segment (unclear how many solely used a travel service). Their ratio of rooms booked per active user was 0.7x in 2018, a number that has stayed fairly steady since then despite users almost doubling. However, if you assume the average person books at least 3 hotel room nights at a time, that implies only 160mn users booked rooms in 2021 for 23% penetration, which further implies that there is ample scope for Meituan to increase cross-sell and hotel room nights booked. The other piece of travel is attractions, experiences, and selling travel tickets (airfare, trains, etc) that they can sell in bundles or individually. Our understanding is that this isn’t a big business relative to the hotel room bookings, but there isn’t separate disclosure for it.

Meituan monetizes hotels & travel in two major ways: 1) commissions and 2) advertising. They will take an 8-10% commission of the value of every booking only if the customer completes the trip. Hotels are often willing to pay this because the opportunity cost of lower occupancy is forgone revenue as they have high fixed costs, but relatively low incremental costs. If the hotel owner can collect 200rmb from booking the hotel room out for the night, that could be an incremental 120rmb for them (maid service and utilities are the main incremental costs which cost maybe ~60rmb), so sharing ~20rmb (10% of 200rmb) is well worth it for the owner. However, the issue hotels have is that too much reliance on a booking platform like Meituan could mean Meituan starts taking a cut of all transactions, not just the “incremental” ones. This is why some larger hotel chains like Marriot try forking customers over to booking through their own sites and give additional loyalty points or deals for doing so. This trade-off of being a business enabler by providing traffic, but then also a detractor by commoditizing their offering and running down the margin structure of the business is common to any merchant who has dealt with being listed on a marketplace (all of these complaints are fairly similar for Amazon merchants for instance—they want the traffic Amazon brings as the cost of not being on Amazon is too much forgone opportunity, but they detest the high fees and having their products become less differentiated against a backdrop of dozens of other similar listings). Either way, as long as consumers prefer the marketplace experience like Meituan or Booking, hotels will have to play the game to get access to that audience, which is only growing. Like Coupang CEO Bom Kim is fond of saying, consumers are like flowers and merchants are bees: they have to go to where the flowers are.

The second way Meituan monetizes, which is also a point of tension with hotel operators, is advertising. Hotels can advertise across the Meituan app, including when consumers click into the travel section of the app as well as after they search a location. The sponsored listings in the search result page are great for advertisers because they are targeted towards consumers with high intentionality, but hotel operators think it can be unfair as it will move their listings down in the page ranking even if their hotel is ranked higher. This, of course, is the same criticism Google and any other company that shows search results gets, but it is a fairly established practice. We point it out only to continue to emphasize the “frenemy” relationship Meituan has with hotel operators, who are ready to cut Meituan out of the transaction when and if ever possible (again, similar with most merchants on any marketplace). The problem is that most hotels do not have a strong enough grip on the consumer to get them to gravitate toward their owned website to book there. Certain hotels, especially high-end luxury hotels and destination resorts have stronger bargaining power with Meituan (and can negotiate lower rates) because consumers will go out of their way to book there, but most hotels do not enjoy that preferred positioning in consumers’ minds.

As shown above, commission revenue and Online Marketing Service revenue are split about evenly. They stopped disclosing segment GTV when Corona hit and claimed it was no longer a useful metric of the business (a statement we disagree with, but since they combined In-store and Hotel GTV, it was much less useful). When they last reported it in 2019, they had RMB 222bn of GMV ($35bn). On total reported revenues of RMB 22bn in 2019, that is about a ~10% take-rate. However, since then, revenues have increased 50% and it is hard to believe GTV has increased commensurately in light of the pandemic, suggesting their total take-rate has gone up. Management alluded to as much on an earnings call when they said part of the reason for discontinuing the disclosure of GTV was because new monetization means like advertising would trend differently than GTV. This is a shaky argument as knowing GTV and the take-rate helps an investor better understand how healthy the economics of the ecosystem are, and whether the platform is nearing full extrapolation of their value of the transaction, or worse, over-extracting their share of economics at the long-term cost of a weaker ecosystem (hypocritically, management will still note strong GTV growth on earnings calls as a positive, which of course detracts from their argument that it isn’t a good business indicator). We agree though that having In-store GTV combined with Hotel conflates the business trends. Some industry experts believe that In-store GTV represented the majority, possibly at 60% or 70% in 2019. Other estimates put it more around 50/50 and think that Hotel is the majority now.

One of the key reasons incumbent Trip.com (Ctrip parent company) started bleeding market share was because they pushed the take-rate up too much, changing the hotel operators’ calculus on the opportunity cost of not being on the platform, as well as also opened up the door for competitors to undercut them. Trip could threaten to reduce the visibility of prominent hotel chains like Marriot and Intercontinental to throttle their traffic and gain leverage in fee negotiations (unclear if this actually happened, but it is an allegation that is hard to prove). This brazen show of how Ctrip could impact consumer purchasing decisions did lead to the chains capitulating on fees, but when they reached as high as 25%, they actively looked for other options. With the OTAs’ and hotel chains’ relationship souring, Meituan was able to win global distribution agreements with over 100 hotel chains at commissions that averaged ~10%. Undercutting Ctrip’s rates, paired with a growing and loyal user base was a punch to Ctrip who lost leading market share by # of hotels nights booked around 2017. However, Ctrip still has a far better hold on high end hotel bookings, which are higher value and thus likely still holds leadership by GTV. Now, Meituan has a total estimated market share of >50% by rooms booked vs Trip.com at an estimated ~25% and Tongcheng Travel (The merged eLong + LY.com) at ~10%. Trip generated ~$5.3bn of revenues in 2019, but in 2021 they were still lagging >40% from their 2019 peak with just $3bn in revenues. While no doubt the pandemic is a factor, Meituan in contrast actually grew from 2019 to 2021, with their IH&T segment revenues growing to ~$4.8bn, +45% since 2019. It is true that Meituan’s IH&T segment includes In-Store as well, so that does skew the data, but nevertheless these figures are still supportive of the assertion that Meituan has been a net share gainer in travel. However, it is also likely that domestic travel has been stronger than international, the latter of which is where Ctrip is stronger. Also implicit in these figures though, is that Ctrip is likely still more dominant in the higher end of bookings as they have higher revenues per booking (market share and revenue figures point to about a ~25% higher price per room).

Our consumer interviews, which heavily skew towards the relatively more affluent Chinese, support the assertion that Ctrip is more popular with the affluent as well as middle-aged and older users. This also makes sense given that Ctrip has a more robust outbound offering (hotels outside of China) and has been the biggest OTA advertiser for many years (Ctrip was founded in 1999). Meituan, partly owing to its relatively newer travel service, has larger adoption among younger users and users who come from lower tier cities who mostly travel within China. However, a good portion of the users we spoke with will still price check between both services and if prices are comparable seem to pick based on where they booked last time. One difference worth mentioning is that Ctrip has better customer service, which has become especially important since cancellations have become more common during Covid. All in all though, we see the value props as largely overlapping and as of now it seems market share will settle where it is with both growing in line with the market.

While it is not our base case, it does seem that Meituan is in a better position to gain share over time as they will likely reach a consumer through another one of their services before they decide they want to travel, whereas Ctrip has to rely on paid advertising to reach new users in an internet ecosystem with a weak general search. This is not a trivial point, as Booking Holdings (a US counterpart) spends prodigiously on Google to be a top search result when a customer is looking for hotels. A material portion of traffic is from Google (and to a lesser extent meta search engines). However, neither really exists in China, so Ctrip is relegated to lower funnel brand advertising. (They also have a 5,000 physical store network to serve customers who prefer in-person bookings, which is primarily aimed at lower tier cities). This is in contrast to Tongcheng Travel, who still has the Weixin level 2 access that drives traffic (more on this in our Tencent piece)—in fact, ~80% of their traffic comes from Weixin. Meituan built up their own source of traffic through their Super App and can push their travel offerings there, but Ctrip does not have a great owned channel to reach users in a similar way and instead must try to attract the user to their owned sites or mini-program through brand awareness. This is clearly a competitive disadvantage and over time could bleed them market share, or at the very least drive their customer acquisition costs up versus peers. Having said that, there is also an advantage of only doing one thing and having your brand strongly associated with a single “job” (booking hotel rooms) can more closely entwine in consumer’s minds that product to that job.

As shown below, the IH&T segment is much more profitable than food delivery with >40% margins in 2021. Their revenues are generated from a mix of commissions on bookings, fixed fees for listings (for In-store, more on this below), and advertising through platform. As it is an internet marketplace with low incremental costs to serve an incremental transaction, it scales up very well. Operating profits in 2021 reached ~$2.1bn from $1.25bn in 2019.

Looking forward, commissions are unlikely to increase, leaving just advertising to increase monetization on hotels. However, over-monetizing the platform with too many ads and sponsored listings can have the same effect as jacking up commissions as it forces hotel owners to pay up to maintain the same amount of traffic. As you may recall, Alibaba’s Taobao allows free listings, but monetizes through advertising and sponsored listings. However, many merchants are unhappy with this arrangement as they feel they must pay up to get any amount of traffic as the platform is loaded with >10mn merchant’s products. The more a platform relies on advertising, the more the organic results, which are usually the best fits for the consumer, deteriorate. This can further weigh on consumer experience, in addition to the general ad clutter. We don’t think this is an issue with Meituan today, but it is something to watch out for as they continue to lean on advertising to drive take-rate.

If a hotel owner has 20% margins on a 300rmb room today, then an 8% commission or 24rmb per room would mean their margins fall to 12%, a 40% reduction in the hotel owner’s profit. Layer in another 4% of GTV for advertising or 12rmb or 60% of their profits before paying Meituan’s fees. Perhaps this is tenable for the ecosystem to maintain given the limited bargaining power of the suppliers and relatively high margins to begin with, but push it too far and the marketplace will unwind with hotels leaving or going out of business. Perversely, if the hotel base consolidates enough then they can end up again with negotiating leverage against the platform. Large chains like Marriot and Intercontinental have some negotiating power to withstand usurious fees as they can leave the platform and have some success directing consumers to their owned properties (i.e. their websites and apps), but this still isn’t ideal for them as they lose access to a large user base with high-intentionality. We note all of this to say that it is not enough to just look at Meituan’s profitability, but you must also go a layer below to check that the hotel owners and chain operators have adequate economics to check that Meituan is behaving sustainably and not overearning. Typically, you want a business that helps all providers make money, not because it is necessarily the “fair” thing to do, but simply because it won’t be sustainable otherwise. We have heard some complaints on Meituan’s take-rates today, but by and large we think the hotel ecosystem is in a healthy place. We would want to see Meituan’s future growth come mostly from growing their user base and increasing frequency of trips booked rather than increasing take-rates (whether that be from commissions or advertising). In our travel build we will lay out more explicit assumptions, but we do not assume take-rates increase from the ~10% today (for the consolidated IH&T segment).

In-Store. In-Store is the other piece that is tucked into this segment. It is hard to figure out how meaningful this is in terms of revenue given limited disclosure, but no doubt Meituan believes it is very strategically important for them to own “local commerce”. This segment includes a variety of services including beauty, wedding planning, home renovations, vocational training, local retail, and in-restaurant dining. This is essentially what the Dianping business is, and they continue to add more local services to it (similar to Yelp in the US, but with more integrated into the businesses operation with online booking and payment through their platform more common). In theory it is a good business as there is no “real” COGS and they just take a commission on services or sales they help book through their platform. It is unclear how often the average user engages in these services though and what portion of the total segment revenue can be attributed to in-store, which they monetize similarly through a commission rate and advertising, but also with a fixed listing fee. The listing fee varies by vertical and is highest in the beauty and medical verticals. Approximately 85% of stores in Tier 1 cities are listed on Dianping, which falls slightly to 70% in Tier 2. Koubei, their most direct competitor, doesn’t have the same level of prominence and is very dependent on the Alibaba/ Ant Financial ecosystem. (As Tencent’s Weixin Pay has more adoption among SMBs, this could be a hinderance).

The users we spoke with seldom used these services beyond an occasional hair cut or massage. We did commonly hear though that these services are used more in lower tier cities, which makes sense given Meituan had high penetration in lower tier cities early on and they didn’t have many online enabled alternatives at the time. The higher density in Tier 1 cities also means that small businesses have larger customer bases that live within close proximity, making the “risk” of showing up to a business that could be busy much smaller. People still commonly like to call ahead too and don’t totally trust the app’s online booking.

In-store is an important business for Meituan as its the crux of their O2O (offline to online) strategy, and building out a focus on services puts them in a different position versus the other ecommerce giants who are focused on products. However, while Meituan is moving into more product sales as well—more on this to come. Dine-in is a strategically important service as well as it helps cater to all of a restaurant’s needs and has clear synergies with their food delivery operation. As noted though, overall this isn’t as well-used of a product as Meituan would like today, but if behaviors shift overtime, Meituan is no doubt in the best position to capture the local service market. And if they do, then it could be impactful to their bottom line as it is a business with high margins and low incremental costs with a large TAM. Nevertheless, this market hasn’t developed as much as we would have thought thus far. We will touch back on this in the Super App section, but first we will go through their new initiatives, which management considers important enough to lose ~$5.7bn per annum on, which almost twice the operating profit of their other two segments combined.

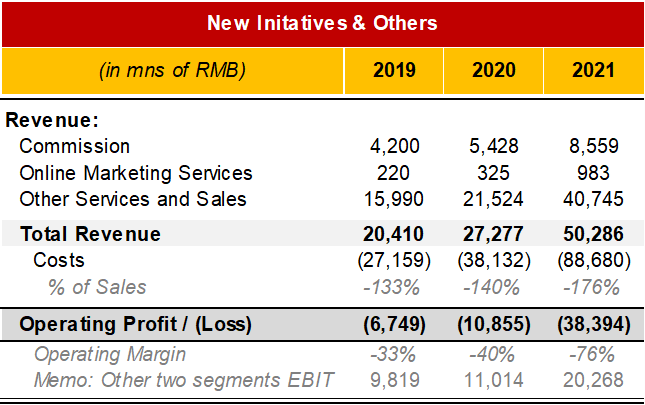

New Initiatives.

Meituan has a flurry of new initiatives to continue to add functions to their Super App and a few that help better support their merchants.

As seen above, New Initiatives are ~28% of total revenues. However, this is misleading because it includes a lot of products that are accounted for on a 1P basis. The 1P accounting is distorting this by around 20 points (i.e. if they were just an agent in the transaction, then New Initiatives would be around ~10% of revenues) but we do not have exact figures. (For more on how 1p vs 3p dynamics shift financial reporting, see our Sea Limited piece).

Either way, they are losing almost twice as much as they make in their other two segments in New Initiatives with a ~$5.7bn loss for 2021 versus ~$3bn in segment profits. This is also before layering in another ~$750mn in unallocated costs (not adjusted for fair value gains/losses which they include here). Below we will go through the slew of new businesses they are experimenting with, but at a high level, new efforts are aimed at either expanding their customer base, increasing user frequency and thus loyalty to Meituan, or supporting their merchant ecosystem. Somewhat disappointingly, none of these businesses appear to have the same opportunity to be a profit center on the same level of travel. But of course, it’s not so easy to find many high-margin businesses (especially in China) that easily fit in with their services focus.

Meituan Select. Launched in 2020,this is Meituan’s community group buy business where, similar to other group buy services, a user purchases items in a “group” with some specified minimum required participation for the transaction to go through and then either picks the items up at a location or a “group leader” delivers it to them (usually getting a commission). We have written about this in our Alibaba and JD pieces as it has been a very popular business model that many tech companies were quick to mimic. Alibaba, JD, and Didi all rolled out their own group buy businesses after seeing the success of Pinduoduo, the “original” community group buy player. (Check out our Alibaba piece for more specifics). Ironically, community group buy (CGB) is somewhat similar to the original Groupon business model Meituan copied over a decade ago, but this time focused more on products rather than services. Similarly, the fervor over this business is quelling, partly led by regulation that poured cold water on the excessive discounting which they referred to as “improper pricing behaviors”, but our bet is that they also discovered that this business was harder to execute, less profitable, and had a more fickle customer base than they had originally hoped.

JD’s Jingxi unit (which is their CGB business) was recently reorganized with layoffs (for the second time in 2022) as they rationalized the footprint they operate in. We said at the time of our JD report that “this business is unlikely to ever generate meaningful profits relative to JD’s core retail business, but there could be an ecosystem advantage to having it” and “make no mistake—this is a much lower quality business than their core”. Our claims seem to be supported by their recent curtailment. In our report, we noted that since the AOV’s in this segment are very low (RMB 30-50 or $4.50-7.50) with small gross margins (15-30% mark-up would yield a 13-23% gross margin) that leave roughly RMB 3.9-11.5 ($0.60 – $1.70) to cover packaging, fulfillment, delivery, and marketing (all before even allocating overhead). That is a very small margin to make the business operation work and would take significant volume to reach profitability. With so many players aggressively going after this market, it became even more uneconomic than usual with players selling goods under their costs as a customer acquisition strategy. This is one of the behaviors that caught Beijing’s attention as it wrecks the businesses of smaller grocers and stores, potentially putting them out of business. With an increased attention on CGB pricing strategies, the tech giants will have to find another way to get consumers attention. However, most of them are simply either shutting down operations or greatly reducing the footprint they operate in.

Meituan recently pulled out of Beijing and has laid off staff in addition to pulling Meituan Select from their app’s and mini-program’s home page. This is a stark pivot from just a year ago when Wang Xing said on an earnings call that there are “300-400mn users to acquire in the next few quarters” and that it was “an opportunity that comes once every 5 to 10 years”. Users from 2020 to 1Q22 did increase 182mn, which is significant, but this business has not materialized in line with their ambitions. At the time they were talking about CGB like it was their next “food delivery” platform, by which we mean a customer acquisition tool to build a second foundation of a large cohort of users with a high frequency service that they could then later cross-sell. From this framework, although they never admitted it, it seems they were conscious that CGB would never be a huge profit center with an economics profile more similar to food delivery than travel.

With this business getting fewer and fewer resources and an increasingly larger focus on stemming losses, it will be interesting to see how many of those new users they are able to hold onto. Nevertheless, this business will not be the platform expansion they were hoping for, at least not anytime soon. The overall rationalization of this industry could be a positive for long term development, but given typical Chinese competitive behavior, we think if this industry does become better, it will only spark another round of competition. Meituan’s competitive advantage here is a little unclear anyway as one of their most unique assets, their local delivery network, has limited involvement in this business. Meituan does have a large user base and was far earlier to this than everyone but Pinduoduo, however their moat here is extremely shallow. We actually thought JD, who owns their own logistics network that covers all of China including thousands of warehouses with the benefit of huge volumes from their core retail business to spread shipping costs, had the best competitive advantage longer term. With them pulling back too though, we think it is a mix of a realization of how hard it is to make the economics of this low margin business work, the regulatory focus, and the softening economic environment which has made companies shift to capital preservation mode. Long term we think this industry will still exist, just at a relatively smaller scale. It is unclear to us whether Meituan is still in this business in the long-term.

Meituan Grocery. Also known as Meituan Maicai, Meituan Grocery is their grocery delivery platform that was founded in 2019. They utilize a warehouse network close to the end customer to deliver fresh produce and other grocery products to the customer. Originally, they started operations in just Tier 1 cities (Shanghai, Beijing, Guangzhou and Shenzhen), supported by a 300-warehouse network, but have since expanded, especially on the back of Covid which drove some service stations to experience 3x typical volume.

As you may remember from our Alibaba and JD pieces, grocery has become a battle ground in ecommerce owing to the high frequency, large AOV, and essential nature of it. Most consumers will continue to shop at the same supermarkets week after week, so habituating consumers to their grocery platform is a top priority as they believe it will confer retention benefits and improve opportunities to cross-sell, in addition to being a potential source of profit. To bolster their position in grocery, Alibaba and JD are opening up their own supermarkets and offering delivery directly from there. Meituan seems to be taking a different route by scattering warehouses around a city that have the products stocked and can be formatted for quick picking and packing. This is in contrast to the Alibaba/ JD supermarket formats which usually require picking from the front of the store, the same way customers typically shop. This leads to slower packing, especially if its crowded. However, they have the benefit of selling the same inventory through two separate channels (in-store and online). Meituan’s model makes sense for them to optimize on quick delivery and it is much cheaper to open and operate a small warehouse than a full supermarket. It is still early innings in this industry and their Grocery operation is very likely loss making as they start it up, but it is a more promising initiative that fits well within their preexisting food delivery businesses and will benefit from piggy backing off of that network, with more efficient delivery order matching than what Alibaba or JD can currently do.

Meituan Instant Shopping. This is their delivery option for local commerce and enables users to purchase items that are sold by local stores in under 30 minutes. This category is also known as “quick commerce” and is most popular for items like FMCG and flowers, but has not gained broad stream adoption. Ideally, they want to position this as a service for users to get most of their shopping needs, but in reality, users tend to think of them when there is a high time sensitivity, which is not often. They are estimated to generate around RMB 60 to 70bn GTV, which is ~10% of their food delivery GTV, so it is becoming notable. However, competition is picking up with both Alibaba and JD making quick commerce a high priority. It is unclear how this market ultimately shakes out, but we are slightly skeptical on the ultimate TAM as the need to receive most products within ~30 minutes (and to pay a premium for that) seems limited. See our Alibaba, Coupang, or JD piece for more on local/ quick commerce.

Bike-Share. Meituan got their start in bike-share after acquiring Mobike in 2018 for $2.7bn USD. The logic here is similar to their other initiatives: add essential, high frequency services so users use the app more and feel they cannot live without. However, bike-share has been a particularly disastrous with them not only paying a lot for a bigger foothold in this industry, but with it also still unprofitable and no clear path for how that will change. Below is out commentary on Bike-share from our Didi piece, which captured the issues of this business model.

In the unit economic sketch above we estimate most of the costs, but the point stands that it is very easy to show incredibly strong unit economics if you assume a bike can last 3 years (or even 2) and frequency is just moderate. This attractive payback is what brought a glut of competitors and capital into the market. In reality though, the unit economics were much worse with most bikes lasting much less than a year. The increase in competition drove an oversupply of bikes and relative frequency suffered as a result. Tack on increased subsidies to get consumers to try their respective service and many start-ups were unable to bear the losses: Kuqi Bikes, Dingding Bikes, 3Vbikes, Wukong Bikes, Ofo, and many others were all forced to shut down operations. While the the start-ups thought they could get really quick paybacks, perhaps as low as a month, in reality they were usually contribution margin negative. The Actual Unit Economic sketch on the right is informed by Hellobike, which released an IPO prospectus before deciding to not IPO. In it we can extrapolate that average frequency is only ~1.4 rides per bike and contribution margin is close to 0 (they report just 7% gross margins). This is a great example of how a great business in theory can be decimated by idealistic assumptions and a ruthless competitive response.